15 June 2026• Pavan Adwani

Income Tax Search & Seizure

When the Income Tax Department Knocks Without Warning

Imagine it is early morning. You hear a firm knock at your door, and a group of officials identifies themselves as officers from the Income Tax Department. They carry a warrant. They are here to search your premises under Section 132 of the Income Tax Act. Your heart races. You do not know what to say, what to hand over, or what rights you have.

This scenario commonly called an income tax raid is one of the most stressful financial events a taxpayer can face. Yet, for thousands of individuals and businesses across India, it is a very real possibility. The Income Tax Department’s Investigation Wing has intensified search and seizure operations in recent years, leveraging advanced data analytics, the Annual Information Statement (AIS), and cross-referencing between GST returns and ITR filings to identify discrepancies worth pursuing.

Here is the critical point: an income tax search and seizure operation does not automatically mean you are guilty of anything. It means the department has reason to believe that undisclosed income or assets may exist on your premises. You have legal rights, procedural safeguards protect you, and expert representation can make an enormous difference to the outcome.

This comprehensive guide prepared by the expert team at Adwani and Company, led byDr. Haresh Adwani, PhD in Commerce and law graduate walks you through the complete income tax search and seizure process: what triggers it, what officers can and cannot do, what your rights are, how penalties work, and most importantly, how to protect yourself before one ever happens.

Read our detailed guide on: ITR 1 vs ITR 2 vs ITR 3 vs ITR 4: The Definitive Guide to Picking the Right Income Tax Return Form for AY 2026-27

What Is Income Tax Search and Seizure Under Section 132?

The income tax search and seizure power flows directly from Section 132 of the Income Tax Act, 1961. It is one of the most significant and most feared enforcement tools available to the Income Tax Department.

Legally speaking, Income Tax search and seizure operation allows authorized Income Tax officers to enter and inspect any premises residential, commercial, or otherwise seize books of accounts, documents, cash, jewellery, and other valuables believed to represent undisclosed income, and record statements from persons present at the scene.

The Income Tax Department’s official position, as reflected in its operational guidelines, is clear: search and seizure is a measure of last resort, reserved for situations where normal assessment channels cannot adequately unearth concealed income.

Search vs. Survey : An Important Distinction

Many taxpayers confuse a search with a survey. They are legally distinct operations with very different powers.

A survey under Section 133A is comparatively mild. It can only be conducted at business premises during normal working hours. Officers can inspect books of account and records but cannot seize assets during a survey.

An Income tax search and seizure is far more intrusive. It can happen at any hour, at any premises home, office, bank locker, or any other location. Officers can seize physical assets including cash, gold, jewellery, and digital records. Statements recorded during a search carry evidentiary value in subsequent assessment proceedings.

Understanding this distinction matters deeply because the two operations require different responses, and the consequences of each are fundamentally different.

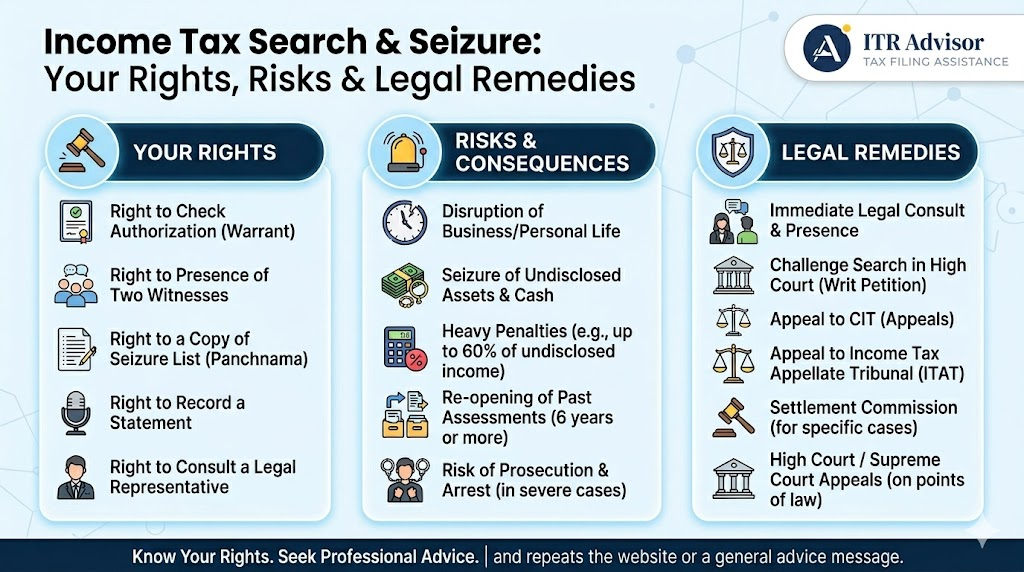

What Triggers an Income Tax Search and Seizure?

The Income Tax Department does not conduct searches randomly. Before any search warrant is issued under Section 132, the authorized officer must have documented “reason to believe” a legal standard that requires credible, concrete information rather than mere suspicion.

Common triggers that lead to an income tax search and seizure include:

1. Credible Intelligence Reports

The department’s Investigation Wing collects intelligence from multiple sources informants, government data systems, financial intelligence units about individuals or businesses holding substantial undisclosed income or assets.

2. Significant Mismatch in Financial Data

India’s tax infrastructure now cross-references GST returns, ITR data, AIS (Annual Information Statement), banking transactions, property registrations, and foreign remittances. A business declaring ₹40 lakh turnover while showing GST credits for ₹1.8 crore worth of input purchases is an obvious red flag.

3. Lavish Expenditure Inconsistent With Declared Income

High-value wedding expenditure, luxury real estate purchases, or acquisition of expensive vehicles that are not commensurate with declared income routinely trigger investigation wing activity.

4. Tip-Offs From Associated Parties

Former employees, business partners, or related parties sometimes provide information to the Income Tax Department. Such information, when independently verified, can form the basis of a search warrant.

5. Duplicate Books or Manipulated Accounts

Evidence of double accounting maintaining one set of books for tax purposes and another for actual business is a direct trigger for an income tax search and seizure under Section 132.

As Dr. Haresh Adwani explains: “The vast majority of search operations today are data-driven. With AIS, GSTN data, and property registry data all feeding into one analytical system, discrepancies that once went unnoticed for years now surface within months. Clean books are your best protection.”

The Step-by-Step Income Tax Search and Seizure Process

Understanding exactly what happens during an income tax search helps you respond calmly, correctly, and in a legally sound manner.

Step 1 : Authorization and Warrant

No search can begin without a valid written warrant of authorization issued by a senior authority typically the Principal Director General, Director General, Principal Commissioner, or Commissioner of Income Tax. This authorization must be based on documented reasons that meet the legal standard of “reason to believe.”

The Supreme Court of India, in landmark decisions including Pooran Mal v. Director of Inspection [1974] 93 ITR 505, upheld the constitutional validity of Section 132, holding that search powers directed at persons who have evaded tax on solid grounds are a reasonable restriction on fundamental rights.

Step 2 : Arrival at Premises and Identification

Officers must identify themselves and present the search warrant. You have the right to examine this warrant carefully. The search team must be accompanied by at least two independent local witnesses (panchas).

Step 3 : The Search Operation

During the search, officers may:

1.Enter and inspect every room, locker, safe, cupboard, or storage area

2. Break open any locked containers if keys are not provided

3. Examine all books of account, ledgers, digital files, and correspondence

4. Seize cash, jewelry, documents, electronic devices, and any other valuables believed to represent undisclosed income

5.Record statements from persons present

The entire process is documented through a formal

Panchnamaa contemporaneous record of proceedings that lists every item seized, every statement recorded, and all actions taken. A copy of the Panchnama must be provided to you at the conclusion of the search.

Step 4 : Post-Search Assessment

An income tax search and seizure triggers a special assessment process under Section 153A of the Income Tax Act. The Assessing Officer will issue notices requiring you to file returns for the current year plus the preceding six assessment years or up to ten years in cases involving serious undisclosed foreign assets or assets exceeding a prescribed threshold.

This is where the financial impact of a search operation becomes concrete. Every year in the six-year window can be reopened, reassessed, and subjected to additions, penalties, and interest.

Tax Rates and Penalties After an Income Tax Search

This is the section that taxpayers fear most and rightfully so. The tax treatment of undisclosed income discovered during a search is significantly harsher than regular income.

Section 115BBE: Flat Tax on Unexplained Income

Any income discovered during a search that cannot be explained — undisclosed cash, unexplained jewellery, unaccounted business receipts is taxed at a flat rate of 60% under Section 115BBE. With applicable surcharge and cess, the effective tax rate rises to approximately 77% to 83%. No deductions or exemptions are available against this income.

Section 271AAC: Additional Penalty

A penalty of 10% of the tax payable under Section 115BBE is levied under Section 271AAC, in addition to the tax already assessed.

Section 276C: Prosecution

Where willful tax evasion is established and the evaded amount exceeds ₹25 lakh, prosecution proceedings under Section 276C can be initiated. Conviction can lead to imprisonment of six months to seven years along with fines.

Practical Example:

Mr. Arvind Mehta runs a retail business in Mumbai. During an income tax search and seizure operation, officers discover ₹45 lakh in unaccounted cash kept in a safe, along with records of off-book sales totaling ₹1.2 crore over four years. Here is how his exposure is computed:

Item Amount

Undisclosed cash seized ₹45,00,000

Undisclosed income from books ₹1,20,00,000

Total Undisclosed Income ₹1,65,00,000

Tax @ 60% under Section 115BBE ₹99,00,000

Surcharge + Cess (approx.) ₹18,00,000

Penalty under Section 271AAC (10%) ₹9,90,000

Total Liability ₹1,26,90,000**

In other words, Mr. Mehta faces a liability of approximately ₹1.27 crore on undisclosed income of ₹1.65 crore effectively losing over 77% of the undisclosed amount to taxes and penalties, without accounting for interest under Section 234A or potential prosecution proceedings.

This example illustrates precisely why proactive compliance declaring all income, reconciling books correctly, and filing accurate ITRs is infinitely less costly than facing an income tax search and seizure

Your Legal Rights During an Income Tax Search and Seizur

Here is what most taxpayers do not know

you have significant legal rights during a search operation. Exercising them correctly, without obstruction, can materially affect the outcome of the subsequent assessment

1.Verify the Warrant

You have the right to examine the search warrant and verify the identity of every officer present. Ask to see identity cards. Note the warrant number and the name of the authorizing officer.

2.Call Your Chartered Accountant or Legal Advisor

You have the right to inform your CA or legal advisor about the search. At Adwani and Company, Dr. Haresh Adwani and the team are available to advise clients through search operations, helping them respond to statements and requests in a legally sound manner.

3.Receive a Copy of the Panchnama

At the conclusion of the search, officers must provide you with a signed copy of the Panchnama, listing every item seized and every statement recorded. Retain this document carefully it forms the foundation of your entire post-search legal strategy.

4.Retract Statements Made Under Coercion

Statements recorded during a search carry evidentiary weight. However, the law provides that statements extracted under coercion or undue influence can be retracted within a reasonable time. If you believe a statement was recorded under pressure, consult a qualified tax expert immediately.

5.Object to Retention Beyond 180 Days

The Income Tax Department cannot retain seized books of account or documents for more than 180 days without a valid extension order. If retention is extended, you have the right to make a formal application objecting to the extension.

6. Seek Judicial Review

If you believe the search was conducted without valid authorization, without meeting the legal standard of “reason to believe,” or with procedural lapses, you have the right to challenge the search in the appropriate High Court. Courts have the power to quash unlawful searches, and a significant percentage of additions made during search assessments are reversed in appeals on evidentiary grounds.

How to Prevent an Income Tax Search and Seizure

The most effective legal strategy is one that ensures a search never happens in the first place. The Income Tax Department’s own advisories consistently emphasize that voluntary, accurate, and timely compliance is the clearest protection against enforcement action.

Here are the key preventive practices recommended by Adwani and Company:

1. File accurate ITRs every year: Ensure all sources of income, including interest, dividends, capital gains, freelance income, and rental income, are properly declared.

2. Reconcile GST and ITR data: Your GST turnover and your ITR income must be consistent. Large, unexplained gaps are automatic red flags in the department’s analytical systems.

3. Maintain proper books of account: Preserve vouchers, invoices, bank statements, and supporting documents for at least seven years.

4. Explain large cash transactions: Any cash deposits above ₹10 lakh or large withdrawals should have documented explanations. The Annual Information Statement (AIS) on incometax.gov.in shows exactly what data the department has about your financial transactions.

5. Declare all assets in the ITR: The ITR Schedule AL (Assets and Liabilities) is compulsory for taxpayers with income above ₹50 lakh. Correct disclosure here is critical.

6. Respond promptly to notices: An ignored income tax notice escalates. A prompt, documented response demonstrates good faith and prevents matters from reaching search stage. *[Learn more about our Tax Compliance and Risk Management Services]*

Frequently Asked Questions

Q1. What is the difference between an income tax search and an income tax survey?

A search under Section 132 can be conducted at any time, at any premises, and includes the power to seize assets. A survey under Section 133A is conducted at business premises during business hours and does not include the power to seize assets.

Q2. Can income tax officers arrest me during a search and seizure?

No. Unlike customs, excise, or enforcement directorate operations, income tax officers do not have the power of arrest during a search and seizure operation. No person can be detained or arrested solely on the basis of an income tax search under Section 132.

Q3. What tax rate applies to undisclosed income found during a search?

Unexplained income discovered during an income tax search is taxed at a flat rate of 60% under Section 115BBE, plus surcharge and cess — bringing the effective rate to approximately 77% to 83%. No deductions or exemptions apply.

Q4. How many years can be reassessed after an income tax search?

The Income Tax Department can reopen and reassess the current assessment year plus the preceding six years — a total of seven years. In cases involving significant undisclosed foreign assets or income above a prescribed threshold, the window can extend to ten years

05.How can Adwani and Company help if I receive a post-search assessment notice

Adwani and Company, under the leadership of Dr. Haresh Adwani, provides end-to-end support for taxpayers facing post-search assessments — from reviewing the Panchnama and preparing explanations for seized items, to representing clients at assessment hearings, Commissioner of Income Tax (Appeals), and the Income Tax Appellate Tribunal (ITAT).

Conclusion

An income tax search and seizure is a powerful legal tool but it is not beyond challenge, and facing one does not mean the end of the road. The Income Tax Act provides significant procedural safeguards precisely because the legislature recognized that such a drastic power must be exercised responsibly.

What determines the outcome of a search and its aftermath is not just what happens during the search itself, but the quality of your documentation, the accuracy of your prior filings, and the expertise of the professionals who represent you in the months that follow.

“Compliance is not just about paying taxes. It is about building a financial record so clean, so consistent, and so well-documented that an income tax search would yield nothing because there is nothing to find. That is the standard every taxpayer should aspire to.”

If you are facing an income tax search, have received a post-search assessment notice, or simply want to ensure your tax affairs are structured to minimize enforcement risk connect with Adwani and Company today.

Our team, brings together decades of experience in income tax representation, search assessment defense, ITAT appeals, and proactive tax risk management. Whether you are an individual, a family business, or a growing company, we ensure you face the Income Tax Department from a position of strength, compliance, and confidence.

Author

Pavan Adwani – Corporate Advisory, Tax Compliance & Regulatory Management.He is actively involved in advising business entities on corporate compliance, tax management, and regulatory frameworks, with a structured and process-oriented approach.

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.