Capital Gains Exemption

Sold a house or a bundle of long-held shares this year and now staring at a capital gains figure that makes your stomach drop? You probably don’t have to pay tax on the full amount. Most taxpayers overpay not because they picked the wrong section, but because they never understood whether their capital gains exemption is judged by the asset they buy or the gain they invest.

What Is Capital Gains Exemption?

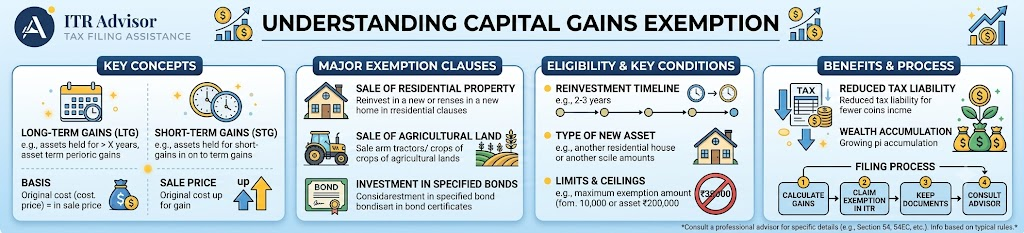

Capital gains exemption lets a taxpayer reduce or avoid tax on profit from selling property, land, gold, or securities, provided the proceeds or gains are reinvested in a specified manner within a prescribed time. The Income Tax Department recognises several such provisions commonly Sections 54, 54F and 54EC each built around a different combination of asset sold and asset purchased. The confusion begins when taxpayers assume all these sections work the same way. They don’t.

Asset View vs Gain View: The Real Difference

The Asset View : Sections 54 and 54F

Sections 54 and 54F anchor the capital gains exemption to the new asset you acquire a residential house in India. Section 54 applies when you sell a house and buy another; Section 54F applies when you sell any other long-term asset and reinvest the net consideration into a house. The exemption is proportionate to how much you reinvest.

The Gain View : Section 54EC

Section 54EC exempts gains from selling land or building when the gain amount, not the full sale proceeds, is invested in specified bonds (REC, NHAI, PFC, IRFC, or HUDCO) within six months, capped at ₹50 lakh a year. No particular asset needs to be purchased — only the gain needs a home.

Choosing the Right Capital Gains Exemption Route

Most taxpayers can combine both views reinvesting part of the gain in a house under Section 54 or 54F, and the remainder in Section 54EC bonds within six months, subject to each provision’s caps.

- Sold a house? Compare Section 54 (asset view) against 54EC (gain view).

- Sold land, gold, or shares? Section 54F is your asset-view option.

- Can’t decide immediately? A Capital Gains Account Scheme deposit protects your window.

Key Takeaways

- Capital gains exemption is either asset-based (Sections 54, 54F) or gain-based (Section 54EC).

- Section 54EC is capped at ₹50 lakh a year with a strict six-month window.

Combining both views, where eligible, can maximise your exemption.

Read our detailed guide on Tax Saving vs Wealth Creation in India: Are You Investing Smart or Just Buying a Deduction?

Why Professional Guidance Matters

According to Dr. Haresh Adwani of Adwani & Co LLP, most capital gains exemption claims fail scrutiny not from picking the wrong section, but from missing the reinvestment timeline or the CGAS deposit deadline a risk that grows as the Income Tax Act, 2025 renumbers these provisions from April 2026. The Income Tax Department’s official guidance and notified Section 54EC bond lists are a useful starting point, though joint ownership and NRI cases need individual review.

Frequently Asked Questions on Capital Gains Exemption

1.Can I combine Section 54 and Section 54EC?

Yes. You can split your capital gains exemption between a new house under Section 54 and bonds under Section 54EC.

2.What if I can’t reinvest before filing my return?

Deposit the gain in a Capital Gains Account Scheme before the filing due date to preserve the exemption.

3.Does capital gains exemption apply to short-term gains?

No. Sections 54, 54F and 54EC apply only to long-term capital gains

Conclusion: Plan Your Capital Gains Exemption the Smart Way

Capital gains exemption rewards taxpayers who understand whether their provision watches the asset bought or the gain invested. Get this right before your reinvestment deadline, and connect with itradvisor.in today for guidance on your capital gains exemption claim for AY 2026-27.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

At ITRAdvisor.in, we help NRIs and returning Indians with:

✔️ NRE and NRO taxation

✔️ Residential status determination

✔️ Returning NRI tax planning

✔️ DTAA advisory

✔️ Foreign asset reporting

✔️ NRI Income Tax Return filing

✔️ Tax notice handling

✔️ Capital gains and property taxation

If you are unsure whether your NRE interest is taxable, whether you need to file an ITR in India, or how to handle NRO income, professional guidance can help avoid costly mistakes.

Visit ITRAdvisor.in to schedule a consultation and get clarity on your NRI tax obligations.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.