GST Appeal Pre-Deposit in APL-01

If you’ve ever tried to file a GST appeal after receiving a demand order, you know how unforgiving the GSTN portal can be. A single locked field, an uneditable pre-deposit amount, and your entire GST show cause notice reply appeal collapses before it even begins. For months, taxpayers and tax professionals across India were struggling silently with exactly this problem the pre-deposit field in Form APL-01 was simply not accepting inputs. That nightmare is over. After a long-awaited GST portal fix in April 2026, the APL-01 pre-deposit field is now editable, and here’s everything you need to know to file your GST appeal correctly.

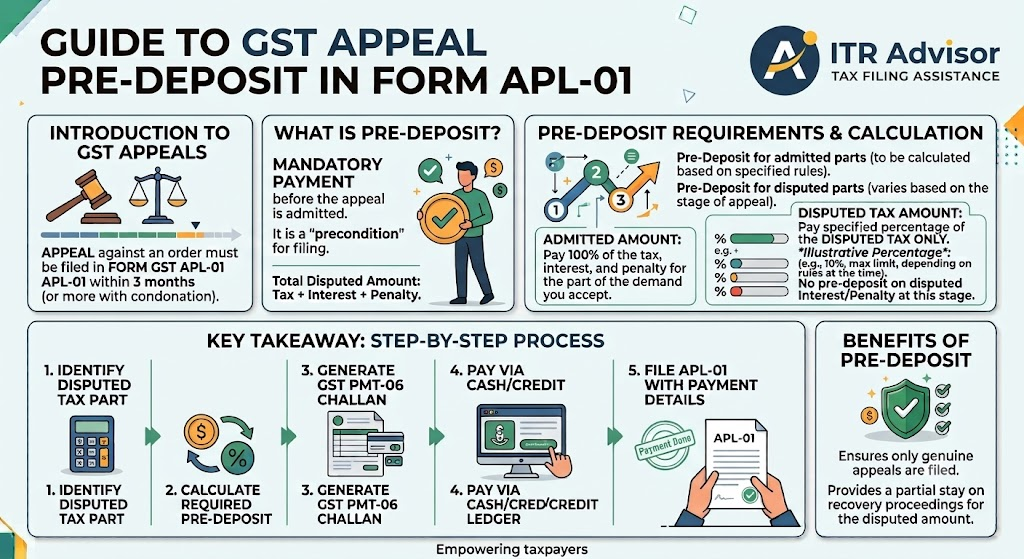

What Is GST Appeal Pre-Deposit and Why Does It Matter?

Under Section 107 of the CGST Act, 2017, a taxpayer who wishes to appeal against a GST demand order before the Appellate Authority is required to deposit a portion of the disputed tax amount upfront. This mandatory pre-deposit for GST appeal is not optional without it, the appeal is not even admitted. The Income Tax Department’s analogy here is instructive: just as you cannot contest an assessment without meeting procedural requirements, the GST law demands that appellants demonstrate financial seriousness before the dispute is heard.

Specifically, the GST appeal pre-deposit requirement is:

- 10% of the disputed tax, interest, and penalty for a first appeal before the Appellate Authority (Section 107(6))

- 20% of the disputed tax for a second appeal before the GST Appellate Tribunal (Section 112(8))

- This amount must be paid through the Electronic Cash Ledger or Electronic Credit Ledger, and the ARN (Acknowledgment Reference Number) of the payment must be correctly entered in Form APL-01

The APL-01 Pre-Deposit Field Problem: What Was Going Wrong?

Between late 2024 and early 2026, a critical technical bug on the GSTN portal made it impossible for many taxpayers to enter or edit the pre-deposit amount in the APL-01 form. The field appeared greyed out, or the entered value would reset to zero upon submission. This was not a user error it was a confirmed portal-level glitch that impacted a large number of GST appeal pre-deposit 2026 filings.

The consequences were severe:

- Appeals were filed without the mandatory pre-deposit amount being captured

- Several Appellate Authorities dismissed appeals on technical grounds, citing non-compliance with pre-deposit conditions

- Taxpayers who had already paid the 10% pre-deposit could not link it to their appeal due to the locked field

- CA firms had to resort to offline submissions and hardcopy representations to circumvent the portal issue

April 2026 GST Portal Fix: What Has Changed in APL-01?

The GST Network (GSTN) rolled out a backend portal update in April 2026 that specifically addressed the APL-01 pre-deposit field freeze issue. As of this update, the following improvements are live on the portal:

1. Pre-Deposit Amount Field Is Now Fully Editable

Taxpayers can now directly enter the pre-deposit amount paid under the Electronic Cash Ledger (ECL) or Electronic Credit Ledger (ECRL) while filing Form APL-01. The amount auto-validates against the challan details on record.

2. ARN / CIN Linkage Is Seamless

The portal now correctly links the Challan Identification Number (CIN) or ARN of the pre-deposit payment to the appeal form. This eliminates the need for manual reconciliation, which was the biggest pain point in the earlier GST portal version.

3. Split Pre-Deposit Across Tax Heads Now Supported

A known limitation was that the portal did not support split pre-deposits across CGST, SGST/UTGST, and IGST heads in one filing. The April 2026 fix allows taxpayers to enter pre-deposit amounts separately for each tax head, making it far easier to handle appeals involving interstate supplies or disputed ITC mismatches.

4. Real-Time Pre-Deposit Validation

After entering the pre-deposit details, the form now runs a real-time check against the demand order amount and flags mismatches before final submission. This proactive validation is a significant improvement over the earlier system where errors surfaced only post-submission.

GST Appeal Pre-Deposit: Quick Reference Table

| Appeal Level | Pre-Deposit % | Form | Time Limit |

| First Appeal (GST Officer → Appellate Authority) | 10% of disputed tax | APL-01 (GSTN Portal) | 3 months from order date |

| Second Appeal (Appellate Authority → Tribunal) | 20% of disputed tax | APL-05 (Tribunal) | 3 months from order |

| High Court / Supreme Court | As directed by Court | WP / SLP | No fixed limit |

Step-by-Step: How to File GST Appeal in APL-01 After the Portal Fix

Now that the APL-01 pre-deposit field is editable, here is the correct process to file a GST demand order appeal on the GSTN portal as of April 2026:

Step 1: Pay the Pre-Deposit First

Log in to the GST portal (gst.gov.in). Navigate to Services → Payments → Create Challan. Pay the required 10% of disputed tax under the applicable tax head (CGST/SGST/IGST). Note the CIN carefully.

Step 2: Open Form APL-01

Go to Services → User Services → My Applications → New Application → Appeal to Appellate Authority. Select the correct order against which you are appealing (DRC-07, OIO, or equivalent demand order).

Step 3: Enter Pre-Deposit Details

In the ‘Pre-Deposit Details’ section, which is now fully editable after the April 2026 fix, enter the CIN and the amount deposited for each tax head. The system will validate the amount against 10% of the demand.

Step 4: Upload Supporting Documents

Attach the demand order, your reply to the GST show cause notice, any hearing notices, and the payment challan. File size limits apply compress PDFs where necessary.

Step 5: Submit & Track

Submit the form. You will receive an ARN for the appeal. Track the status under My Applications. A hearing notice is typically issued by the Appellate Authority within 30–60 days.

Expert Perspective: Why Correct Pre-Deposit Entry Is Non-Negotiable

According to Dr. Haresh Adwani, a PhD in Commerce and law graduate associated with Adwani & Co LLP, the pre-deposit is not merely a procedural formality it is a jurisdictional requirement. The Appellate Authority does not have the power to condone non-compliance with Section 107(6). Even if the non-compliance was due to the portal’s technical bug, the burden of proving that the pre-deposit was indeed paid falls on the taxpayer.

This is why it is critically important to:

- Always pay the pre-deposit before initiating the APL-01 filing, never simultaneously

- Retain the original challan and CIN as primary evidence

- Cross-verify the pre-deposit amount entered in APL-01 with the actual demand order figure

- If the appeal period is expiring, file immediately and supplement with a condonation application if needed

Read our detailed guide on Complete GST Compliance Checklist for Small Businesses in Pune: Essential Guide for FY 2026–27

Key Takeaways

The APL-01 pre-deposit field is now editable on the GSTN portal after the April 2026 fix.

✅ A 10% pre-deposit of disputed tax is mandatory for a first appeal under Section 107 of the CGST Act.

✅ Pay the pre-deposit via challan first, then enter the CIN in the APL-01 form never enter blank.

✅ The April 2026 update supports split pre-deposit across CGST, SGST, and IGST heads.

✅ If your earlier appeal was dismissed due to this portal bug, consult a GST professional immediately for remedial options. ✅ Always file within the 3-month limit from the date of the demand order condonation is discretionary, not guaranteed.

Frequently Asked Questions

Q1. What is the GST appeal pre-deposit amount required for filing APL-01?

For a first appeal before the Appellate Authority under Section 107(6), you must deposit 10% of the disputed tax, interest, and penalty. This amount must be paid before submitting Form APL-01 on the GSTN portal.

Q2. Is the APL-01 pre-deposit field editable now on the GST portal in 2026?

Yes. The GSTN rolled out a fix in April 2026 that makes the pre-deposit field in APL-01 fully editable. You can now enter the CIN, payment date, and tax-head-wise split correctly.

Q3. What happens if I filed a GST appeal without entering the pre-deposit amount due to the portal bug?

Your appeal may have been dismissed on technical grounds. You should immediately consult a GST professional and explore filing a fresh appeal with condonation of delay, or a writ petition before the High Court if the appeal period has expired.

Q4. Can I use the Electronic Credit Ledger (ITC balance) for the GST appeal pre-deposit?

Yes, the pre-deposit can be paid through both the Electronic Cash Ledger and the Electronic Credit Ledger. However, it must be from the same GSTIN under appeal, and the CIN or ARN must be linked in APL-01.

Q5. What is the time limit to file a GST appeal in Form APL-01 after a demand order?

The appeal must be filed within 3 months from the date of the demand order or OIO. The Appellate Authority can condone delays of up to 1 month for sufficient cause, but condonation beyond that is not permitted under the statute.

Conclusion: Don’t Let a Portal Glitch Cost You Your GST Appeal

The April 2026 GST portal fix is a much-needed correction that restores the integrity of the GST appeal process. But knowing that the pre-deposit field is editable is only the first step. Filing a GST appeal correctly with accurate pre-deposit entry, proper document attachment, and strict adherence to time limits requires both technical knowledge and practical experience. A wrongly filed APL-01 can result in your appeal being dismissed or the pre-deposit being forfeited, leaving you with no recourse against an unjust demand order.

The GST framework, as administered through gst.gov.in and supported by circulars from the Central Board of Indirect Taxes and Customs (CBIC), is complex but navigable with the right guidance.

Whether you are responding to a GST show cause notice, planning a Section 107 appeal, or recovering from a dismissed filing, expert support can make all the difference.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP

Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later

If you or someone you know has received a Section 148 income tax reassessment notice, do not panic but do act quickly and smartly. The law is on your side, provided you know where to look.

📞 Take Action Today

Need help evaluating whether your income tax reassessment notice is valid?

Connect with the experts at itradvisor.in for a detailed assessment of your notice, legal objection drafting, and end-to-end reply support. Visit: www.itradvisor.in | Powered by Adwani & Co LLP