ESOP Tax Trap

A senior employee once shared the news with quiet pride: “My company has granted me ESOPs worth ₹50 lakh.” The excitement was real. The number was real. But the tax problem lurking behind it? Completely invisible to them. If you hold ESOPs and haven’t thought about ESOP tax implications in India 2026, you may be walking straight into an unexpected tax liability one that arrives before a single rupee lands in your bank account.

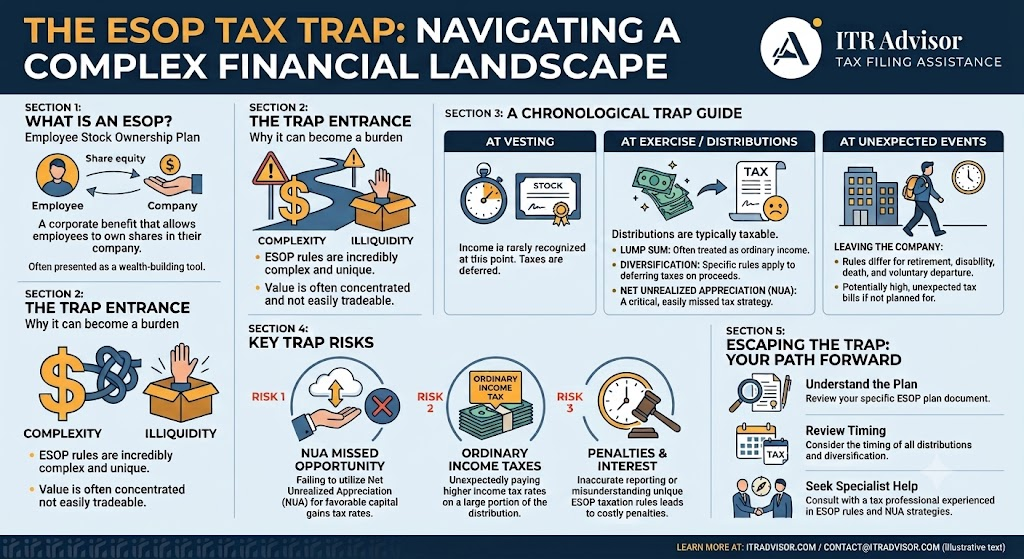

What Are ESOPs and Why Does the Tax Timing Matter?

Employee Stock Option Plans (ESOPs) are a popular component of compensation packages across Indian startups and MNCs alike. They give employees the right to purchase company shares at a pre-determined price (the exercise price) at a future date.

The critical issue with ESOP taxation in India is not whether you will be taxed you will be but when, and on how much. Most employees focus on the grant letter figure and miss the two separate tax events that can arise.

Stage 1: Tax at the Time of Exercise The Perquisite Trap

This is where most ESOP holders are blindsided. Under the Income Tax Act, 1961, the benefit you receive upon exercising your stock options is treated as a perquisite under the head ‘Salaries’. The taxable amount is calculated as:

Taxable Perquisite = (Fair Market Value on Date of Exercise − Exercise Price) × Number of Shares

ESOP Perquisite Tax Calculation: A Real Example

Let’s make this concrete with a simple illustration:

Exercise Price: ₹100 per share Fair Market Value (FMV) on Exercise Date: ₹600 per share Number of Shares: 10,000 Taxable Perquisite = (₹600 − ₹100) × 10,000 = ₹50,00,000

This ₹50 lakh is added to your salary income and taxed at your applicable slab rate. For a taxpayer in the 30% slab, the tax liability could be ₹15+ lakh before selling a single share.

Your employer is required to deduct TDS on this perquisite value at the time of exercise. According to guidelines issued by the Income Tax Department (incometax.gov.in), the employer must report this as part of Form 16.

What Is FMV and How Is It Determined for ESOP Taxation?

FMV Fair Market Value is the crux of the entire ESOP tax calculation. The method of FMV determination depends on whether the company is listed or unlisted.

- Listed companies: FMV is the average of the opening and closing price on the date of exercise on a recognised stock exchange.

- Unlisted companies: FMV must be determined by a Category I Merchant Banker registered with SEBI. The valuation report is critical documentation.

For start up employees, ESOP taxation on unlisted company shares is especially misunderstood. The FMV can be significantly higher than the exercise price even if the company hasn’t gone public creating a paper tax liability with no immediate liquidity to pay it.

Stage 2: Capital Gains Tax When You Sell the Shares

After exercising, when you eventually sell the shares, a second tax event occurs this time under Capital Gains.

- The cost of acquisition for capital gains purposes is the FMV on the date of exercise (since that value was already taxed as perquisite).

- Short-Term Capital Gains (STCG): If shares are sold within 12 months (24 months for unlisted), gains are taxed at 15% for listed shares.

- Long-Term Capital Gains (LTCG): If held beyond the qualifying period, LTCG above ₹1 lakh on listed shares is taxed at 10% without indexation.

For unlisted company shares, LTCG is taxed at 20% with indexation benefits if held for more than 24 months.

Read our detailed guide on ESOP Valuation in India: What Every Employee and Founder Must Know in 2026

Key Takeaways: ESOP Tax Implications in India 2026

1. ESOPs are taxed at two stages: at exercise (as salary perquisite) and at sale (as capital gains).

2. The taxable perquisite = (FMV − Exercise Price) × Shares, and it’s added to your income in the year of exercise.

3. For unlisted startups, FMV is determined by a SEBI-registered merchant banker.

4. TDS is deducted by the employer at the time of exercise.

5. Timing your exercise strategically can significantly reduce your effective tax liability. 6. ESOP capital gains tax depends on the holding period and whether the company is listed or unlisted.

Questions to Ask Before Exercising Your ESOPs

As highlighted by Dr. Haresh Adwani, a PhD in Commerce and legal expert with decades of tax advisory experience, most employees make ESOP decisions without understanding the financial math behind them. Before you exercise, ask:

- What is the current FMV and who has certified it?

- What will my perquisite tax liability be in this financial year?

- Is this a listed or unlisted company, and how does that affect my tax?

- Do I have the liquidity to pay the tax before I can sell the shares?

- What is the optimal timing strategy to minimize my total tax outgo?

Frequently Asked Questions: ESOP Tax Implications India

Q1. When is ESOP taxed in India at grant, vesting, or exercise?

ESOPs are not taxed at grant or vesting. Tax is triggered at the time of exercise, when the difference between FMV and exercise price becomes a taxable perquisite under the head Salaries.

Q2. How is ESOP perquisite tax calculated for unlisted start up employees?

For unlisted companies, the FMV is determined by a Category I Merchant Banker registered with SEBI. The taxable perquisite is (FMV − Exercise Price) × number of shares, taxed at the employee’s applicable income slab rate.

Q3. Is capital gains tax applicable on ESOPs after sale?

Yes. After exercise, if you sell the shares, capital gains tax applies. The FMV on the exercise date is treated as the cost of acquisition, and gains are taxed as STCG or LTCG depending on the holding period.

Q4. Does the employer deduct TDS on ESOP perquisite?

Yes. The employer is legally required to deduct TDS on the perquisite value at the time of exercise and report it in Form 16. This amount is reflected in your total salary income for the year.

Q5. What is the ESOP tax treatment for unlisted company shares in India 2026?

For unlisted shares, LTCG applies at 20% with indexation if held for more than 24 months; STCG is taxed at slab rates. The FMV must be certified by a SEBI-registered merchant banker for tax purposes.

Conclusion

ESOPs are a genuine wealth-creation tool but only for those who understand the ESOP tax implications in India before making the exercise decision. A poorly timed exercise can generate a tax bill that far exceeds available cash, particularly for start up employees holding unlisted company shares.

The good news: with the right tax planning, you can time your exercise, stagger your sales, and significantly reduce your overall tax burden. The key is knowing the numbers before you act.

About the Author – Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.