10 Common ITR Filing Errors That Can Trigger Income Tax Notices in 2026

08 June 2026• Prafull Nile

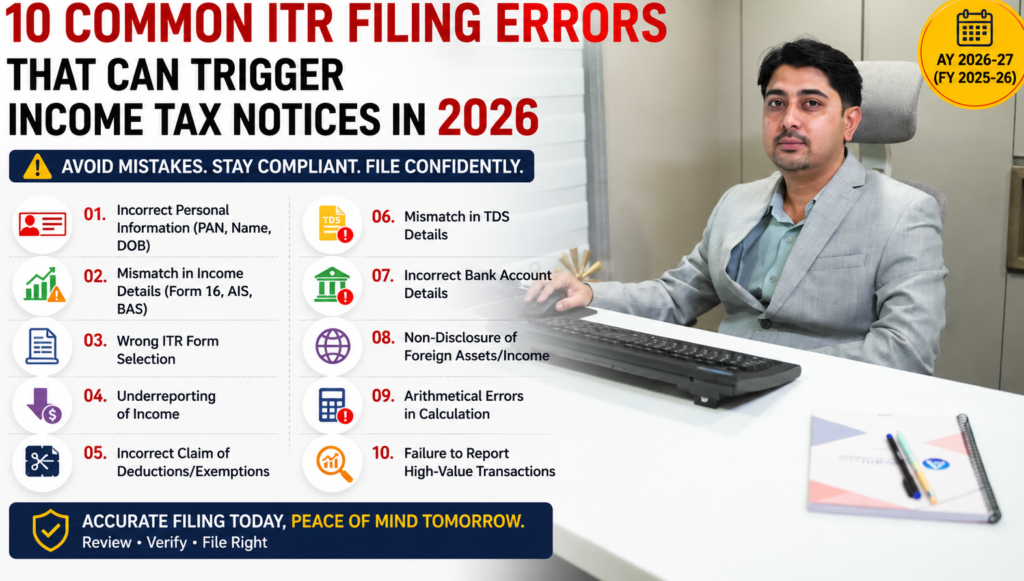

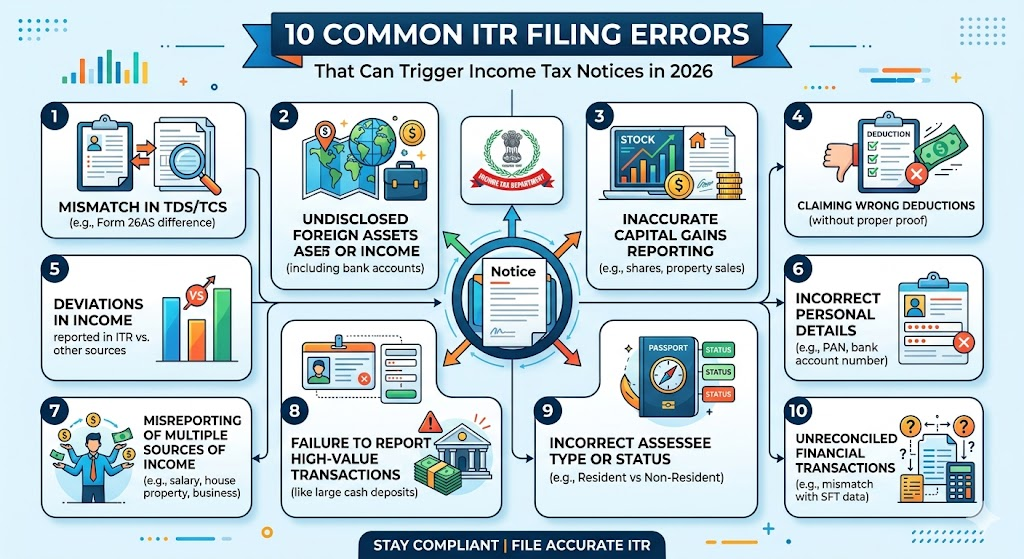

10 Common ITR Filing Errors

Filing your Income Tax Return (ITR) may appear simple, especially with pre-filled data available on the Income Tax Portal. However, thousands of taxpayers receive notices every year due to avoidable mistakes while filing their returns.

Many taxpayers believe that if tax has been deducted or Form 16 has been issued, there is no possibility of receiving a notice. Unfortunately, this is not always true.

The Income Tax Department now uses data from:

- Annual Information Statement (AIS)

- Form 26AS

- Banks

- Mutual Funds

- Stock Brokers

- Property Registrars

- Credit Card Companies

As a result, even small filing errors can result in tax demands, refund delays, scrutiny, or notices.

Let’s look at the most common ITR filing mistakes and how to avoid them.

- Not Checking AIS Before Filing

This is currently one of the biggest mistakes taxpayers make.

Many individuals file their returns using only Form 16 without reviewing the Annual Information Statement (AIS).

AIS may contain:

- FD interest

- Dividend income

- Share transactions

- Mutual fund redemptions

- Property transactions

- Foreign remittances

If income reflected in AIS is not reported in the ITR, the department may issue a notice.

Example

A salaried employee reported salary income based on Form 16 but forgot to include ₹38,000 FD interest reflected in AIS.

The mismatch was later identified during return processing.

Also Read our detailed guide on: Salary vs AIS Mismatch in Your ITR : Dangerous, Common & Completely Fixable

- Incorrect Selection of ITR Form

Using the wrong ITR form is a common mistake.

Examples:

- Using ITR 1 despite having capital gains

- Using ITR 1 despite owning foreign assets

- Using ITR 4 despite being ineligible

An incorrect form can make the return defective.

- Not Reporting Interest Income

Many taxpayers assume that because TDS has been deducted, interest income need not be reported.

This is incorrect.

Commonly missed income includes:

- Savings account interest

- Fixed Deposit interest

- Recurring Deposit interest

The income must generally be disclosed in the return.

- Ignoring Dividend Income

Dividend income received from shares and mutual funds is often forgotten during filing.

Since this information is generally available to the department, non-reporting can create mismatches.

- Incorrect Capital Gains Reporting

This is one of the most frequent reasons for notices.

Taxpayers often:

- Forget to report share transactions

- Ignore mutual fund redemptions

- Miscalculate capital gains

- Fail to report property sales

Example

A taxpayer sold mutual funds worth ₹12 lakh and assumed there was no taxable gain because the amount was reinvested.

The transaction appeared in AIS but was omitted from the ITR.

A notice was later received seeking clarification.

- Claiming Deductions Without Proper Documentation

Many taxpayers claim deductions under:

- Section 80C

- Section 80D

- Section 80G

without maintaining supporting records.

If questioned by the department, documentary evidence may be required.

- Not Reporting Foreign Assets

This mistake is particularly common among NRIs returning to India.

Foreign bank accounts, investments, and other reportable assets may require disclosure depending on residential status and applicable provisions.

Failure to disclose can have serious consequences.

- Not Reconciling Form 26AS

Before filing, taxpayers should compare:

- Form 16

- Form 26AS

- AIS

- Bank records

Differences should be investigated before submission.

- Incorrect Bank Account Details

A simple mistake in bank account information can result in:

- Refund failure

- Delayed processing

- Additional compliance issues

Always verify account details carefully.

- Filing in a Hurry Before the Deadline

Many taxpayers wait until the last few days before the due date.

As a result, important items are overlooked, including:

- AIS mismatches

- Capital gains

- Interest income

- Foreign assets

- TDS discrepancies

Rushed filing often leads to mistakes that could have been avoided.

Real-Life Example: Notice Due to AIS Mismatch

Mr. Sharma filed his Income Tax Return based solely on Form 16 provided by his employer.

A few months later, he received a communication from the Income Tax Department.

Upon review, it was found that:

- FD interest of ₹62,000 reflected in AIS was not reported.

- Dividend income of ₹14,000 was omitted.

- Mutual fund redemption transactions were not disclosed.

Although the omissions were unintentional, additional compliance was required to resolve the matter.

This situation is becoming increasingly common as the department relies heavily on AIS data.

Can I Correct an ITR Filing Mistake?

In many situations, taxpayers may be able to rectify mistakes by filing a revised return within the applicable timelines.

However, early identification of errors is important.

The longer a mistake remains uncorrected, the greater the risk of notices, demands, or penalties.

How to Avoid ITR Filing Errors:

Before filing your return:

✔️ Verify Form 16

✔️ Check AIS thoroughly

✔️ Review Form 26AS

✔️ Reconcile bank interest

✔️ Verify dividend income

✔️ Check capital gains statements

✔️ Confirm bank account details

✔️ Select the correct ITR form

✔️ Review foreign asset disclosures

✔️ Seek professional advice for complex transactions

Frequently Asked Questions

1.Can a small mistake in ITR trigger a notice?

Yes. Even small mismatches between the ITR and AIS can result in communications from the Income Tax Department.

2.Can I revise my ITR after filing?

In many cases, taxpayers can file a revised return within the prescribed timelines.

3.Is AIS more important than Form 16?

Both are important. However, AIS often contains additional information that may not appear in Form 16.

What is the most common ITR filing mistake

Currently, failure to reconcile AIS before filing is among the most common errors.

Final Thoughts

Most Income Tax notices are not issued because taxpayers intentionally hide income. They are often the result of simple mistakes, omissions, or mismatches.

A careful review of AIS, Form 26AS, interest income, capital gains, and deductions before filing can significantly reduce the risk of future notices and tax disputes.

Taking a few extra minutes before filing can save months of stress later.

Many taxpayers file their returns themselves and later discover mistakes that result in notices, refund delays, or additional tax demands.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.