Capital Gain Tax on Mutual Funds : Complete Guide for AY 2026-27

If you have invested in mutual funds and redeemed or switched units during FY 2025-26, capital gains taxation is something you cannot afford to ignore at ITR filing time.

The rules around mutual fund capital gains tax in India have changed significantly over the last two years. The Finance Act 2023 removed the indexation benefit for debt mutual funds. The Finance Act 2024 revised LTCG and STCG rates for equity funds. For AY 2026-27, understanding these updated rules is critical to accurate filing and avoiding income tax notices.

This guide explains the complete taxation framework for mutual fund capital gains covering equity funds, debt funds, hybrid funds, international funds, tax harvesting strategies, ITR reporting, and AIS compliance in plain, practical terms.

What Are Capital Gains on Mutual Funds?

When you redeem, switch, or sell mutual fund units, any profit you earn over your purchase cost (cost of acquisition) is called a capital gain. This gain is taxable under the head ‘Capital Gains’ as per the Income Tax Act, 1961.

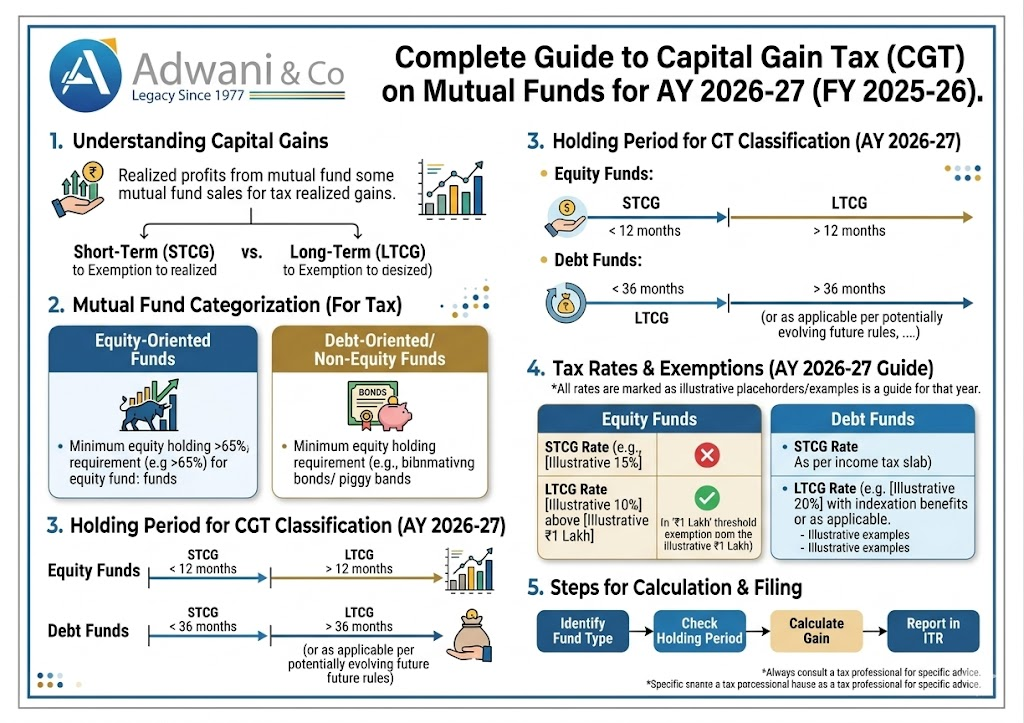

Capital gains from mutual funds are classified based on two factors:

- Type of fund : equity-oriented or non-equity (debt, international, hybrid)

- Holding period : duration from purchase date to redemption date

Importantly, switching between schemes even within the same fund house is treated as a redemption and triggers capital gains. Similarly, receiving units via dividend reinvestment can have cost and holding period implications.

Common misconception: Many investors believe that switching from a growth plan to a direct plan, or from regular to direct, is not taxable. It is. Any switch or transfer of units is a redemption in the eyes of the Income Tax Department and generates capital gains or losses.

Short-Term vs Long-Term Capital Gains: Holding Period Rules

The boundary between short-term capital gains (STCG) and long-term capital gains (LTCG) depends on the type of mutual fund.

| Fund Type | Short-Term Holding Period | Long-Term Holding Period |

| Equity Mutual Funds (equity exposure ≥65%) | 12 months or less | More than 12 months |

| Debt Mutual Funds (equity exposure <35%) | 36 months or less (old rule) All periods post Apr 2023 | More than 36 months (old rule) No LTCG benefit post Apr 2023 |

| Hybrid / Balanced Advantage Funds (equity 35%-65%) | 24 months or less | More than 24 months |

| International / Overseas Funds (equity <35%) | 24 months or less (old rule) All periods post Apr 2023 | More than 24 months (old rule) No LTCG benefit post Apr 2023 |

| Fund of Funds (domestic equity) | 12 months or less | More than 12 months |

| Gold ETFs / Gold Funds | 24 months or less | More than 24 months |

Note: Post Finance Act 2023: For debt mutual funds and overseas funds purchased on or after 1 April 2023, there is no distinction between STCG and LTCG all gains are taxed at income tax slab rates regardless of holding period.

Capital Gain Tax Rates on Mutual Funds for AY 2026-27

The Finance Act 2024 revised the capital gains tax rates applicable from 23 July 2024 onwards. These revised rates apply fully to FY 2025-26 returns filed as AY 2026-27.

Equity Mutual Funds (Equity Exposure ≥ 65%)

| Gain Type | Holding Period | Tax Rate (AY 2026-27) | Exemption Limit |

| Short-Term Capital Gain (STCG) | Up to 12 months | 20% (flat) + surcharge + cess | Nil |

| Long-Term Capital Gain (LTCG) | More than 12 months | 12.5% (flat) + surcharge + cess | Rs. 1.25 lakh per year (aggregate) |

Budget 2024 Change: STCG rate on equity was raised from 15% to 20%. LTCG rate was raised from 10% to 12.5%. The exemption limit was raised from Rs. 1 lakh to Rs. 1.25 lakh. These changes apply to transactions on or after 23 July 2024.

Debt Mutual Funds (Post 1 April 2023 Purchases)

| Purchase Date | Tax Treatment | Applicable Rate |

| Purchased before 1 April 2023 (held >36 months) | LTCG with indexation | 20% with indexation benefit |

| Purchased before 1 April 2023 (held ≤36 months) | STCG | Income tax slab rate |

| Purchased on or after 1 April 2023 (any holding period) | Taxed as ordinary income | Income tax slab rate (no indexation, no LTCG benefit) |

Note: The Finance Act 2023 removed the LTCG benefit and indexation for debt mutual funds purchased on or after 1 April 2023. This fundamentally changed debt fund tax efficiency versus fixed deposits.

Hybrid & Other Fund Categories

| Fund Category | Equity Exposure | STCG Rate | LTCG Rate | Indexation |

| Aggressive Hybrid (≥65% equity) | ≥65% | 20% | 12.5% above Rs. 1.25L | No |

| Conservative Hybrid / Debt-oriented Hybrid | <35% equity | Slab rate | Slab rate (post Apr 2023) | No (post Apr 2023) |

| Balanced Advantage Fund (35-65% equity) | 35-65% | 20% or slab | 12.5% or slab | Depends on equity exposure |

| International / Overseas Funds | Foreign equity | Slab rate | Slab rate (post Apr 2023) | No (post Apr 2023) |

| Gold ETF / Gold Fund | No equity | Slab rate (≤24 months) | 12.5% (>24 months, no indexation post 2024) | No (post 2024) |

| Fund of Funds – Domestic Equity | ≥90% in equity MFs | 20% | 12.5% above Rs. 1.25L | No |

What Is Indexation Benefit and Who Can Still Claim It?

Indexation allows you to inflate your purchase cost using the Cost Inflation Index (CII) notified by the Income Tax Department each year. This reduces your effective capital gain and therefore your tax liability.

Post the Finance Act 2024 amendments, indexation for most asset classes has been modified. For mutual funds specifically:

- Equity mutual funds: Never had indexation benefit tax at flat rates

- Debt mutual funds purchased before 1 April 2023 and held for more than 36 months: LTCG with indexation at 20% still applies grandfathered treatment

- Debt mutual funds purchased on or after 1 April 2023: No indexation, taxed at slab rates regardless of holding

- Gold funds and FoFs: Post Finance Act 2024, the 20% with indexation benefit for long-term gains has been replaced with 12.5% without indexation

| Asset Class | Pre-1 April 2023 Purchases (Long-term) | Post-1 April 2023 Purchases |

| Debt Mutual Funds | 20% with indexation (LTCG >36 months) | Slab rate, no indexation |

| International Funds | 20% with indexation (LTCG >36 months) | Slab rate, no indexation |

| Gold ETF / Gold Funds | 20% with indexation (LTCG >24 months) | 12.5% without indexation (LTCG >24 months) |

| Equity Mutual Funds | 12.5% without indexation (LTCG >12 months) | 12.5% without indexation (LTCG >12 months) |

Exemptions Available on Mutual Fund Capital Gains

Rs. 1.25 Lakh LTCG Exemption on Equity Funds

Under Section 112A of the Income Tax Act, 1961, long-term capital gains from equity-oriented mutual funds are exempt up to Rs. 1.25 lakh per financial year (aggregate across all equity assets including equity MFs, equity shares, equity ETFs, and units of business trusts).

Only gains exceeding Rs. 1.25 lakh are taxed at 12.5% (without indexation).

Example: If your total LTCG from equity mutual funds and direct equity shares combined is Rs. 2 lakh in FY 2025-26, your taxable LTCG is Rs. 75,000 (Rs. 2L minus Rs. 1.25L), taxed at 12.5% = Rs. 9,375.

Section 54F: Capital Gain Exemption on Reinvestment in Residential Property

If you redeem any long-term capital asset (including mutual fund units classified as long-term, other than a residential house) and reinvest the net consideration in purchasing or constructing a residential house property, you may claim exemption under Section 54F.

This is particularly useful for investors planning to deploy mutual fund redemption proceeds into real estate.

Section 54EE and 54EC: Bonds

Long-term capital gains from mutual funds may also qualify for exemption under Section 54EC by reinvesting up to Rs. 50 lakh in specified NHAI or REC bonds within 6 months of the sale.

Tax Loss Harvesting: A Practical Strategy for Mutual Fund Investors

Tax loss harvesting is a strategy where investors intentionally redeem loss-making mutual fund units before the financial year end (March 31) to book losses, which can then be set off against existing capital gains to reduce tax liability.

How Set-Off Rules Work Under the Income Tax Act

| Type of Loss | Can Be Set Off Against | Carry Forward Period |

| Short-Term Capital Loss (STCL) | STCG or LTCG (any asset) | 8 years |

| Long-Term Capital Loss (LTCL) | LTCG only (same or different asset) | 8 years |

| Business Loss | Business income only (not capital gains) | 8 years |

| Speculative Loss | Speculative income only | 4 years |

Key Insight: You can set off your short-term capital losses from poorly performing debt funds against long-term capital gains from equity funds. This cross-asset, cross-category set-off is allowed under the Income Tax Act and is a powerful planning tool.

Tax Harvesting in Practice: Example

Situation: Aditya has LTCG of Rs. 3 lakh from equity mutual funds in FY 2025-26. He also has STCL of Rs. 1.5 lakh from an international fund that has underperformed.

- Taxable LTCG before set-off = Rs. 3 lakh

- Less: LTCG exemption = Rs. 1.25 lakh

- Taxable LTCG after exemption = Rs. 1.75 lakh

- Less: STCL set-off = Rs. 1.5 lakh

- Net taxable LTCG = Rs. 25,000

- Tax at 12.5% = Rs. 3,125 (versus Rs. 21,875 without harvesting)

AIS, Form 26AS and Mutual Fund Capital Gains: Reporting Obligations

The Annual Information Statement (AIS) on the Income Tax portal now captures all mutual fund transactions reported by RTAs (Registrar and Transfer Agents) such as CAMS and KFintech. This includes purchases, redemptions, switches, SIP and SWP transactions, and dividend payouts.

Why AIS Mismatches in Mutual Funds Are a Common Notice Trigger

If your ITR does not reflect the capital gains shown in your AIS, the Income Tax Department’s automated system flags this discrepancy. This is one of the most common reasons salaried individuals who also have mutual fund investments receive notices under Section 143(1)(a) or Section 142(1).

Common causes of AIS mismatch for mutual fund investors:

- Not reporting gains from old folio numbers or dormant accounts

- Switching between direct and regular plans without reporting the resulting gain

- Not accounting for reinvested dividends (growth option vs IDCW option confusion)

- Not including gains from ELSS fund redemptions after 3-year lock-in

- Joint holding gains reported under the first holder’s PAN in AIS

How to Download Your Capital Gain Statement

- Log in to CAMS (camsonline.com) or KFintech (kfintech.com) with your PAN and email

- Navigate to ‘Capital Gain Statement’ under the Reports section

- Select the financial year FY 2025-26 (1 April 2025 to 31 March 2026)

- Download the statement and verify it matches your AIS on incometax.gov.in

- For SIPs, each SIP instalment has a different purchase date and cost ensure all are captured

Which ITR Form to Use for Mutual Fund Capital Gains in AY 2026-27?

| Taxpayer Profile | Correct ITR Form |

| Salaried with only equity MF LTCG (no other capital assets, LTCG ≤Rs. 1.25L) | ITR-1 (Sahaj) — if total income ≤Rs. 50L |

| Salaried with any capital gains (STCG or LTCG exceeding basic limits) | ITR-2 |

| Business income + capital gains from MFs | ITR-3 |

| Presumptive taxation professionals (44ADA) + capital gains from MFs | ITR-3 (not ITR-4, since ITR-4 cannot report capital gains) |

| NRI with Indian mutual fund redemptions | ITR-2 |

| Company or LLP | ITR-6 or ITR-5 as applicable |

How to Report Mutual Fund Capital Gains in ITR-2

- Go to Schedule CG (Capital Gains) in ITR-2

- Equity MF LTCG report under ‘Section 112A’ in Schedule 112A (scrip-wise details required)

- Equity MF STCG report under ‘Section 111A’

- Debt MF / other MF gains report under ‘Short-Term Capital Gains taxable at applicable rate’ or LTCG under Section 112

- Set-off and carry forward report in Schedule CYLA, BFLA, and CFL

- Use the pre-filled data but always verify against your capital gain statement

TDS on Mutual Fund Redemptions and Dividends

TDS on Mutual Fund Dividends (IDCW)

Under Section 194K of the Income Tax Act, mutual fund houses deduct TDS at 10% on dividend (IDCW) income paid to resident individuals if the aggregate dividend in a financial year exceeds Rs. 5,000. This TDS is reflected in Form 26AS and AIS.

TDS on Redemptions by NRIs

For NRI investors, mutual fund redemptions attract TDS as follows:

| Fund Type | STCG TDS Rate for NRI | LTCG TDS Rate for NRI |

| Equity Mutual Funds | 20% (was 15% pre-Budget 2024) | 12.5% (above Rs. 1.25L exemption) |

| Debt Mutual Funds (post Apr 2023) | Slab rate / 30% for NRIs | No separate LTCG — slab rate |

| Other Non-Equity Funds | Applicable slab rate / 30% | 20% with indexation (pre-Apr 2023 purchases) |

The Grandfathering Rule: Equity Mutual Funds Held Before 31 January 2018

When the government reintroduced LTCG tax on equity mutual funds through the Finance Act 2018, it provided a grandfathering benefit. Gains accrued in equity mutual funds up to 31 January 2018 were protected from taxation.

If you are still holding equity mutual fund units purchased before 31 January 2018, your cost of acquisition for tax purposes is the higher of:

- Your actual purchase price

- The NAV (Net Asset Value) of the fund on 31 January 2018

This effectively means that all gains up to 31 January 2018 are tax-free under LTCG. Only gains post that date are taxable at 12.5%.

If you have very old mutual fund folios with units purchased before 2018, your capital gain statement will reflect this grandfathering cost automatically. Ensure your ITR filing uses the correct grandfathered cost basis.

ELSS Mutual Funds: Tax Deduction + Capital Gains Taxation

Equity Linked Savings Schemes (ELSS) offer a dual tax benefit deduction under Section 80C (up to Rs. 1.5 lakh) on investment, and long-term capital gains treatment on redemption after the mandatory 3 year lock in.

| Aspect | ELSS Details |

| Lock-in period | 3 years from each SIP instalment date |

| Section 80C deduction | Up to Rs. 1.5 lakh per year (under old tax regime only) |

| LTCG tax rate on redemption | 12.5% above Rs. 1.25 lakh (same as equity funds) |

| STCG possibility | No lock-in ensures minimum 3-year holding (>12 months = LTCG) |

| Reporting in ITR | Schedule 112A under Capital Gains scrip-wise detail needed |

| Applicable ITR form | ITR-2 or ITR-3 (not ITR-1 or ITR-4) |

| 80C deduction new regime | Not available Section 80C deductions not applicable under new tax regime |

Common Mistakes Mutual Fund Investors Make in ITR Filing

- Filing ITR-1 or ITR-4 despite having capital gains from mutual funds leads to defective return notice

- Not reporting ELSS redemptions treated as income not disclosed, can trigger scrutiny

- Not matching AIS with capital gain statement before filing AIS mismatches trigger Section 143(1)(a) notices

- Missing gains from SWP (Systematic Withdrawal Plans) each SWP withdrawal is a partial redemption taxable as capital gain

- Ignoring dividend (IDCW) income taxable at slab rate, must be reported under ‘Income from Other Sources’

- Not reporting losses losses eligible for carry forward are forfeited if not claimed in ITR

- Treating all mutual fund gains as LTCG STCG from equity funds held under 12 months is taxed at 20%, not 12.5%

- Not accounting for SIP-wise holding period each SIP instalment has its own purchase date; gains from instalments held <12 months are STCG

Practical Examples: Calculating Mutual Fund Capital Gains Tax for AY 2026-27

Example 1 : Salaried Investor with Equity MF Redemption

Ramesh is a salaried individual earning Rs. 10 lakh per year. In FY 2025-26, he redeemed equity mutual fund units with total LTCG of Rs. 2 lakh and STCG of Rs. 30,000.

| Capital Gain Component | Amount | Tax Rate | Tax Payable |

| LTCG from equity MFs | Rs. 2,00,000 | 12.5% above Rs. 1.25L exemption | Rs. 9,375 on Rs. 75,000 |

| STCG from equity MFs | Rs. 30,000 | 20% | Rs. 6,000 |

| Total MF Capital Gain Tax | Rs. 15,375 |

Example 2 : Debt Fund Investor (Post April 2023 Purchase)

Sunaina purchased debt mutual fund units in June 2023 for Rs. 5 lakh. She redeemed them in December 2025 for Rs. 5.8 lakh (gain of Rs. 80,000). She falls in the 30% tax bracket.

- No LTCG benefit purchased after 1 April 2023

- No indexation benefit

- Rs. 80,000 added to total income and taxed at 30% slab = Rs. 24,000

- Had she purchased this before 1 April 2023 and held for >36 months LTCG with indexation at 20% could have been applicable

Example 3 : SIP with Mixed LTCG and STCG

Priya runs a monthly SIP of Rs. 10,000 in an aggressive hybrid fund (equity ≥65%) since April 2023. She redeemed all units in May 2025.

- SIP instalments from April 2023 to April 2024 (13 months or more by May 2025): LTCG at 12.5%

- SIP instalments from May 2024 to April 2025 (held <12 months by May 2025): STCG at 20%

- Her capital gain statement from CAMS will split this automatically she should not manually aggregate

Key Takeaways

- Equity mutual funds: LTCG at 12.5% above Rs. 1.25 lakh (>12 months); STCG at 20% (≤12 months) Finance Act 2024 rates

- Debt mutual funds purchased after 1 April 2023: taxed at slab rates no LTCG, no indexation benefit

- Debt funds purchased before 1 April 2023: LTCG with indexation at 20% still applicable if held >36 months

- Switch, SWP, and plan change transactions are taxable redemption events often missed by investors

- Tax loss harvesting before 31 March can significantly reduce net capital gains tax liability

- Short-term losses from any capital asset can be set off against both STCG and LTCG

- AIS on the Income Tax Portal captures all MF transactions mismatches trigger notices

- File ITR-2 or ITR-3 for capital gains not ITR-1 or ITR-4

- NRIs face TDS at source on MF redemptions and must file ITR to claim excess TDS refunds

- For SIP investments, each instalment has its own holding period and cost use the capital gain statement from CAMS/KFintech

Frequently Asked Questions (FAQs)

Q1. What is the LTCG tax rate on equity mutual funds for AY 2026-27?

Long-term capital gains from equity mutual funds for AY 2026-27 are taxed at 12.5% (without indexation) on gains exceeding Rs. 1.25 lakh in a financial year. This rate was revised upward from 10% by the Finance Act 2024, effective from 23 July 2024. LTCG up to Rs. 1.25 lakh is fully exempt.

Q2. What is the STCG tax rate on equity mutual funds for AY 2026-27?

Short-term capital gains from equity mutual funds where units are held for 12 months or less are taxed at a flat rate of 20% under Section 111A of the Income Tax Act. The Finance Act 2024 revised this rate from 15% to 20%, applicable from 23 July 2024.

Q3. Is there any exemption on capital gains from equity mutual funds?

Yes. Under Section 112A, LTCG from equity-oriented mutual funds is exempt up to Rs. 1.25 lakh per financial year in aggregate (including gains from equity shares, equity mutual funds, and equity ETFs). Only the amount exceeding Rs. 1.25 lakh is taxed at 12.5%. There is no exemption for STCG from equity mutual funds.

Q4. Is dividend (IDCW) from mutual funds taxable?

Yes. Dividend income from mutual funds now called IDCW (Income Distribution cum Capital Withdrawal) is taxable in the hands of the investor at their applicable income tax slab rate under ‘Income from Other Sources’. Mutual fund houses deduct TDS at 10% under Section 194K if aggregate dividend in a financial year exceeds Rs. 5,000 for resident individuals. This TDS appears in Form 26AS.

Q5. How are NRI investments in Indian mutual funds taxed?

NRIs with investments in Indian mutual funds are subject to the same capital gains tax rates as resident investors, but TDS is deducted at source by the mutual fund house. For equity funds, TDS on STCG is 20% and on LTCG is 12.5%. For debt funds, TDS is at applicable rates. NRIs should file their Indian ITR to reconcile actual tax liability against TDS deducted and claim refunds if excess TDS has been deducted.

Conclusion:

Mutual fund capital gains taxation in India has gone through some of its most significant changes in recent memory the Finance Act 2023 and Finance Act 2024 together rewrote the rules for both equity and debt funds. For AY 2026-27, investors need to be particularly careful about the revised LTCG and STCG rates for equity funds, the slab-rate treatment of new debt fund investments, and the correct ITR form to use.

The good news is that with proper planning tax loss harvesting, use of the Rs. 1.25 lakh LTCG exemption, set-off of losses, and timely filing the overall tax outgo from mutual fund investments can be optimised legally.

The starting point is always the capital gain statement from your RTA (CAMS or KFintech), reconciled carefully against your AIS. Do this before your ITR filing, not after a notice arrives.

File on time, report accurately, and claim every benefit you are entitled to. If your portfolio has multiple fund types, SIPs, and switches, professional guidance ensures you don’t leave money on the table — or face unnecessary scrutiny.

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

bout the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra.