Received a Credit Card Income Tax Notice? Here’s the Ultimate Guide to Protect Yourself in 2025

CA Dipesh Gurubakshani April 2026 11 min read

If your total credit card payments in a financial year crossed ₹10 lakh, there is a very real possibility that your bank has already reported it to the Income Tax Department. And if that number does not reconcile with your declared income, a credit card income tax notice could be headed your way or may have already arrived.

This guide, crafted with insights from Dr. Haresh Adwani a distinguished tax advisor and financial strategist — breaks down exactly how these notices are generated, what legal provisions apply, and most importantly, what you must do right now to protect yourself.

What Is a Credit Card Income Tax Notice and Why Should You Care?

A credit card income tax notice is an official communication from the Income Tax Department of India asking you to explain the source of funds behind your credit card payments. It is not an accusation of wrongdoing but it is a formal legal demand that requires a structured, documented response.

The notice is triggered when the department’s automated systems identify a mismatch between what you earn (as declared in your Income Tax Return) and what you spend (as reported by your bank under the Statement of Financial Transactions framework). In simple terms: if your spending story does not match your income story, the tax department wants an explanation.

According to the Income Tax Department of India (www.incometax.gov.in), the Annual Information Statement (AIS) is a comprehensive financial dossier that includes details of every significant financial transaction including credit card payments made during a financial year.

The key threshold you must know: any aggregate credit card payment exceeding ₹10 lakh in a single financial year is mandatorily reported. This single data point can become the starting point of an unwanted tax scrutiny.

How the Income Tax Department Tracks Your Credit Card Spending

The Statement of Financial Transactions (SFT) Your Bank’s Report Card to the Government

Under Rule 114E of the Income Tax Rules, 1962, every bank and credit card company is legally required to submit a Statement of Financial Transactions (SFT) to the Income Tax Department. This is not optional — it is a statutory obligation.

The SFT captures the following information about your credit card usage:

- Total credit card bill payments during the financial year (if aggregate exceeds ₹10 lakh)

- Cash payments of ₹1 lakh or more made against credit card dues in a single transaction

- Any high-value single credit card payment exceeding ₹10 lakh

Once the SFT is filed, this data is automatically reflected in your Annual Information Statement (AIS), which you can view on the Income Tax e-Filing Portal. When you file your ITR, the system cross-checks these figures with your declared income and if a significant mismatch is found, your profile is flagged for scrutiny.

Your Annual Information Statement: What the Tax Department Sees About You

Many taxpayers are unaware of just how comprehensive their AIS is. Log into the Income Tax e-Filing Portal and navigate to the AIS section you will find a detailed record of your financial activity including savings account interest, dividends, property transactions, foreign remittances, stock market trades, mutual fund redemptions, and yes your credit card payments.

Dr. Haresh Adwani regularly advises clients to review their AIS before filing their ITR every year. “The AIS tells you exactly what story the government has already built about your finances. Your ITR should reconcile with that story not contradict it,” he notes.

The failure to reconcile these two data points is what triggers most credit card income tax notices in India today.

The Triggers: What Makes a Credit Card Income Tax Notice Land in Your Inbox?

1. Payments Significantly Exceeding Declared Income

The most straightforward trigger. If your declared annual income is ₹7 lakh but your credit card payments total ₹13 lakh, the department’s algorithm flags a ₹6 lakh unexplained gap. This gap — unless satisfactorily explained with documentation — can be treated as unexplained expenditure under Section 69C of the Income Tax Act.

2. Cash Payments Against Credit Card Bills

Paying your credit card bill in cash is a significant red flag. The SFT reporting mechanism specifically captures cash payments of ₹1 lakh or more against credit card dues. Cash transactions are inherently difficult to trace, which is why the department treats them with heightened suspicion.

3. High-Value Individual Purchases

Even if your overall annual spending is within limits, a single large purchase — say, a ₹5 lakh piece of jewellery, a luxury appliance, or an international business-class flight — can trigger specific scrutiny if not proportionate to your known income.

4. Inconsistency Across Multiple Financial Instruments

The Income Tax Department’s Project Insight initiative uses advanced data analytics to cross-reference multiple financial data points simultaneously. If your credit card spending, bank deposits, property registrations, and investment patterns collectively suggest a lifestyle inconsistent with your declared income, the risk of receiving a credit card income tax notice multiplies significantly.

Quick Reference: Credit Card Payments and Tax Risk

| Scenario | Threshold | Reporting Required | Tax Risk |

| Annual credit card payments | Above ₹10 lakh | Yes (SFT by bank) | High : AIS mismatch likely |

| Cash payment vs. credit card bill | Above ₹1 lakh (single) | Yes (SFT) | Medium,High : red flag |

| No explanation for excess spend | Any amount flagged | N/A | Very High:Section 69C applies |

| Third-party card usage (undocumented) | Any amount | N/A | Medium:burden of proof on taxpayer |

Section 69C of the Income Tax Act: The Law That Can Cost You 78% in Taxes

This is the provision that gives most taxpayers sleepless nights — and rightly so. Section 69C of the Income Tax Act, 1961 deals with ‘unexplained expenditure.’ If the Assessing Officer finds that you have incurred an expenditure that you cannot satisfactorily explain, and the source of that expenditure is not disclosed in your return, the entire amount can be deemed as income and taxed at a punishing rate.

How much tax under Section 69C? The income deemed under Section 69C is taxed at a flat rate of 60% under Section 115BBE, plus a 25% surcharge on the tax amount, plus 4% health and education cess. The effective tax rate comes out to approximately 78%. Add interest under Section 234A/234B and penalties under Section 271AAC (up to 10% of the undisclosed income), and you can see why this provision is so feared.

A Numerical Example to Understand Section 69C Better

Let us consider a real-world scenario that the team at itradvisor.in frequently encounters:

| Parameter | Amount |

| Declared Annual Income | ₹9,00,000 |

| Total Credit Card Payments (FY) | ₹17,50,000 |

| Unexplained Difference | ₹8,50,000 |

| Tax @ 60% under Sec 115BBE | ₹5,10,000 |

| Surcharge @ 25% of tax | ₹1,27,500 |

| Cess @ 4% | ₹25,500 |

| Total Tax Demand (approx.) | ₹6,63,000 |

| Penalty under Sec 271AAC (10%) | ₹85,000 |

| TOTAL LIABILITY (approx.) | ₹7,48,000 |

This example illustrates why a credit card income tax notice is not something to take lightly. On a seemingly routine spending pattern, the potential tax liability can wipe out years of savings.

The Most Common Real-Life Scenarios That Trigger a Credit Card Income Tax Notice

Scenario 1: Entire Family Sharing One Credit Card

This is India’s most common household financial arrangement — a single primary credit card used by the entire family. Your spouse shops online, your parents pay medical bills, your children book their tuition fees all on your card. The result? A total annual payment figure that is completely disproportionate to your personal income. The fix is simple but often neglected: always collect reimbursements via bank transfer (UPI or NEFT), never cash. A ₹500 UPI transfer creates a permanent, timestamped digital record. Cash repayment leaves no trace.

Scenario 2: Routing Business Expenses Through a Personal Card

Freelancers, consultants, and small business owners commonly use personal credit cards for client entertainment, travel, software subscriptions, and office supplies. This is perfectly legal — but it creates a documentation nightmare when the department asks you to explain your spending. Maintain a detailed monthly categorisation of every business transaction on your personal card. Ideally, open a separate business credit card. This clean separation is among the top recommendations that Dr. Haresh Adwani makes to self-employed clients.

Scenario 3: High-Frequency Reward Point Optimisation

Financially savvy individuals often route every possible payment insurance premiums, utility bills, mutual fund SIPs, rent through credit cards to maximise cashback and reward points. There is absolutely nothing wrong with this strategy. But it can push annual payments well above ₹10 lakh even for moderate earners. The key safeguard: ensure your ITR fully discloses all income streams including interest income, rental income, capital gains, and freelancing earnings so that the total outflow figure is proportionately justified.

Scenario 4: Friends Swiping and Repaying

Group travel bookings, shared dinners, joint purchases these are common in urban India. But when a friend swipes your card for ₹1.5 lakh and returns the money in cash two days later, that ₹1.5 lakh becomes part of your reported credit card payments with no corresponding income source on record. The rule is non-negotiable: always insist on digital transfers for reimbursements. The convenience of cash is not worth the documentation risk.

Scenario 5: High-Value EMI Purchases

When you buy a ₹1.8 lakh laptop or a ₹3 lakh television on EMI, the entire purchase amount may appear as a single lump-sum in the SFT report even though you are repaying it over 24 months. This single entry can significantly skew the apparent gap between your income and expenditure. Keep purchase invoices, EMI conversion letters, and bank statements as supporting evidence. These documents can instantly clarify the nature of the transaction if a notice arrives.

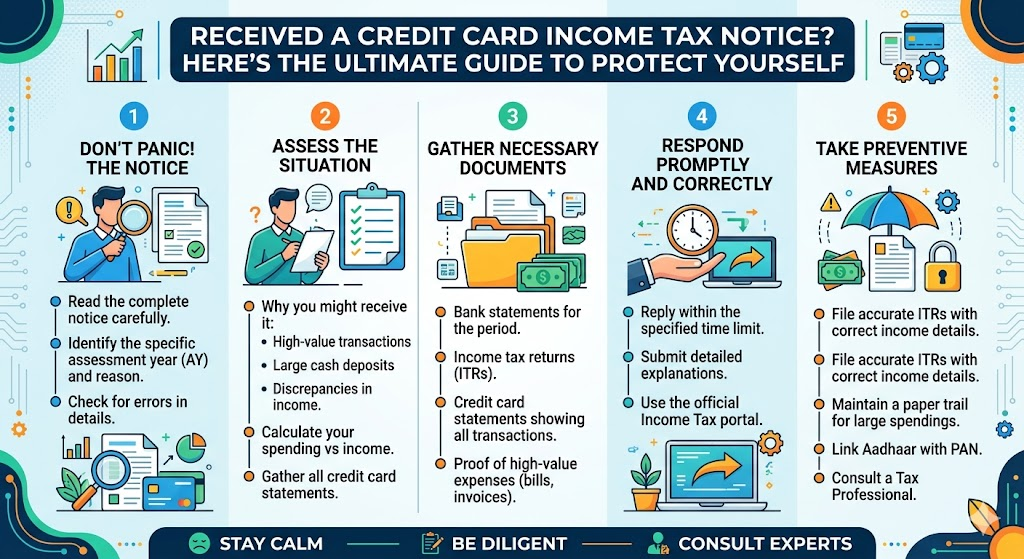

7 Powerful Steps to Protect Yourself From a Credit Card Income Tax Notice

- Track your annual credit card payments actively. If you are nearing ₹8–9 lakh in a financial year, start maintaining a detailed transaction log immediately.

- Review your Annual Information Statement (AIS) on the Income Tax e-Filing Portal before filing your ITR. Reconcile every figure. If anything appears incorrect, raise a dispute on the portal itself the department allows you to flag inaccurate SFT data.

- Collect all reimbursements digitally. Bank transfers and UPI payments create an automatic, permanent paper trail. Never accept cash repayments for shared card usage.

- Disclose all income sources in your ITR including savings bank interest, fixed deposit interest, rental income, capital gains, and any freelancing revenue. Even small undisclosed income can be the critical gap that makes your credit card spending look suspicious.

- Separate business and personal credit cards. If you are a business owner or self-employed professional, this is a compliance imperative, not merely a best practice.

- Perform a pre-filing income-vs-expenditure reconciliation. Total your credit card payments, EMIs, rent, and cash withdrawals. If the sum exceeds your declared income, identify the funding source and document it before the department asks.

- Consult a qualified tax advisor before filing especially if your annual credit card payments are above ₹10 lakh. A proactive review is far less costly than responding to a scrutiny notice.

For professional guidance on income tax compliance and credit card tax planning, explore the advisory services available at itradvisor.in — your trusted destination for expert tax and financial advice.

Already Received a Credit Card Income Tax Notice? Here’s Your Immediate Action Plan

If the notice has already arrived, do not panic but also do not delay. Here is what you need to do:

- Read the notice carefully. Identify under which section it is issued Section 142(1) (seeking information), Section 148 (reassessment), or another assessment-related provision. Each has a different timeline and response requirement.

- Compile all relevant documents immediately: credit card statements, bank statements, UPI transaction histories, purchase invoices, family member declarations (if applicable), and employer or business income certificates.

- Prepare a detailed reconciliation statement that maps every major credit card payment to its source of funds. The cleaner and more organised this document, the stronger your case.

- Engage a qualified Chartered Accountant with experience in income tax assessment proceedings. A poorly drafted response can escalate a straightforward notice into a full-scale assessment.

- Submit the response within the stipulated deadline. Missing the deadline can result in ex-parte assessment — the department proceeding in your absence, which rarely works in the taxpayer’s favour.

Dr. Haresh Adwani emphasises that most credit card income tax notice cases are resolvable at the first response stage itself, provided the taxpayer has maintained even basic documentation. “The department is not trying to punish honest taxpayers,” he explains. “It is trying to identify undisclosed income. If you can show that your spending is justified, the matter ends there.”

Learn more about our Income Tax Notice Response Services and how we help taxpayers navigate scrutiny with confidence.

https://www.adwaniandco.com/blog/section148-notice-how-to-reply

India’s Financial Surveillance Framework: Understanding the Full Picture

The credit card income tax notice is just one manifestation of a much broader shift in how the Indian government monitors financial activity. Over the past decade, the Income Tax Department has built a sophisticated, multi-layered data intelligence ecosystem:

- Project Insight: A data analytics initiative that aggregates and analyses financial data from banks, registrars, market intermediaries, and more to identify tax non-compliance

- Faceless Assessment Scheme: All tax assessments are now conducted digitally, with no personal interaction making the process data-driven and algorithm-dependent

- Annual Information Statement (AIS): A comprehensive financial profile accessible to both the taxpayer and the department

- GST Return Cross Matching: For business owners, GST turnover declared on the GST Portal (www.gst.gov.in) is routinely cross-checked with ITR income declarations

- MCA Filings: Directors and shareholders of companies have their financial profiles cross-referenced with MCA data via the Ministry of Corporate Affairs portal (www.mca.gov.in)

In this environment, financial transparency is no longer optional it is the only viable strategy. The taxpayers who maintain clean, well documented financial records are the ones who sleep soundly when notices arrive.

Also Read

https://www.adwaniandco.com/services/taxation-compliance

Conclusion:

In today’s digitally surveilled tax environment, every credit card swipe creates a data point. When those data points collectively suggest a mismatch with your declared income, the Income Tax Department’s algorithms will take notice literally.

A credit card income tax notice is not a verdict of guilt. It is a data-driven question from the government: “Can you explain your spending?” For taxpayers who maintain clean records, reconcile their finances proactively, and declare all sources of income, the answer is straightforward. For those who do not, the consequences as Section 69C demonstrates can be financially devastating.

The solution is not complicated. Track your credit card payments against your declared income. Collect digital proof for all shared card usage. Review your AIS before filing your ITR. Declare all income. And when in doubt, consult a qualified tax professional before the notice arrives not after.

Dr. Haresh Adwanileaves us with this: “The cost of organised documentation is a few hours a year. The cost of disorganised finances is years of legal stress and lakhs in tax liability. The choice is yours — and it is an easy one.”

Frequently Asked Questions

Q1. What is the SFT limit for credit card payments that triggers reporting to the Income Tax Department?

Any aggregate credit card payment exceeding ₹10 lakh during a single financial year is mandatorily reported to the Income Tax Department by your bank or card issuer under Rule 114E. Additionally, any cash payment of ₹1 lakh or more made against a credit card bill is also separately reported.

Q2. Can I get a credit card income tax notice if my income is declared correctly?

Yes, you can. A notice is triggered by a mismatch between your declared income and your reported credit card payments not necessarily by undeclared income. If your spending appears disproportionate to your income, the department may seek an explanation even if your returns were filed correctly. This is why income-expenditure reconciliation before filing is critical.

Q3. What happens under Section 69C if I cannot explain my credit card spending?

Under Section 69C of the Income Tax Act, 1961, any expenditure that cannot be satisfactorily explained may be deemed as income. This income is then taxed at 60% under Section 115BBE, plus a 25% surcharge and 4% cess resulting in an effective tax rate of approximately 78%. Penalties under Section 271AAC can add a further 10% of the undisclosed income.

Q4. Is it illegal for family members to use my credit card?

It is not illegal, but it creates a documentation challenge. Since the card is issued in your name, all payments are attributed to your financial profile. If the department questions the spending, you must prove that others used the card and reimbursed you. Always ensure reimbursements are made via digital transfers (UPI/NEFT) rather than cash.

Q5. How do I check if my credit card payments have been reported in my AIS?

Log in to the Income Tax e-Filing Portal (www.incometax.gov.in), go to ‘Services’, then ‘Annual Information Statement (AIS)’. Under the SFT section, you will find details of credit card payments reported against your PAN. Review this before filing your ITR every year.

Q6. Can I dispute incorrect credit card payment data in my AIS?

Yes. The Income Tax e-Filing Portal allows taxpayers to submit feedback on AIS data. If you believe the reported credit card payment figure is incorrect for example, if it reflects payments made by another cardholder on an add-on card you can raise a dispute directly on the portal, and the information will be sent back to the reporting entity (your bank) for verification.

Q7. How many years back can the Income Tax Department send a credit card income tax notice?

Generally, the department can reopen assessments up to 3 years from the end of the relevant assessment year for regular cases. In cases where the escaped income exceeds ₹50 lakh, this period can extend up to 10 years. Maintaining documentation for at least 7 years is a prudent practice.

Author

CA.Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services.

Whether you have already received a credit card income tax notice or want to ensure you never do — Adwani and Company is your trusted partner. Led by Dr. Haresh Adwani and a seasoned team of Chartered Accountants, Adwani and Company provides end-to-end income tax compliance, notice response, and financial planning services.

Visit: www.adwaniandco.com | Call: +91 7620 127 137 | Email: enquiries@adwaniandco.com