GST Compliance Checklist India 2026: 7 Essential Rules to Avoid Notices and Penalties

Introduction: GST Compliance Is Not a Once a Year Exercise

India’s GST system governed by the CGST Act 2017, IGST Act 2017, and SGST laws operates on a multi-rate structure (5%, 12%, 18%, 28%) with mandatory monthly and quarterly filings, automated data matching, and increasing use of AI-powered scrutiny tools by the GSTN. In 2026, a compliance gap that might have gone unnoticed three years ago now triggers an automated show cause notice within weeks.

This guide authored by Dr. Haresh Adwani, a GST practitioner with over 20 years of advisory experience provides the 7 compliance rules every GST registered business must follow, a complete filing schedule, and a practical framework for staying penalty free in FY 2026-27.

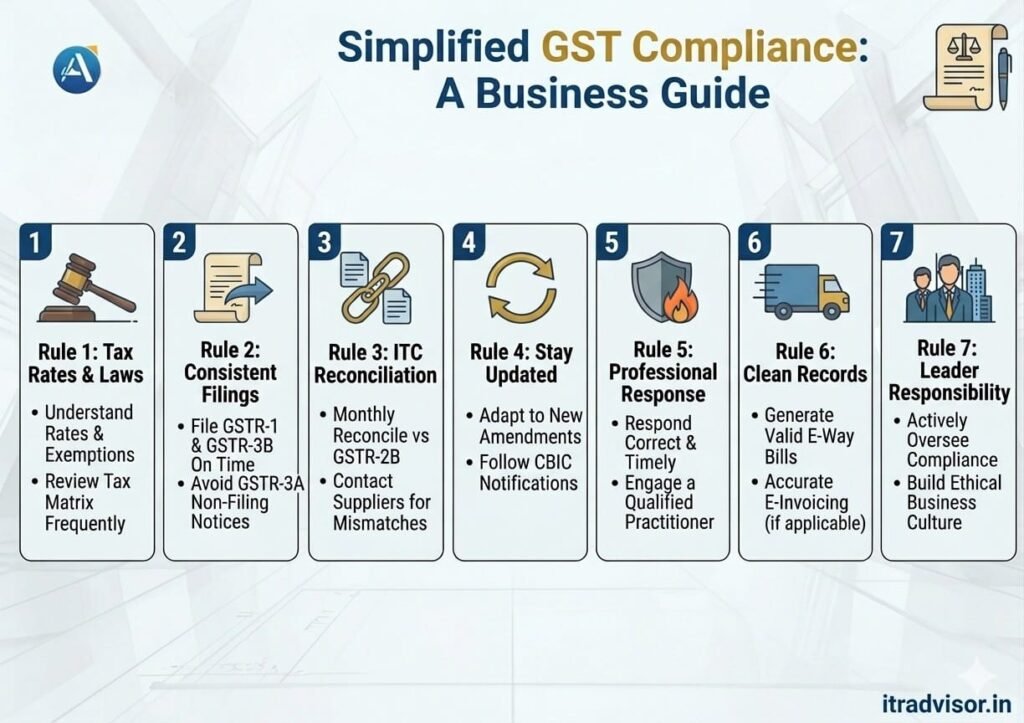

Rule 1: Know the Law Understand GST Rates, Exemptions, and ITC Rules

The most powerful defence against a GST Show Cause Notice (SCN) is understanding the law better than the notice that arrives. Businesses must correctly identify which GST rate applies to their specific goods or services, which exemptions under CGST notifications apply, and what Input Tax Credit (ITC) conditions must be satisfied under Sections 16 and 17.

Incorrect rate application for example, charging 12% on a service that should attract 18%, or incorrectly claiming the healthcare exemption on a taxable service is one of the most common automated notice triggers in 2026. Build a product/service tax matrix for your business and review it every time the GST Council issues notifications.

Rule 2: Consistency File Returns on Time, Every Filing Period Without Exception

GST compliance is built on consistent, on-time filing of GSTR-1, GSTR3B, GSTR9, and GSTR9C. A single missed filing cascades into data mismatches, ITC blocks for your buyers, automated GSTR-3A non-filing notices, and GSTIN suspension risk.

| Practical Example On-Time Filing Value A Mumbai textile trader with Rs. 25 lakh monthly turnover pays approximately Rs. 4.5 lakh in GST per month. Consistent on-time filing avoids: late fees of Rs. 50 per day per return (Rs. 20 for Nil returns), 18% p.a. interest on unpaid tax, GSTIN suspension, and downstream ITC denial for buyers. One missed GSTR-3B can cascade into mismatches, demand notices, and interest liability. Consistency is your lowest-cost compliance strategy. |

Rule 3: Team Coordination Reconcile Your ITC Against GSTR-2B Every Month

Your ITC claims in GSTR3B must reconcile with the auto-populated GSTR-2B data on the GST portal. Any gap whether because a supplier has not filed GSTR1, filed it late, or reported an incorrect invoice triggers automated discrepancy notices under Section 61 of the CGST Act.

Monthly reconciliation between your purchase register, GSTR-2B data, and GSTR3B filings is the single most effective habit to prevent ITC-related demand notices before they are issued. Where a supplier has consistently not filed, consider reversing provisional ITC under Section 16(2) to eliminate the mismatch risk.

Rule 4: Adapt Stay Current with GST Amendments, Notifications, and Circulars

Since GST’s implementation in July 2017, the legal landscape has evolved continuously rate changes, new notifications, CBIC circulars, Advance Ruling Authority (AAR) decisions, and Supreme Court judgments all affect your GST liability. Businesses that apply outdated rates or expired exemptions face demand notices for the differential tax plus interest.

Subscribe to CBIC notification alerts, track GST Council recommendations, and review your tax matrix every time a major notification is issued. Adwani & Company maintains a live amendment tracker for all advisory clients.

Rule 5: Perform Under Pressure Respond to GST Notices Correctly and on Time

Receiving a GST Show Cause Notice is a high-pressure moment for any business. The correct response requires: filing within the stipulated timeline, addressing each allegation individually with documentary evidence, citing the applicable legal provisions and CBIC circulars, referencing favourable High Court and Tribunal judgments, and where genuine liability exists opting for voluntary payment with interest to reduce penalty exposure under Section 73.

Ignoring a GST notice results in an ex-parte demand order. Panic driven incomplete responses worsen your position. Engage a qualified GST practitioner immediately upon receiving any show cause notice or DRC-01A pre-notice intimation.

Rule 6: Build Infrastructure E Way Bills, E Invoicing, and Clean Audit Trails

GST compliance infrastructure the systems that generate and archive e way bills, e invoices, and accounting records is not optional. The stakes are high:

- E-way bill violations (goods movement above Rs. 50,000 without a valid e-way bill) attract a penalty equal to 100% of the tax due on the consignment.

- E-invoicing is mandatory for all registered taxpayers with aggregate turnover above Rs. 5 crore in any financial year from FY 2017-18 onwards. Lapses lead to ITC denial for your buyers damaging your commercial relationships.

- A clean, reconcilable accounting system that generates audit trails matching your GST returns is your primary defence in any scrutiny or audit.

Rule 7: Leadership GST Accountability Starts at the Top

Under Section 89 of the CGST Act, every person in charge of the conduct of business directors, partners, and the karta of HUFs can be held personally liable for the entity’s GST dues in cases of non-compliance. GST compliance is not solely the accountant’s responsibility; it begins with the business owner and promoter.

Businesses where leadership treats GST compliance as an operational priority not an annual afterthought consistently avoid notices, penalties, and business disruption.

Also Read:

https://itradvisor.in/blog/gst-show-cause-notice-2026https://itradvisor.in/blog/gst-show-cause-notice-2026

GST Filing Mistakes Businesses Must Eliminate in 2026

| Common Mistake | Consequence | Prevention |

| Incorrect GST rate application | Tax demand + interest + penalty | Build and maintain a product/service tax matrix |

| GSTR-1 vs GSTR-3B mismatch | Section 61 scrutiny notice | Reconcile before filing each return |

| Excess or unsupported ITC claim | ITC reversal demand + 18% interest | Verify against GSTR-2B before claiming |

| Late filing of GSTR-1 / GSTR-3B | Late fees + GSTIN suspension risk | Automate reminders; use a GST compliance calendar |

| Ignoring GST notices | Ex-parte demand order | Engage a GST practitioner within 48 hours of receipt |

| Not reconciling ITC monthly | Mismatches trigger automated notices | Monthly purchase register vs GSTR-2B reconciliation |

| Errors in e-invoicing / e-way bills | Penalties + ITC denial for buyers | Use GSTN-approved software with auto-validation |

GST Compliance Checklist India 2026: Complete Filing Schedule

| Return / Obligation | Frequency | Due Date |

| GSTR-1 (Outward Supplies) | Monthly / Quarterly (QRMP) | 11th of following month / Quarterly |

| GSTR-3B (Tax Payment Return) | Monthly | 20th / 22nd / 24th (category-based) |

| GSTR-9 (Annual Return) | Annual | 31st December of following FY |

| GSTR-9C (Reconciliation Statement) | Annual (turnover >Rs. 5 crore) | 31st December of following FY |

| E-way Bills | Per consignment | Before goods movement commences |

| E-invoicing | Per transaction (turnover >Rs. 5 crore) | Real-time reporting to IRP |

| LUT (Letter of Undertaking) | Annual (exporters) | Before first export invoice of the FY |

Frequently Asked Questions

Q1. What is the late fee for filing GSTR-3B after the due date?

Late fee is Rs. 50 per day (Rs. 25 CGST + Rs. 25 SGST), subject to a maximum of Rs. 10,000 per return. For Nil returns, the fee is Rs. 20 per day. Interest at 18% per annum is charged separately on any unpaid tax amount.

Q2. How do I resolve an ITC mismatch between my records and GSTR-2B?

Compare your purchase register against GSTR-2B. Contact suppliers who have not filed their GSTR1. Where suppliers remain non-compliant, reverse the provisional ITC under Section 16(2) and re-claim once the supplier files maintaining contemporaneous documentation of all follow-ups.

Q3. Is e-invoicing mandatory for all businesses?

As of 2024-25, e-invoicing is mandatory for all GST-registered businesses with aggregate turnover exceeding Rs. 5 crore in any financial year from FY 2017-18 onwards. This threshold has progressively reduced since 2020 and may be reduced further in future GST Council meetings.

Q4. Can a GST show cause notice be withdrawn after a satisfactory response?

Yes. If the adjudicating officer accepts the taxpayer’s response as satisfactory and complete, proceedings can be dropped without any demand or penalty being confirmed. This outcome is most reliably achieved with a professionally drafted, fully documented reply.

Q5. What is the QRMP scheme?

The Quarterly Return Monthly Payment (QRMP) scheme allows taxpayers with aggregate turnover up to Rs. 5 crore to file GSTR-1 and GSTR-3B quarterly, while making monthly tax deposits through a fixed-sum challan or self-assessed payment. Available since FY 2021-22.

Conclusion: Compliance Is the Foundation of Business Continuity

GST compliance in 2026 is not just about avoiding penalties it is about protecting your business’s operational continuity, commercial relationships, and credit standing. Businesses that build systematic, technology-supported compliance processes experience fewer notices, lower professional costs, and stronger buyer relationships.

About the AuthorAbout the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977has guided hundreds of SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly

contributes to professional seminars and industry forums in Pune.