How to Reply to a GST Notice Under Section 73 The Ultimate Taxpayer’s Survival Guide (2026)

Dr. Haresh Adwani, April 2026, 9 min read

Reply to a GST Notice

You open your email one morning to find a notice from the GST department. Your pulse quickens. Your mind races. What does this mean? Will you face massive penalties? Is your business at risk?

Take a deep breath you are not alone, and this situation is far more manageable than it seems.

Every year, thousands of Indian businesses receive a GST notice under Section 73 of the Central Goods and Services Tax (CGST) Act, 2017. Most of these notices arise from routine discrepancies in return filings not from any deliberate wrongdoing. The good news? When handled correctly and promptly, a Section 73 notice can be resolved without paying a single rupee in penalty.

This comprehensive 2026 guide crafted by the advisory team at ITR Advisor in consultation with Dr. Haresh Adwani of Adwani and Company walks you through every step of the process. From understanding what the notice actually says, to drafting a powerful reply, to attending hearings and filing appeals, we cover it all.

What is a GST Notice Under Section 73? Understanding the Legal Framework

Section 73 of the CGST Act, 2017 empowers a Proper Officer of the GST department to issue a Show Cause Notice (SCN) to a registered taxpayer when any of the following situations arise:

- Tax has not been paid or has been short-paid

- An erroneous refund has been claimed and granted

- Input Tax Credit (ITC) has been wrongly availed or utilised

The defining feature of a Section 73 notice and what separates it from the far more serious Section 74 is that it applies only to cases where there is NO allegation of fraud, wilful misstatement, or suppression of facts. In other words, the tax authority is saying: ‘We believe there is a gap in your tax payments, but we are not accusing you of intentional wrongdoing.’

According to the GST Portal (gst.gov.in), Section 73 proceedings are one of the most common types of demand proceedings initiated against registered taxpayers, particularly in the context of ITC mismatches and return filing inconsistencies.

Learn more about our GST Compliance and Advisory Services to ensure your filings are always accurate and audit-ready.

When is a GST Notice Under Section 73 Issued? Common Triggers You Must Know

Understanding why you received this notice is the first critical step toward resolving it. The GST department relies heavily on data analytics and cross-matching of return data to identify discrepancies. Here are the most common triggers:

| Trigger Scenario | Root Cause | Frequency |

| GSTR-3B vs GSTR-2A/2B Mismatch | ITC claimed exceeds supplier-reported figures | Very High |

| GSTR-1 vs GSTR-3B Discrepancy | Output tax declared but not fully remitted | High |

| Short Payment of Tax | Tax liability computed incorrectly | High |

| Excess ITC Claimed | ITC beyond eligible or blocked credit limits | Medium |

| Erroneous Refund Received | Refund conditions not fulfilled at the time of claim | Medium |

| Annual Return Mismatch | GSTR 9/9C data inconsistent with monthly returns | Medium |

| Non-payment by Unregistered Persons | Tax liability exists but not discharged | Low |

As Dr. Haresh Adwani frequently advises his clients: ‘A Section 73 notice is not the end of the road it is an invitation by the department to explain your position. Your response determines the outcome, not the notice itself.’

Critical Time Limits Under Section 73 : Deadlines That Can Make or Break Your Case

One of the most important and most overlooked aspects of handling a GST notice under Section 73 is understanding the time limits. Missing a deadline can transform a simple notice into a confirmed demand with penalties and interest.

| Action | Time Limit | Outcome |

| Voluntary payment before SCN | Any time before SCN is issued | No SCN issued — zero penalty |

| Payment after SCN within window | Within 30 days of receiving SCN | No penalty levied — only tax + interest |

| Filing your reply (DRC-06) | As mentioned in the notice (typically 30 days) | Failure = ex-parte order against you |

| Officer must issue demand order (DRC-07) | Within 3 years from due date of annual return | Notice becomes time-barred if officer misses this |

| SCN issuance deadline | At least 3 months before the order deadline | Can be challenged as legally defective |

| Appeal against order (GST APL-01) | Within 3 months from date of order | Right to appeal forfeited if missed |

Important 2026 Update: Following amendments introduced through the Finance Act 2024, the deadline for issuing orders under Section 73 for financial years 2018-19 through 2021-22 was extended. If you receive a notice covering these years in 2025 or 2026, it may still be legally valid. Always verify the notice date against the applicable deadline and consult a qualified tax advisor immediately.

Read our detailed guide on GST Return Filing Deadlines and Compliance Calendar to stay ahead of important dates.

https://itradvisor.in/blog/how-to-reply-to-a-gst-notice-under-section73

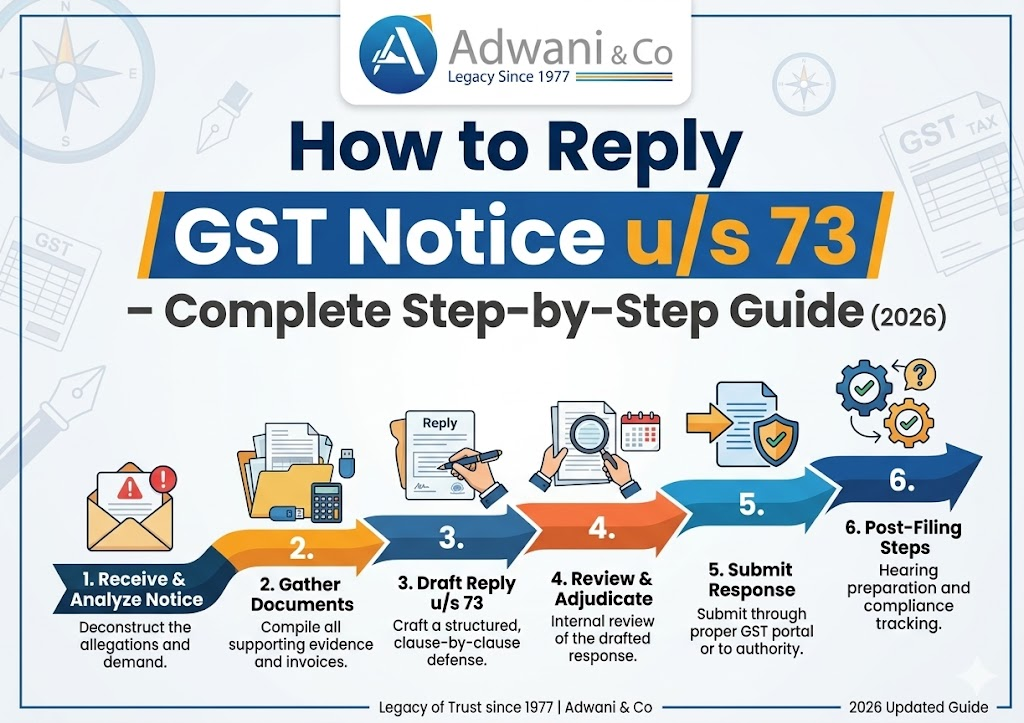

Step by Step: How to Reply to a GST Notice Under Section 73 (7 Step Action Plan)

Now let’s get to the heart of the matter — the actual process of replying to your GST Section 73 notice. Follow these seven steps methodically for the best possible outcome.

Step 1 : Read the Notice Carefully (DRC-01 or DRC-01A)

Before doing anything else, sit down and read the notice thoroughly. Identify the following key elements:

- Financial year and tax period in question

- Amount demanded broken down by CGST, SGST, IGST, and Cess

- Specific reason or allegation stated in the notice

- Whether this is a pre SCN intimation (DRC 01A) or a formal Show Cause Notice (DRC 01)

- The exact deadline for your response

DRC-01A is an intimation before the formal notice responding at this stage gives you the maximum benefit of zero penalty.

Step 2 : Gather and Analyse Your Records

Download all relevant data from the GST portal for the disputed period: your GSTR 1, GSTR 3B, GSTR 2A, and GSTR 2B. Compare the department’s claim against your own books. In most cases, discrepancies arise from timing differences, supplier non-filing, or genuine data entry errors all of which can be explained with proper documentation.

Step 3 : Decide Your Response Strategy

Based on your analysis, you have three broad options:

- Option A : Accept and Pay: If the demand is correct, paying within 30 days of the SCN eliminates any penalty. You pay only tax + 18% interest.

- Option B : Partial Agreement: Accept the valid portion of the demand, pay it, and formally contest the remaining amount with evidence.

- Option C : Full Contest: If you believe the entire demand is incorrect or unsupported, file a detailed point-by-point rebuttal with documentary proof.

Dr. Haresh Adwani recommends: ‘Always aim for Option A or B where the facts support it. Paying what is legitimately due and contesting only what is genuinely disputable gives you the strongest position with the adjudicating officer.’

Step 4 : Draft Your Reply (GST Notice Reply Format for Section 73)

Your written reply must address each allegation in the SCN paragraph by paragraph. The reply should include:

- A brief background of your business and the relevant period

- A point-by-point rebuttal of each discrepancy raised

- A reconciliation statement showing your computation vs. the department’s

- References to relevant GST circulars, notifications, or judicial rulings (if applicable)

- A list of attached supporting documents

File your reply using Form GST DRC-06 on the GST portal. You can upload your detailed written representation as a PDF attachment within the form.

Step 5 : File the Reply on the GST Portal

Log in to the GST Portal at gst.gov.in. Navigate to: Services → User Services → View Notices and Orders. Locate the relevant notice and click on it to open the reply interface. Select DRC-06, fill in the required details, upload your reply document and supporting attachments (PDF, maximum 5 MB each), and submit. Save the ARN (Acknowledgement Reference Number) as proof of submission.

Step 6 : Attend the Personal Hearing

After reviewing your reply, the adjudicating officer may call you for a personal hearing. This is your opportunity to present your case verbally and clarify any points of confusion. Attend in person or send an authorised representative (a CA or tax consultant). Carry original documents, a concise argument sheet, and be prepared to answer questions. If you need more time, request a written adjournment through the portal.

Step 7 : Review the Order and Plan Next Steps

Following the hearing, the officer will issue a demand order via Form DRC-07. If the order is in your favour, no further action is needed. If you disagree with the outcome, file an appeal before the First Appellate Authority using Form GST APL-01 within three months of the order date. Pre-deposit 10% of the disputed amount when filing the appeal.

Documents Required to Effectively Reply to a Section 73 GST Notice

A strong reply is only as powerful as the evidence behind it. Gather the following documents before filing your response:

- GSTR 1 for all months in the disputed period

- GSTR 3B for all months in the disputed period

- GSTR 2A and GSTR 2B reconciliation statement

- GSTR-9 (Annual Return) and GSTR-9C (if applicable)

- Purchase invoices supporting every ITC claim in question

- Sales invoices for the disputed tax period

- Bank account statements confirming payment of tax

- Supplier correspondence or confirmation letters (for disputed ITC)

- E-way bills (where goods movement is in question)

- Books of accounts and tax ledgers

- CA certified reconciliation statement this carries significant weight

Pro Tip from the ITR Advisor team: Even if the officer did not specifically ask for a reconciliation statement, always include one. It demonstrates transparency and good faith two qualities that adjudicating officers value when exercising their discretion.

Real World Example: How Proper Handling of a Section 73 Notice Saved ₹16+ Lakhs

To understand the real-world impact of responding correctly, consider this illustrative case:

A mid-sized textile wholesaler in Pune received a Section 73 SCN alleging that ITC of ₹18.4 lakhs had been claimed on invoices not reflecting in GSTR-2B for FY 2021-22. The business owner, unfamiliar with the process, missed the initial response deadline, and an ex-parte order was passed confirming the entire demand.

When the case was brought to Adwani and Company, Dr. Haresh Adwani’s team conducted a detailed reconciliation exercise. They discovered that:

- 87% of the disputed ITC (₹16.01 lakhs) was valid and supported by purchase invoices and payment proof. The mismatch had occurred because several suppliers had filed GSTR-1 after the GSTR-2B cut-off date.

- The remaining ₹2.39 lakhs represented ITC that had genuinely been claimed in error.

The team filed a rectification application with the complete reconciliation and supporting evidence. The result: the confirmed demand was reduced from ₹18.4 lakhs to just ₹2.1 lakhs — a reduction of over 88%. The penalty on the rectified amount was also fully waived given the circumstances.

The lesson? Even after an ex-parte order, a well-constructed response backed by solid documentation can dramatically change the outcome. Acting early is always better, but acting correctly is what truly matters.

What Happens If You Ignore a GST Section 73 Notice? The Consequences Are Severe

| Situation | Legal Consequence |

| No reply filed within stipulated time | Ex-parte order passed demand confirmed without hearing your side |

| Demand confirmed via DRC-07 | 18% annual interest on unpaid tax + minimum 10% penalty |

| Continued non payment after order | Recovery actions: bank account attachment, asset seizure |

| Failure to pay confirmed demand | Tax Recovery Officer issues certificate property recovery initiated |

| Minimum penalty under Section 73 | Higher of ₹10,000 or 10% of the tax demand confirmed |

The single most important thing to remember: if you pay the full tax demand within 30 days of receiving the SCN, you pay ZERO penalty. This window is your most valuable legal protection do not let it pass unused.

Conclusion: A Section 73 GST Notice Is a Problem You Can Solve With the Right Guidance

Receiving a GST notice under Section 73 is understandably stressful. But with the right knowledge and timely action, it is a problem that can be resolved often without paying any penalty at all.

The key steps are simple in principle: read the notice carefully, understand the allegation, gather your documentation, and respond within the stipulated time. Whether you choose to pay, partially accept, or fully contest the demand, what matters most is that you respond and respond well.

The Indian GST framework, as administered through the GST Portal (gst.gov.in) and guided by the Ministry of Finance, provides multiple safeguards for honest taxpayers. The law rewards proactive compliance and penalises inaction. Every window the law provides the 30-day penalty-free payment window, the right to a personal hearing, the right to appeal exists to protect you. Use these windows wisely.

1: What is the correct format for replying to a GST Section 73 notice? Is there a PDF format?

There is no fixed government-prescribed PDF format for the reply. Your response is filed online using Form GST DRC-06 on the GST portal (gst.gov.in). You prepare your detailed written reply addressing each point in the notice and upload it as a PDF attachment within DRC-06. The quality and completeness of your reply document matters far more than its format.

2: How is replying to a GST notice different from replying to an Income Tax notice?

They are entirely separate processes governed by different laws and portals. Income tax notices are handled under the Income Tax Act, 1961 via the Income Tax portal (incometax.gov.in), while GST notices are handled under the CGST Act, 2017 via the GST portal (gst.gov.in). The forms, time limits, appellate authorities, and procedural rules differ significantly. Expertise in one does not automatically translate to competence in the other.

3: What is the time limit to reply to a GST notice under Section 73?

The reply deadline is specified in the notice itself, and is typically 30 days from the date the notice is served. If you receive a DRC-01A (pre-notice intimation) before the formal SCN, you have 30 days to pay or respond before the SCN is formally issued. Extensions can be requested in writing through the portal, though they are at the officer’s discretion.

4: Can I completely avoid paying a penalty under Section 73?

Yes completely. If you pay the full tax liability within 30 days of the SCN being issued, Section 73(8) of the CGST Act explicitly provides that no penalty shall be payable. Even better, if you pay voluntarily upon receiving the DRC-01A (before the SCN is even issued), neither the SCN nor any penalty will apply. The law is deliberately designed to reward proactive compliance.

5: What if I believe the entire demand is wrong? Can I contest it fully?

Absolutely. File a detailed reply via DRC-06 on the GST portal, addressing every allegation with supporting evidence invoices, ledger entries, reconciliation statements, and any relevant legal provisions or circulars. The officer is legally obligated to consider your reply before issuing any order. If the order still goes against you, you retain the right to appeal before the GST Appellate Authority (GST APL-01) within three months. The tax dispute process in India has multiple levels of recourse.

FAQ 6: Is a Section 73 GST notice a criminal matter? Should I worry about prosecution?

No. Section 73 is a civil tax proceeding not a criminal one. Criminal prosecution under GST law is governed by Section 132 and applies only to cases involving deliberate fraud, fake invoicing, or wilful tax evasion above ₹2 crore. A Section 73 notice, by definition, involves no allegation of fraud. Responding properly ensures the matter remains in the civil domain and is resolved administratively.

7: Should I hire a CA or tax consultant to handle a Section 73 notice?

For any demand above ₹1 lakh, or where ITC mismatches are involved, professional representation is strongly recommended. A qualified Chartered Accountant can identify weaknesses in the department’s claim, compute the correct tax liability, draft a legally sound reply, represent you in personal hearings, and negotiate for reduction or waiver of demands. The cost of professional advice is almost always a fraction of what an improperly handled notice can cost you in penalties, interest, and recovery actions.

As Dr. Haresh Adwani of Adwani and Company puts it: ‘The worst response to a GST notice is no response. The best response is a prompt, well-documented, professionally crafted reply that demonstrates your commitment to compliance and places the burden of proof squarely on the department’s claims.’

At ITR Advisor, we are committed to making complex tax matters understandable and manageable for every Indian business from startups to established enterprises. Our goal is to give you the clarity and confidence to handle any tax situation with authority.

Take Action Today Expert GST Notice Assistance Is Just a Call Away

Facing a GST notice under Section 73 and unsure how to respond? Do not wait every day counts when tax deadlines are involved.

Connect with Adwani and Company a trusted CA firm with decades of experience in GST advisory, tax notice handling, and business compliance. Led by Dr. Haresh Adwani (PhD in Commerce, Law Graduate, Managing Partner), the firm has successfully resolved hundreds of GST disputes for SMEs, startups, and corporates across Pune and Maharashtra.

- 90%+ success rate in demand reduction

- Expert reply drafting and hearing representation

- 24-hour turnaround for urgent notice reviews

- Transparent, fixed-fee advisory

ContactAdwani and Company today for a confidential consultation and take the first step toward resolving your GST notice with confidence, clarity, and expert support.

Visit: www.adwaniandco.com | Call: +91 7620 127 137 | Email: enquiries@adwaniandco.com