Income Tax AY 2026-27: The Proven Guide to New ITR Forms, Rules & Avoiding Costly Mistakes

Why AY 2026-27 Could Be the Most Important Tax Year of Your Life

Income tax AY 2026-27 is here and it brings the most sweeping changes to India’s tax filing system in over six decades. If you file the wrong ITR form, miss a renamed document, or skip the new Aadhaar validation rule, your return will be flagged as defective. The penalties are real, the deadlines are firm, and the window to prepare is shrinking fast.

This is your proven, step-by-step guide to everything that has changed and exactly what you must do to file correctly, confidently, and on time.

What Has Changed in Income Tax AY 2026-27? (Key Highlights)

Before we go deep, here is a rapid summary of every major change under the new Income Tax Act, 2025 and Income Tax Rules, 2026, both effective from 1 April 2026:

- ✅ All ITR forms (ITR-1 to ITR-7) have been fully revamped

- ✅ ITR-1 now permits up to two house properties a landmark change for salaried taxpayers

- ✅ LTCG up to ₹1.25 lakh under Section 112A is now reportable directly in ITR-1

- ✅ Deductions under Sections 80C–80U must now be selected via a precise sub-section drop-down

- ✅ The 28-digit Aadhaar Enrolment ID is no longer accepted — only the 12-digit Aadhaar Number is valid

- ✅ Dual contact details (two emails + two mobile numbers) are now mandatory for every filer

- ✅ Form 16 has been renamed Form 130 and Form 26AS is now Form 168

- ✅ Both AY 2026-27 and TY 2026-27 now coexist on the e-filing portal choosing the wrong one is a critical and costly mistake

Each of these is explained in full below.

The Legal Foundation: Income Tax Act 2025 & Income Tax Rules 2026

The Income Tax Act, 1961 served Indian taxpayers for 65 years. From 1 April 2026, it has been replaced procedurally by the Income Tax Act, 2025, supported by the freshly issued Income Tax Rules, 2026.

What this means in practice:

- Tax slabs and rates remain broadly similar for most taxpayers

- But the reporting procedures, form structures, document names, and validation rules have been comprehensively redesigned

- All ITR forms have been rebuilt from scratch under the new legal framework

- Dozens of statutory documents that employers and professionals have used for years now carry entirely new names and form numbers

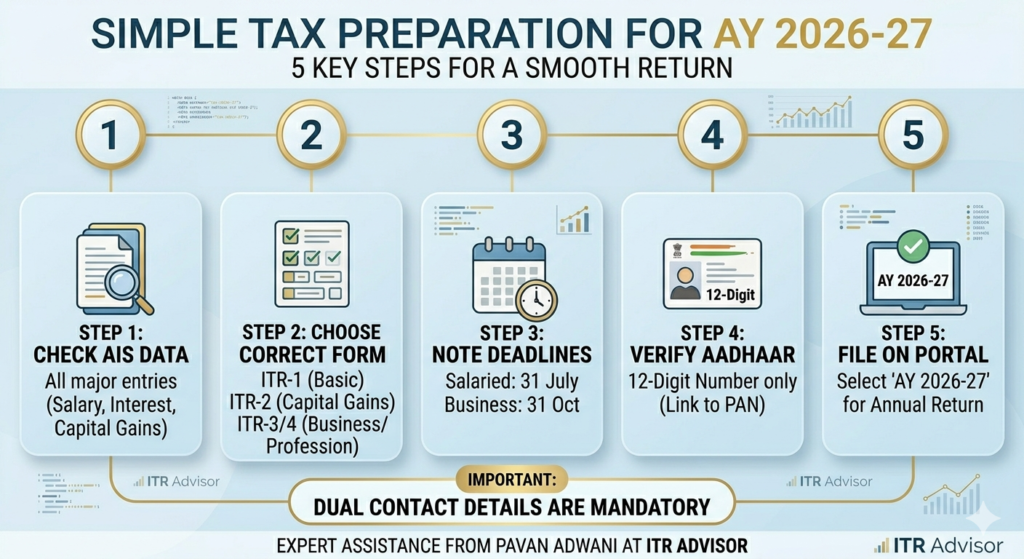

According to the Income Tax Department of India at incometax.gov.in, the restructuring aims to reduce ambiguity in declarations, improve accuracy of TDS credit reconciliation, and tighten alignment between taxpayer-reported income and the government’s own Annual Information Statement (AIS) data.

The message for every taxpayer is simple: last year’s approach will not work in income tax AY 2026-27. The rules have changed and those who adapt early will have a smooth season while those who don’t will face notices, defective return orders, and delays.

Learn more about our Taxation & Compliance Services at ITR Advisor we help individuals, businesses, and professionals navigate every update with confidence.

Critical ITR Filing Due Dates for AY 2026-27 Do Not Miss These

Missing a deadline costs money. Under Section 234F, late filing attracts a fee of up to ₹5,000. Beyond the fee, late filers may lose the right to carry forward capital losses and face delays in TDS refund processing.

Mark these dates in your calendar right now:

| Taxpayer Category | Applicable Forms | Last Date |

|---|---|---|

| Salaried, pensioners, non-audit individuals | ITR-1 & ITR-2 | 31 July 2026 |

| Non-audit businesses & professionals | ITR-3 & ITR-4 | 31 August 2026 |

| Tax audit cases (businesses & firms) | ITR-3, ITR-5 & ITR-6 | 31 October 2026 |

| Transfer pricing cases | As applicable | 30 November 2026 |

Each of these changes is explained in detail below.

Expert advice from Pavan Adwani: “Do not wait until July. The new forms demand far more granular data than before reconciled AIS, precise sub-section deduction mapping, and verified Aadhaar details. Taxpayers who start in June file better returns and get refunds faster.”

🔗 Read our detailed guide on ITR Filing Deadlines and Late Filing Penalties

Which ITR Form Should You File for AY 2026-27? Complete Guide

Filing the wrong ITR form results in a defective return notice from the department. Here is the definitive breakdown of all seven forms:

ITR-1 (SAHAJ) – Massively Expanded for AY 2026-27

Who can use it: Resident individuals earning salary or pension income, with up to two house properties (NEW), income from other sources, and LTCG under Section 112A of up to ₹1.25 lakh with no brought-forward losses (NEW).

This is the biggest practical change in the income tax AY 2026-27 filing season. Millions of salaried taxpayers who were previously forced to file the more complex ITR-2 solely because of two house properties or small capital gains can now use the simpler SAHAJ form.

ITR-2 – Capital Gains, Foreign Assets, Multiple Properties

Who must use it: Individuals and HUFs with LTCG exceeding ₹1.25 lakh, more than two house properties, foreign assets or foreign income, or those who are directors in a company or hold unlisted shares.

ITR-3 – Business or Profession Income

Who must use it: Individuals and HUFs with income from a business or profession – including F&O traders, intraday stock traders, and all proprietorship businesses not opting for presumptive taxation.

ITR-4 (SUGAM) – Presumptive Taxation Made Simple

Who can use it: Individuals, HUFs, and firms that opt for the presumptive income scheme under:

- Section 44AD – businesses with gross turnover up to ₹2 crore

- Section 44ADA – professionals (doctors, CAs, lawyers, engineers) with receipts up to ₹50 lakh

- Section 44AE – goods transport operators

If you are eligible, this form eliminates the need for detailed bookkeeping and dramatically simplifies your compliance burden.

ITR-5, ITR-6, ITR-7

- ITR-5: Firms, LLPs, AOPs, and BOIs

- ITR-6: All companies not claiming Section 11 exemptions

- ITR-7: Trusts, research institutions, political parties, and specified entities under Sections 139(4A)–139(4D)

🔗 Not sure which ITR form applies to you? Read our detailed ITR-1 vs ITR-2 vs ITR-3 vs ITR-4 comparison guide

5 Game-Changing Updates Inside the New ITR Forms for AY 2026-27

1. Two House Properties Now Allowed in ITR-1 A Game-Changer for the Middle Class

Previously, owning two houses automatically disqualified you from filing ITR-1. You had no option but to use ITR-2, with all its additional complexity. This year that wall has come down. Under the new Income Tax Rules, 2026, individuals with up to two residential properties whether self-occupied, rented, or deemed let-out can continue using ITR-1, provided the rest of their income qualifies.

This single change benefits tens of millions of taxpayers across India.

2. Small Investors Get LTCG Relief in ITR-1

If you redeemed equity mutual funds or sold listed shares during FY 2025-26 and earned Long-Term Capital Gains under Section 112A of ₹1.25 lakh or less, and you have no capital losses brought forward from earlier years, you no longer need to file ITR-2. You can report these gains directly in ITR-1.

This is enormous relief for retail SIP investors who had small gains but were burdened with ITR-2 filings simply because of them.

3. Mandatory Drop-Down for Every Deduction No More Lump-Sum Entry

This is the change most likely to trip people up. The new forms no longer allow you to enter a single combined figure under Section 80C. You must now select the exact sub-section for each investment from a mandatory drop-down menu:

- 80C(a) → EPF contributions

- 80C(b) → PPF deposits

- 80C(c) → Life insurance premiums

- 80C(d) → ELSS mutual fund investments

- 80C(e) → Tuition fees

- 80D → Health insurance premiums

- And so on across 80C to 80U

What to do now: Collect every investment proof and map each one to the correct sub-section before you open the e-filing portal. Getting this wrong even with the right total amount can result in a defective return.

4. Aadhaar Enrolment ID Is Dead Only 12-Digit Aadhaar Accepted

The 28-digit Aadhaar Enrolment ID that many taxpayers used in previous years is no longer accepted on the e-filing portal under any circumstances. Only your 12-digit Aadhaar Number is valid for income tax AY 2026-27 filing.

Additionally, your Aadhaar must be actively linked to your PAN. If it is not, your return will be declared invalid and your TDS refunds will be withheld. Check your PAN-Aadhaar linking status at incometax.gov.in today.

5. Two Contact Details Are Now Compulsory

The new ITR forms require every filer to provide two separate email addresses and two separate mobile numbers. The department uses these for OTP verification, refund intimation, and official notices. If either contact becomes inactive, the department may be unable to reach you and that creates compliance risk.

Update your contact details before filing to ensure both sets are active and accessible.

Renamed Forms Under Income Tax Rules 2026 The Complete List

This is the change that is catching even experienced professionals off-guard. Under the Income Tax Rules, 2026, the names and numbers of almost every major statutory form have changed. Referencing old form names in tax proceedings or correspondence can cause serious complications.

Here is the complete renaming reference table:

| Old Name | New Form Number | What It Is |

|---|---|---|

| Form 16 | Form 130 | Employer’s TDS certificate for salary income |

| Form 26AS | Form 168 | Tax Credit Statement (TDS, TCS, advance tax) |

| Form 15G / 15H | Form 121 | Self-declaration for non-deduction of TDS on interest |

| Form 3CA / 3CB / 3CD | Form 26 | Unified Tax Audit Report |

| Forms 26QB / 26QC / 26QD / 26QE | Form 141 | Property purchase & rent TDS challan/return |

For HR teams and employers: Update your payroll software templates, TDS certificate formats, and employee communication templates immediately. Issuing a document labelled “Form 16” instead of “Form 130” during the income tax AY 2026-27 season may create confusion during employee tax filing and in any departmental proceedings.

AY 2026-27 vs TY 2026-27 The Costly Portal Confusion You Must Avoid

The e-filing portal at incometax.gov.in now simultaneously supports two compliance frameworks, and this is creating genuine confusion:

AY 2026-27 (Assessment Year 2026-27) Select this to file your regular annual return reporting income earned in FY 2025-26 (1 April 2025 to 31 March 2026). This is what almost every individual taxpayer needs to select.

TY 2026-27 (Tax Year 2026-27) This is for ongoing compliance obligations under the new Income Tax Act, 2025, tracking transactions from 1 April 2026 onward. This is NOT your annual return for past income.

Selecting TY 2026-27 when you intend to file your regular annual return is a critical and costly mistake your submission will be misclassified and you may face a notice for non-filing of the actual return.

Always choose AY 2026-27 for your standard annual income tax return. When in doubt, consult a professional.

Real-World Example: Choosing the Right ITR Form for AY 2026-27

Here is a practical scenario from the advisory files of Pavan Adwani that illustrates how the new rules work:

Case Study: Priya Senior Analyst, Pune

Priya earns ₹13.8 lakh annually from her job. She owns two flats one self-occupied, one rented at ₹15,000/month. In December 2025, she redeemed equity mutual funds she had held for over two years, earning LTCG of ₹78,000 under Section 112A. She has no carried-forward capital losses.

| Income Component | Amount |

|---|---|

| Salary Income | ₹13,80,000 |

| Rental Income (after 30% standard deduction) | ₹1,26,000 |

| LTCG under Section 112A | ₹78,000 |

| Less: Section 80C (EPF + LIC) | ₹1,50,000 |

| Less: Standard Deduction | ₹75,000 |

Which form should Priya use?

Under the old rules, Priya would have been compelled to file ITR-2 due to two house properties and capital gains.

Under the income tax AY 2026-27 rules: Priya’s LTCG is below ₹1.25 lakh, she has no brought-forward losses, and the new rules permit two house properties in ITR-1. She now qualifies for the simpler ITR-1 (SAHAJ) saving time, reducing complexity, and lowering her risk of filing errors.

Proven 5-Step Action Plan for Filing Income Tax AY 2026-27 Without Stress

Step 1: Download Your AIS and Reconcile Every Entry

Log in to incometax.gov.in, navigate to the AIS section, and download your Annual Information Statement. Cross-check every transaction salary, dividends, mutual fund redemptions, interest income, property transactions against your own records. Raise objections on the portal for any incorrect entries before you file.

Step 2: Gather Capital Gain Statements from Every AMC and Broker

Get your Consolidated Account Statement (CAS) from CAMS or KFintech. Download individual capital gain statements from every mutual fund house where you redeemed units in FY 2025-26. Know your LTCG and STCG separately, by asset class and holding period.

Step 3: Map Every Deduction to the Correct Sub-Section

Create a simple table listing each investment/expenditure, the amount, the supporting document, and the exact sub-section it falls under. This preparation prevents errors in the new mandatory drop-down system.

Step 4: Verify PAN-Aadhaar Linkage Right Now

Do not wait until the day you file. Verifying and completing PAN-Aadhaar linkage takes a few days to reflect in the system. Check your status today at the official portal.

Step 5: Update Both Sets of Contact Details

Log into the e-filing portal and ensure your primary and secondary email and mobile number are both active. This is now a mandatory field in the new ITR forms a missing or inactive contact can block your return from being processed.

🔗 Want us to handle all of this for you? Book an ITR Filing Consultation with ITR Advisor

Conclusion: Income Tax AY 2026-27 Demands Preparation — Start Today

The income tax AY 2026-27 season is the most consequential filing season Indian taxpayers have faced in a generation. The transition to the Income Tax Act, 2025 and Income Tax Rules, 2026 has changed how you select your ITR form, how you claim deductions, what documents your employer must give you, and how the e-filing portal validates your identity.

The good news: every single one of these changes is manageable provided you start now, not in the last week of July.

Reconcile your AIS. Map your deductions. Verify your Aadhaar-PAN linkage. Know your correct ITR form. And if any part of this feels overwhelming, work with a qualified professional who already knows the new rules inside out.

As Pavan Adwani says: “The biggest tax mistakes are never made because someone didn’t know the rules. They are made because someone didn’t start early enough to apply them correctly. In AY 2026-27, that margin for error is smaller than ever.”

Frequently Asked Questions About Income Tax Filing AY 2026-27

Q1. What are the biggest income tax changes for AY 2026-27?

The major changes include: revamped ITR forms under the Income Tax Act, 2025 and Rules, 2026; expanded eligibility for ITR-1 (now allows two house properties and LTCG up to ₹1.25 lakh); mandatory sub-section-level reporting of deductions; rejection of Aadhaar Enrolment IDs; dual contact details requirement; and comprehensive renaming of statutory forms such as Form 16 (now Form 130) and Form 26AS (now Form 168).

Q2. What is the last date to file ITR for AY 2026-27 for salaried individuals?

For salaried individuals and non-audit cases filing ITR-1 or ITR-2, the due date is 31 July 2026. Filing after this date attracts a late filing fee under Section 234F and may result in loss of certain deductions.

Q3. Can I report capital gains in ITR-1 for AY 2026-27?

Yes, but with conditions. You can report LTCG under Section 112A up to ₹1.25 lakh in ITR-1, provided there are no brought-forward or carry-forward capital losses from previous years. If your LTCG exceeds ₹1.25 lakh or you have any capital losses, you must use ITR-2.

Q4. What is the difference between AY 2026-27 and TY 2026-27 on the e-filing portal?

AY 2026-27 is used for reporting income earned in FY 2025-26 this is your regular annual return. TY 2026-27 relates to current-year compliance under the new Income Tax Act, 2025 for transactions from April 2026. Most taxpayers filing their standard return should select AY 2026-27. Choosing TY 2026-27 by mistake will result in a misclassified filing.

Q5. What happens if my Aadhaar is not linked to my PAN when I file?

Your return will be treated as invalid by the department. You may also face withholding of TDS refunds and be unable to complete the OTP-based verification process. Link your Aadhaar to PAN at incometax.gov.in before attempting to file.

Ready to File Your Income Tax Return for AY 2026-27?

Don’t navigate the most complex tax season in years on your own.

Connect with ITR Advisor today powered by the expertise of Pavan Adwani and a team of seasoned tax and compliance professionals. Whether you are a salaried individual, a business owner, or a company navigating the new audit framework, we are here to make AY 2026-27 your smoothest filing year yet.

👉 Get Expert ITR Filing Assistance at ITR Advisor

Author

Pavan Adwani – Corporate Advisory, Tax Compliance & Regulatory Management.He is actively involved in advising business entities on corporate compliance, tax management, and regulatory frameworks, with a structured and process-oriented approach.