Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Dr. Haresh Adwani April 2026 11 min read

Introduction: Why Income Tax Notices Are Increasing in 2026

The Income Tax Department’s Annual Information Statement (AIS) now aggregates data from over 30 reporting entities banks, mutual funds, stock exchanges, property registrars, foreign remittance handlers, insurance companies, and employers against every PAN in India. In AY 2026-27, mismatches between ITR disclosures and AIS data are the primary automated notice trigger.

The result: the volume of income tax notices issued has risen significantly, and the majority of them are not accusations of wrongdoing they are requests for information, automated processing results, or procedural communications. The problem is never the notice itself; it is an uninformed, delayed, or incomplete response.

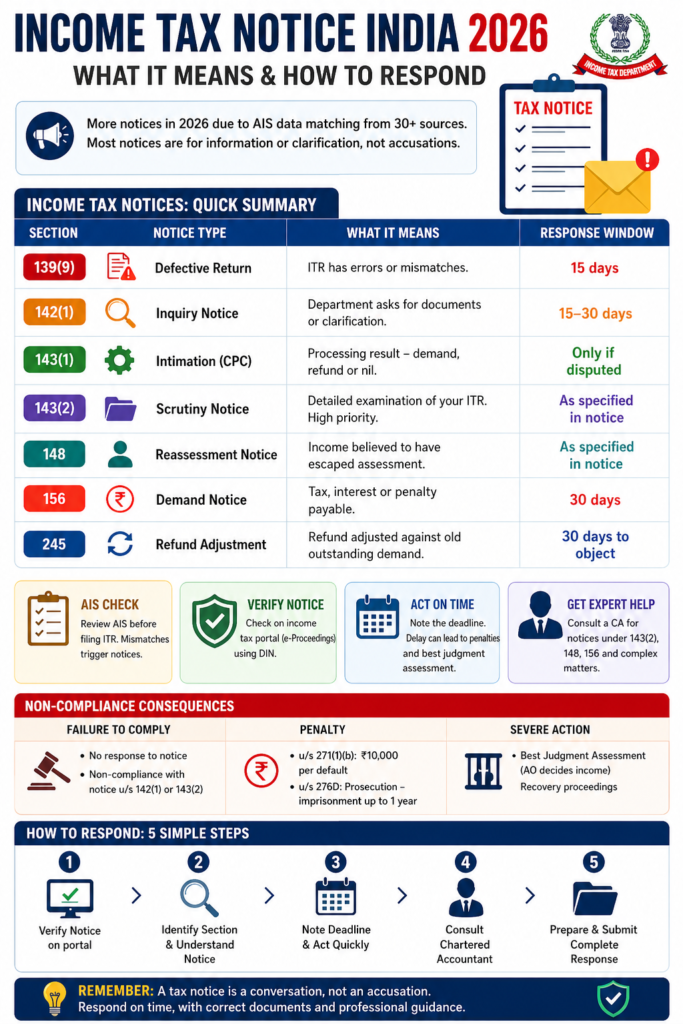

All Income Tax Notices: Quick Reference Table 2026

| Section | Notice Type | What It Means | Response Window |

| 139(9) | Defective Return | ITR has errors, wrong form, or data mismatches | 15 days |

| 142(1) | Inquiry Notice | Department seeks documents or clarifications | 15–30 days |

| 143(1) | Automated Intimation (CPC) | Processing result demand, refund, or nil | Only if disputed |

| 143(2) | Scrutiny Notice | Detailed examination of your ITR high priority | As specified in notice |

| 148 | Reassessment Notice | Income believed to have escaped assessment | As specified in notice |

| 156 | Demand Notice | Tax, interest, or penalty confirmed payable | 30 days |

| 245 | Refund Adjustment | Refund adjusted against old outstanding demand | 30 days to object |

Every Income Tax Notice Explained in Detail

Section 139(9): Defective Return Notice

Issued when your filed ITR is considered defective incorrect form selection, incomplete mandatory fields, or data mismatches between the ITR and Form 26AS or AIS. You must rectify and refile within 15 days. Failure results in the return being treated as never filed, attracting late filing penalties and permanent loss of loss carry-forward benefits.

Section 142(1): Inquiry Notice Before Assessment

One of the most frequently received notices. Issued to request production of specific documents, clarification on income items, or to ask you to file a return if you have not. Respond within the timeframe specified typically 15 to 30 days. This is usually manageable if your books are accurate and your ITR is correctly filed. Non-compliance attracts penalties under Section 271(1)(b) and, in wilful cases, criminal prosecution under Section 276D.

Section 143(1): Automated Intimation from CPC

This is an automated, system-generated intimation not a traditional assessment notice. It communicates the result of the CPC’s processing of your ITR: a demand, a refund, or no change. You need to respond only if you believe the department’s calculation is incorrect. In that case, file a rectification request under Section 154 on the e-filing portal. Most 143(1) demands arise from TDS credit mismatches or arithmetic differences.

Section 143(2): Scrutiny Notice High Priority

This is a high-priority notice. It signals that the Assessing Officer (AO) intends to examine your ITR in full detail requiring production of books of accounts, vouchers, contracts, and financial statements. The AO must issue this notice within 3 months from the end of the financial year in which the return was filed. Engage a qualified CA immediately. Do not attempt to respond to a Section 143(2) notice without professional representation.

Section 148: Reassessment Notice

Issued when the AO has “reason to believe” that income chargeable to tax has escaped assessment in a past year. The Finance Act 2021 fundamentally overhauled the reassessment framework a mandatory pre-notice procedure under Section 148A must now be followed before any Section 148 notice can be validly issued. A significant proportion of Section 148 notices are legally challengeable. The limitation period is 3 years from the end of the relevant assessment year for escaped income below Rs. 50 lakh; up to 10 years for escaped income of Rs. 50 lakh or more with specific documentary evidence.

Section 156: Notice of Demand

Issued after assessment is completed, confirming that tax, interest, or penalty is payable. You must pay within 30 days. If you disagree for example, because the demand does not account for TDS credits or because an appeal has been filed respond immediately with a rectification under Section 154 or an appeal under Section 246A. Failure to pay or contest results in recovery proceedings.

Section 245: Refund Adjusted Against Arrear Demand

Penalty Reference Table: Non-Compliance with Income Tax Notices

| Section | Violation | Consequence |

| 271(1)(b) | Failure to comply with notice under Section 142(1) or 143(2) | Rs. 10,000 penalty per default each failure is a separate default |

| 276D | Wilful failure to comply with Section 142(1) notice | Criminal prosecution imprisonment up to 1 year |

| 144 | No response to any notice AO proceeds ex-parte | Best Judgment Assessment AO determines income arbitrarily, typically adversely |

The AIS Cross-Matching Effect: Why More Notices Are Being Issued in 2026

The Annual Information Statement (AIS) captures data from banks (savings account credits, fixed deposits), mutual fund transactions, stock market trades (including F&O and ESOP vesting), property purchases and sales, foreign remittances, insurance policy payouts, and employer salary data. Every significant financial transaction is reported against your PAN.

Before filing your ITR for AY 2026-27, always download and review your AIS on www.incometax.gov.in. Unexplained entries in AIS should be addressed in the ITR itself not left to explain in a notice response. Discrepancies between AIS and ITR figures trigger automated notices within weeks of filing.

Also Read ;

https://itradvisor.in/blog/gst-show-cause-notice-2026

How to Respond to an Income Tax Notice: Step-by-Step

Step 1: Verify the Notice Is Genuine

Log into www.incometax.gov.in, go to the “e-Proceedings” tab, and verify the notice against your PAN. Every valid notice carries a Document Identification Number (DIN) use “Verify Service Request” to validate it. A notice without a DIN, or one not appearing in e-Proceedings, is legally invalid and need not be acted upon. Verify first, then respond.

Step 2: Identify the Section and Urgency Level

The notice specifies the section under which it is issued. This tells you the nature of proceedings and urgency. Section 143(2) and Section 148 require immediate professional engagement. Section 143(1) intimations are typically straightforward to resolve online using the rectification mechanism.

Step 3: Note Your Exact Response Deadline

Every notice carries a specific response deadline. Missing it risks: an ex-parte assessment done entirely on the AO’s judgment, adverse income additions, and Section 271(1)(b) penalties for each default. Your response deadline is your most critical resource time lost cannot be recovered.

Step 4: Engage a Chartered Accountant

Section 143(1) intimations can often be addressed directly via the e-filing portal. All other notices particularly 143(2), 148, and 156 require professional analysis, documentation assembly, and representation.

Frequently Asked Questions

Q1. Is every income tax notice cause for serious concern?

No. Many notices particularly Section 143(1) intimations and 139(9) defective return notices are routine and readily resolved. Identify the section first: that tells you precisely how serious the notice is and what action to take. Timely, informed action always produces the best outcome

Q2. What is the response timeline for a Section 143(2) scrutiny notice?

The notice specifies the exact response date typically 30 days from service. Extensions can be requested from the AO, but are not automatic and must be applied for before the deadline, not after.

Q3. Can a Section 148 reassessment notice be challenged?

Yes. If the notice was issued without the mandatory Section 148A procedure, beyond the limitation period, or without adequate “reason to believe,” it can be challenged by writ petition in the High Court. Adwani & Company has successfully quashed multiple invalid reassessment notices.

4. How do I verify that an income tax notice is genuine?

Log into www.incometax.gov.in → “e-Proceedings” tab → verify the notice appears against your PAN → use “Verify Service Request” to validate the DIN. If the notice does not appear in e-Proceedings, treat it as suspicious and consult a CA before taking any action.

Conclusion: An Income Tax Notice Is a Conversation Respond with Confidence

An income tax notice is the government’s mechanism for verifying your tax affairs not an automatic accusation of wrongdoing. The correct response is always timely, well documented, legally grounded, and professionally represented. Avoidance and delay are your two most damaging choices.

Adwani & Company’s income tax notice practice covers the complete dispute lifecycle: notice analysis, written submissions, AO representation, appeals before CIT(A), ITAT, and High Court writ petitions. Contact Dr. Haresh Adwani at www.itradvisor.in.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. As Managing Partner of Adwani & Co LLP a firm established in 1977 has guided hundreds of SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularlycontributes to professional seminars and industry forums in Pune.