ITR Filing 2026: Smart Strategies to Beat the Deadline, Slash Your Tax Bill & Secure Your Future

CA Dipesh Gurubakshani May 2026 14 min read

The Harsh Reality Most Indian Taxpayers Learn Too Late About ITR Filing 2026

Imagine discovering on August 1st that you missed the July 31st deadline. Your refund of ₹38,000 is delayed. The Income Tax portal is overloaded. And you’re now staring at a penalty notice.

This is not a hypothetical. It happens to lakhs of Indian taxpayers every single year.

The truth is that ITR filing 2026 is far more than a routine government formality. Done right, it is your most powerful financial instrument the document that unlocks loan approvals, validates visa applications, shields you from scrutiny, and legally puts thousands of rupees back in your pocket. Done wrong or worse, done late it becomes a costly, avoidable nightmare.

For Assessment Year 2026-27 (Financial Year 2025-26), the e-filing window is live on the Income Tax Department’s official portal at incometax.gov.in. Budget 2026 introduced sweeping changes to deadlines, revised return windows, and filing categories that every taxpayer — salaried, self-employed, NRI, or business owner must understand before hitting the submit button.

This guide, curated by the experts at Adwani and Company, breaks down every aspect of ITR filing 2026 in plain language: the exact deadlines, the correct forms, the smartest deductions, the costliest mistakes, and how to ensure your return not only complies with the law but actively works in your financial favour.

Learn more about our Income Tax Filing and Compliance Services

ITR Filing 2026 Last Date: Your CategoryWise Deadline Breakdown

One of the most consequential changes of Budget 2026 is the bifurcation of the ITR filing last date 2026 across taxpayer categories. This is no longer a single “July 31” deadline applicable to all. The Income Tax Department of India has assigned distinct deadlines based on your income type, the ITR form applicable to you, and whether a statutory tax audit is required.

Here is the authoritative breakdown for AY 2026-27:

| Taxpayer Category | Applicable ITR Form | ITR Filing Last Date 2026 |

| Salaried employees, pensioners, single house property owners | ITR-1 / ITR-2 | 31 July 2026 |

| Freelancers, consultants, small business owners (non-audit) | ITR-3 / ITR-4 | 31 August 2026 |

| Businesses and professionals requiring statutory tax audit under Section 44AB | ITR-3 / ITR-4 | 31 October 2026 |

| Belated return (missed original deadline) | All applicable forms | 31 December 2026 |

| Updated Return under Section 139(8A) | ITR-U | 31 March 2031 |

Critical Portal Alert: When accessing the Income Tax e-filing portal for AY 2026-27, always select

Tab 1 (Income Tax Act, 1961).

Tab 2 is reserved for Tax Year 2026-27 filings, which relate to the next assessment cycle. Selecting the wrong tab will invalidate your return entirely a mistake that can result in missed refunds and unnecessary processing delays.

At Adwani and Company, we routinely advises his clients: “Your ITR filing last date 2026 depends entirely on who you are as a taxpayer. The single biggest mistake people make is assuming their deadline is July 31st when it may legally be August 31st or even October 31st. Filing under a wrong assumption leads to either rushed errors or missed opportunities.”

What Budget 2026 Changed for ITR Filing: 3 Reforms Every Filer Must Know

Budget 2026 introduced taxpayer-friendly reforms that fundamentally alter the ITR filing landscape for AY 2026-27. Here are the three most impactful changes:

1. Extended Deadline for Freelancers and Business Taxpayers

For the very first time, non-audit filers using ITR-3 and ITR-4 covering freelancers, independent consultants, gig workers, and small business owners have been granted a one-month extension. The ITR filing last date 2026 for this category is now 31 August 2026, not July 31st.

This reform acknowledges the greater complexity involved in business tax filing, where income from multiple sources, GST reconciliation, and expense tracking all require additional time to compile accurately.

2. Revised ITR Window Extended to 31 March 2027

Previously, taxpayers who wanted to correct errors in a filed return or claim missed deductions had until December 31st of the relevant assessment year. Budget 2026 has extended this window significantly: Revised ITR filing for AY 2026-27 is now open until 31 March 2027.

This is one of the most taxpayer-friendly extensions in recent memory. If you file your return in July and later realize you missed a Section 80D deduction or reported a capital gain incorrectly, you now have until March 2027 to file a corrected return typically by paying a modest revision fee.

3. Updated Return (ITR-U) Window Extended to 4 Years

Under Section 139(8A) of the Income Tax Act, 1961, the Updated Return (ITR-U) mechanism has been extended to 48 months (4 years) from the close of the relevant assessment year. For AY 2026-27, eligible taxpayers can file an ITR-U as late as 31 March 2031.

The ITR-U is particularly valuable for taxpayers who later discover unreported income from freelance assignments, stock market gains, fixed deposit interest, or foreign assets. Using the ITR-U proactively is always preferable to facing a scrutiny notice from the Income Tax Department.

How to File ITR Online for AY 2026-27: A Step-by-Step Expert Walkthrough

ITR filing 2026 online is more streamlined than ever, but the most expensive mistakes are still made by taxpayers who rush through the process. The team at Adwani and Company, led by Dr. Haresh Adwani, recommends the following structured approach:

Step 1: Download and Verify Your Form 26AS and AIS

Log in to incometax.gov.in and download both your Annual Information Statement (AIS) and your Form 26AS for FY 2025-26. Cross-check every TDS entry, bank interest credit, dividend income, and transaction reported by third parties (banks, brokers, mutual fund houses) against your own records.

Any discrepancy between your declared income and the government’s data is an automatic scrutiny trigger. Resolve all mismatches with your employer, bank, or broker before filing.

Step 2: Select the Correct ITR Form

This is where a surprising number of taxpayers go wrong. The wrong ITR form results in a “defective return” notice and mandatory refiling.

- ITR-1 (Sahaj): Salaried individuals, pensioners, one house property, income below ₹50 lakh

- ITR-2: Individuals with capital gains income, more than one house property, or foreign assets

- ITR-3: Business or professional income with books of accounts

- ITR-4 (Sugam): Presumptive taxation under Sections 44AD, 44ADA, or 44AE

Step 3: Compute Your Total Income and Maximize Deductions

List every income source salary, rental income, interest, dividends, capital gains, freelance income and then systematically apply every deduction you are legally entitled to claim:

- Section 80C: Up to ₹1.5 lakh (PPF, ELSS, life insurance premium, home loan principal)

- Section 80D: Health insurance premium (₹25,000 for self; ₹50,000 for senior citizen parents)

- HRA Exemption: Computed as the minimum of three prescribed values — not simply the full HRA received

- Section 24(b): Home loan interest up to ₹2 lakh for self-occupied property

- Section 80TTA: Savings account interest exemption up to ₹10,000

- Section 80EEA: Additional home loan interest benefit for first-time buyers

Most taxpayers filing independently leave ₹20,000 to ₹60,000 of legally valid deductions on the table simply because they are unaware of the full breadth of what they are entitled to claim.

Step 4: E-File and E-Verify Within 30 Days

Submit your ITR through the Income Tax portal and e-verify within 30 days using Aadhaar OTP, net banking, or a pre-validated bank account. A return that is filed but not e-verified is treated as invalid effectively as if you never filed at all.

Step 5: Track Your Refund Status

After successful e-verification, monitor your refund at incometax.gov.in under “My Account → Refund/Demand Status.” Early filers consistently receive refunds weeks before late filers, simply due to lower portal congestion.

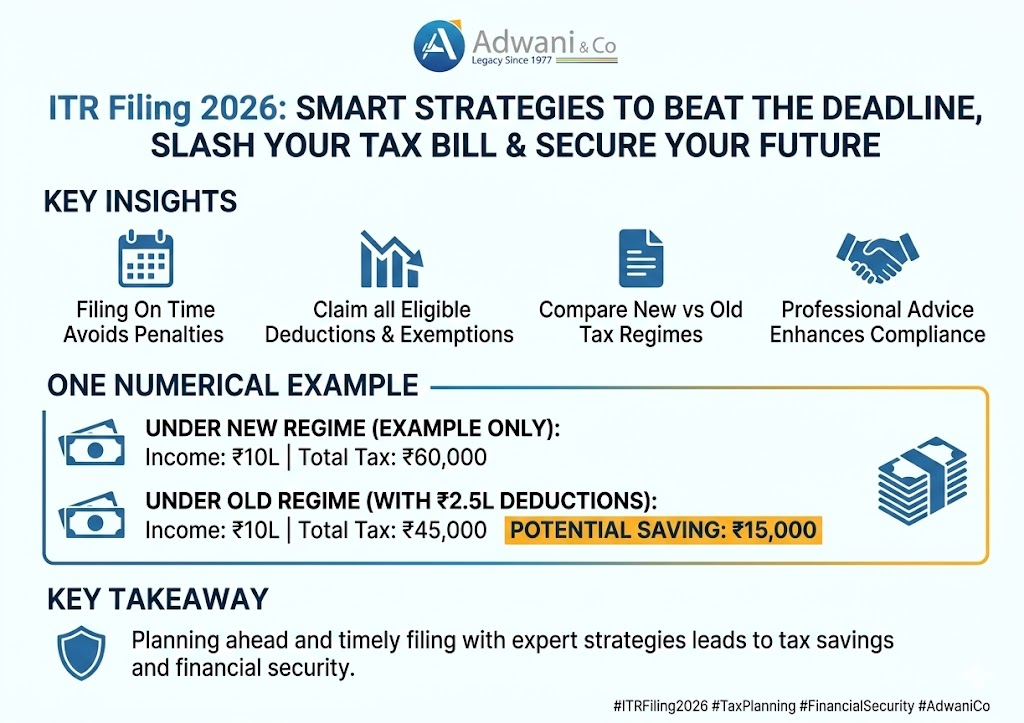

Real-World Example: How Expert ITR Filing 2026 Saved ₹42,000

Consider the case of Suresh Mehta, a 36-year-old IT professional in Pune earning ₹13.5 lakh annually. For three consecutive years, Suresh filed his own return in the last week of July, claiming only Section 80C deductions and his standard employer-reported HRA.

When he finally approached Adwani and Company for assisted ITR filing 2026, Dr. Haresh Adwani’s team conducted a thorough deduction review. Here is what they discovered:

| Deduction Head | Correctly Claimed Amount |

| Section 80C (PPF + ELSS mutual fund) | ₹1,50,000 |

| Section 80D (family health insurance) | ₹25,000 |

| HRA Exemption (recalculated correctly) | ₹84,000 |

| Home Loan Interest — Section 24(b) | ₹2,00,000 |

| Total Eligible Deductions | ₹4,59,000 |

Suresh had been computing his HRA exemption using only the amount received from his employer ignoring the prescribed three-value minimum formula. He had also never claimed his home loan interest, assuming it was already “handled” by his employer’s TDS computation (it was not).

The result: his taxable income dropped from ₹13.5 lakh to approximately ₹9 lakh. At applicable slab rates under the old regime, this translated to a verified tax saving of ₹42,000 tax he had been paying unnecessarily for three years.

This is the measurable difference that expert-assisted ITR filing 2026 delivers.

Learn more about our Deduction Maximization and Tax Planning Advisory

The Real Cost of Missing the ITR Filing 2026 Deadline

The Income Tax Act prescribes specific and escalating consequences for taxpayers who miss the ITR filing last date 2026. Under Section 234F, the late filing fee structure is:

- ₹1,000 if total income is below ₹5 lakh

- ₹5,000 if total income exceeds ₹5 lakh

Beyond the direct financial penalty, late filers also face:

- Interest under Section 234A at 1% per month on any outstanding tax payable

- Loss of carry-forward entitlement for capital gains losses, business losses, and speculative losses a particularly painful consequence for active stock market investors and F&O traders

- Heightened scrutiny probability from the Income Tax Department, including Section 143(2) notices and scrutiny assessments

- Loan and visa complications lenders and embassies typically require the most recent 2-3 years of filed returns as proof of income

The belated ITR deadline for AY 2026-27 is 31 December 2026. Beyond that date, the only option is the Updated Return (ITR-U) mechanism which carries a mandatory additional tax surcharge and cannot be used to claim deductions not already present in the original return.

As the Income Tax Department of India consistently emphasizes through its public outreach, voluntary, timely compliance is both a legal obligation and the most economically rational path for every taxpayer.

ITR Filing 2026 for Salaried vs Business Taxpayers: Key Differences

Salaried Taxpayers (ITR-1 / ITR-2) Deadline: 31 July 2026

Salaried individuals form the largest single category of Indian income tax filers. Their primary income documentation is Form 16 issued by employers, reflecting TDS deducted under Section 192. Key focus areas for ITR filing 2026 include:

- Accurate HRA exemption computation

- Full reconciliation of AIS data with actual income

- Claiming all eligible deductions under Sections 80C through 80U

- Correctly reporting capital gains from mutual fund redemptions or stock sales

Business and Professional Taxpayers (ITR-3 / ITR-4) Deadline: 31 August or 31 October 2026

Freelancers, consultants, traders, and business owners face greater filing complexity. Beyond income computation, they must:

- Maintain and reconcile books of account for the full financial year

- Cross-match GST returns (GSTR-1, GSTR-3B) with income tax filing to avoid discrepancies

- Determine whether tax audit under Section 44AB applies based on turnover thresholds

- Decide between presumptive taxation (Section 44ADA/44AD) and regular computation

Adwani and Company is exceptionally well-positioned to guide business taxpayers through this intersection of tax law, GST compliance, and financial structuring.

Critical ITR Filing Mistakes That Attract Income Tax Notices

Based on years of practice and thousands of client filings, the team at Adwani and Company has identified the most common, costliest errors made during ITR filing 2026:

1. Using the Wrong ITR Form: If you have capital gains even from a single mutual fund redemption ITR-1 is the wrong form. You need ITR-2. Incorrect form selection generates a defective return notice automatically.

2. Ignoring AIS Discrepancies: The Annual Information Statement aggregates data from banks, brokers, employers, and other institutions. Failing to reconcile your declared income with the AIS is the single most common trigger for scrutiny notices.

3. Omitting Bank Interest Income: Savings account interest, FD interest, and RD interest are all taxable in full. Even if TDS has been deducted, the gross interest must be reported in your ITR.

4. Incorrect HRA Calculation: HRA exemption is the minimum of three specific values not simply the HRA component on your payslip. Incorrectly computing this costs thousands of rupees to many salaried filers.

5. Filing Without E-Verifying: A submitted but unverified ITR is legally treated as a non-filing. Always e-verify within 30 days of submission.

6. Overlooking Foreign Assets: Under Schedule FA in the ITR, any foreign bank accounts, investments, or insurance policies must be disclosed. Failure to disclose attracts penalties under the Black Money Act up to ₹10 lakh per undisclosed asset. The Ministry of Finance and CBDT have intensified FATCA and CRS-based scrutiny significantly in 2026.

Read our detailed guide on how to respond on Income Tax notice https://www.adwaniandco.com/blog/income-tax-notice-received

Why Adwani and Company Is the Most Trusted Name for ITR Filing 2026

At Adwani and Company, ITR filing 2026 is handled not by automated software tools or generic templates — but by a team of qualified professionals under the personal supervision of Dr. Haresh Adwani, a PhD holder in Commerce and a trained legal professional with deep expertise in Indian tax statutes, FEMA regulations, and GST compliance.

What makes Adwani and Company the right partner for ITR filing 2026:

- Complete AIS and Form 26AS reconciliation prior to every filing eliminating the risk of income mismatch notices

- Deduction maximization review a systematic analysis of every eligible deduction the client is legally entitled to claim, across all applicable sections

- GST-ITR cross-verification ensuring your income tax return is fully consistent with your GST filing history, a critical requirement for all business taxpayers

- Legal interpretation of gray areas Dr. Haresh Adwani’s law background enables the firm to advise on legally nuanced questions involving capital gains classification, HUF planning, NRI taxation, and business income restructuring

- Year-round support extending beyond ITR filing season to cover assessments, scrutiny notices, revised returns, and proactive tax planning

Clients across Pune and across India salaried professionals, business owners, NRIs, and high-net-worth individuals consistently choose Adwani and Company for one reason: they know their return is being handled by professionals who combine technical accuracy with genuine accountability.

Conclusion:

The ITR filing 2026 season for AY 2026-27 is open. The deadlines July 31st for salaried taxpayers, August 31st for freelancers and small businesses are firm. The penalties for delay are real. And the financial benefits of accurate, timely filing faster refunds, deduction savings, and a clean compliance record are equally real and equally substantial.

Every rupee of deduction you miss is money you legally owe to yourself but chose not to claim. Every day you delay is a day the Income Tax portal gets busier, your refund gets slower, and your risk of an error-under-pressure grows.

The Income Tax Department of India has made the e-filing infrastructure at incometax.gov.in more accessible than ever. But navigating the system correctly, reconciling AIS data, choosing the right form, computing deductions accurately, and understanding Budget 2026 changes that is where expert guidance makes the difference between a return that merely complies and one that genuinely serves your financial interests.

“Filing your taxes on time and correctly is not a burden it is the single most powerful financial habit an Indian citizen can build. Your ITR is your financial identity. Make it count.”

Frequently Asked Questions

Q1. What is the ITR filing last date 2026 for salaried employees?

The ITR filing last date 2026 for salaried individuals and pensioners filing ITR-1 or ITR-2 is 31 July 2026, as confirmed by the Central Board of Direct Taxes (CBDT) and the Income Tax Department of India.

Q2. What is the ITR filing 2026 deadline for freelancers and consultants?

Budget 2026 extended the ITR filing last date 2026 for non-audit freelancers, consultants, and small business owners to 31 August 2026. This is a new, category-specific deadline introduced for FY 2025-26 AY 2026-27 filers.

Q3. What is the penalty for missing the ITR filing 2026 deadline?

Under Section 234F, a late filing fee of ₹1,000 (income below ₹5 lakh) or ₹5,000 (income above ₹5 lakh) applies. Additionally, Section 234A interest at 1% per month accrues on any outstanding tax. You also lose the right to carry forward certain losses.

Q4. Can I file a revised return after submitting my ITR?

Yes. Budget 2026 extended the revised ITR window to 31 March 2027 for AY 2026-27. You can correct errors, add missed deductions, or update income figures by filing a revised return before this date.

Q5. What documents are needed for ITR filing 2026?

? Key documents include: Form 16 (from employer), Form 26AS, Annual Information Statement (AIS), bank statements for the full year, investment proof for Section 80C, health insurance premium receipts, home loan interest certificate, and capital gains statements from your broker or mutual fund platform.

Q6. Can Adwani and Company help with ITR filing 2026 for NRIs?

Yes. Adwani and Company provides comprehensive ITR filing assistance for NRI taxpayers, covering capital gains on Indian property sales, rental income from Indian properties, NRE/NRO account treatment, RNOR status tax planning, and DTAA (Double Taxation Avoidance Agreement) benefit claims. Connect with Dr. Haresh Adwani’s team for a dedicated NRI tax consultation

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.