Old vs New Tax Regime 2025: Stop Guessing, Start Calculating

CA Dipesh Gurubakshani April 2026 11 min read

Every April, millions of Indian taxpayers face a question that could determine whether they save ₹50,000 or silently lose it: Should I choose the old vs new tax regime? Most people answer it the wrong way by asking colleagues, following guesswork, or simply doing nothing and letting the default kick in. That ‘nothing’ decision alone costs thousands of taxpayers lakhs of rupees every year.

The truth is, there is no universally correct answer. Whether the old vs new tax regime works better for you depends entirely on your income level, your deductions, your lifestyle, and your financial discipline. What this guide does is cut through the confusion and give you a clear, number-backed, expert-driven framework to make the right call for your life, not someone else’s.

With the Income Tax Act, 2025 now fully in effect and the new regime established as the default option, the stakes have never been higher. Let’s break it down completely.

Understanding the Old vs New Tax Regime : What Actually Changed

India’s personal income tax system today operates with two distinct parallel structures, each with its own slab rates, deduction rules, and strategic advantages. Every individual taxpayer whether salaried, self-employed, or running a business must choose one at the time of filing returns.

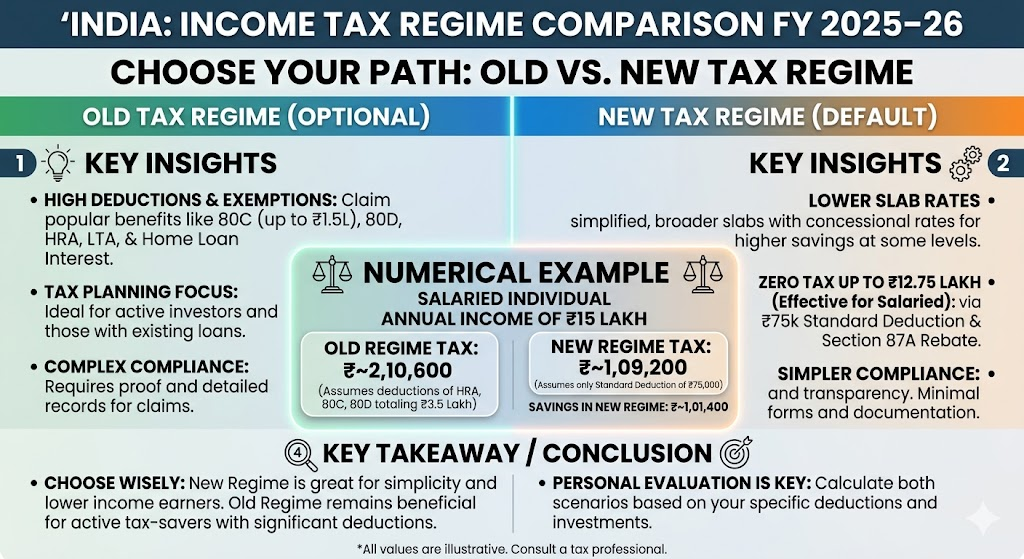

What is the Old Tax Regime?

The old tax regime has been the backbone of Indian income taxation for decades. It allows taxpayers to legally reduce their taxable income by claiming a wide range of deductions and exemptions. The Income Tax Department of India permits deductions such as:

- House Rent Allowance (HRA) under Section 10(13A)

- Standard Deduction of ₹50,000 for salaried individuals

- Section 80C deductions up to ₹1.5 lakh (PPF, ELSS, EPF, LIC, home loan principal)

- Section 80D for health insurance premiums (up to ₹25,000–₹50,000 depending on age)

- Home loan interest deduction under Section 24(b) up to ₹2 lakh for self-occupied property

- Leave Travel Allowance (LTA) and other specific exemptions

The key benefit: these deductions shrink your taxable income before slab rates are applied, meaning your effective tax rate can be significantly lower than what the published rates suggest.

What is the New Tax Regime?

Introduced in Budget 2020 and significantly restructured in Budget 2023, the new tax regime offers lower headline slab rates in exchange for giving up most deductions. Under the Income Tax Act, 2025, the new regime is now the default meaning taxpayers who do not actively opt out will be assessed under this regime.

The new regime is designed to simplify tax compliance, reduce paperwork, and appeal to those who prefer lower rates over complex deduction planning. It still allows the standard deduction of ₹75,000 (revised upward in 2024) and the employer’s NPS contribution under Section 80CCD(2) two benefits that are frequently overlooked.

Old Tax vs New Tax Regime : Slab Rate Comparison for FY 2025–26

| Income Slab | Old Regime Rate | New Regime (FY 2025–26) |

| Up to ₹3,00,000 | Nil | Nil |

| ₹3,00,001 – ₹7,00,000 | 5% | 5% |

| ₹7,00,001 – ₹10,00,000 | 20% | 10% |

| ₹10,00,001 – ₹12,00,000 | 30% | 15% |

| ₹12,00,001 – ₹15,00,000 | 30% | 20% |

| Above ₹15,00,000 | 30% | 30% |

On paper, the new regime’s lower rates between ₹7 lakh and ₹15 lakh look very attractive. But slab rates only tell half the story. Your effective tax rate the percentage of income you actually pay after deductions can be dramatically different. This is the calculation that Dr. Haresh Adwani, of Adwani and Company, insists every taxpayer must do before making their regime choice.

Key Deductions You Lose in the New Tax Regime : And Why It Matters for Tax Saving

Understanding the deduction gap is central to the old vs new tax regime comparison. Here are the most impactful deductions that are not available in the new regime:

HRA (House Rent Allowance): For salaried employees in metro and Tier-1 cities, HRA exemption often ranges from ₹1 lakh to ₹3 lakh annually. This is one of the most powerful salary components from a tax perspective and it simply does not exist in the new regime.

Section 80C (₹1.5 lakh limit): Covers PPF, ELSS mutual funds, home loan principal repayment, life insurance premiums, NSC, and children’s tuition fees. For any disciplined investor, this deduction is almost automatic and it saves up to ₹46,800 in taxes at the highest slab.

Section 80D (Health Insurance): Premiums paid for self and family can be deducted up to ₹25,000 (or ₹50,000 for senior citizens). In the new regime, this benefit disappears entirely.

Home Loan Interest Section 24(b): Up to ₹2 lakh annually on interest for a self-occupied property. For taxpayers with an ongoing home loan, this single deduction can be decisive in regime selection.

LTA (Leave Travel Allowance): Tax-exempt travel allowance available in the old regime for domestic travel twice in a four-year block. Not available in the new regime.

Learn more about our Taxation & Compliance Services — our CA team at Adwani and Company https://www.adwaniandco.com/blog/income-tax-filing-for-salaried-individuals

Real-World Numerical Example: Old vs New Tax Regime at ₹16 Lakh Income

Let’s apply real numbers to understand the difference between Old vs New Tax Regime . Consider Priya, a salaried software professional in Pune earning ₹16 lakh gross annually, with HRA, active 80C investments, a health insurance policy, and a home loan.

| Item | Old Regime | New Regime |

| Gross Salary Income | ₹16,00,000 | ₹16,00,000 |

| Standard Deduction | −₹50,000 | −₹75,000 |

| HRA Exemption | −₹1,80,000 | Not Applicable |

| Section 80C (PPF + ELSS) | −₹1,50,000 | Not Applicable |

| Section 80D (Health Ins.) | −₹25,000 | Not Applicable |

| Home Loan Interest (24b) | −₹1,20,000 | Not Applicable |

| Net Taxable Income | ₹10,75,000 | ₹15,25,000 |

| Approx. Tax (incl. cess) | ~₹1,45,000 | ~₹2,05,000 |

CASESTUDY

In this case, Priya saves approximately ₹60,000 more by choosing the old regime. This calculation assumes actual deduction claims and is illustrative individual results will vary based on specific figures.

This is the calculation that most taxpayers never run. As Dr. Haresh Adwani, founder of Adwani and Company, consistently guides clients: the regime that appears more generous at the slab level is frequently more expensive once your actual deductions are factored in.

Also Read https://itradvisor.in/blog/income-tax-notice

Which Income Band Benefits More : A Practical Old vs New Tax Regime Breakdown

Income Up to ₹12.75 Lakh

Under the new tax regime for FY 2025–26, taxpayers with income up to ₹12 lakh may have zero tax liability due to the revised Section 87A rebate (up to ₹60,000). Combined with the ₹75,000 standard deduction for salaried individuals, effective tax-free income rises to ₹12.75 lakh. For this income band especially those with minimal investments the new regime is a clear winner. This is one of the most significant improvements the government has introduced, as clearly outlined in the Finance Bill 2025 notified by the Ministry of Finance.

Income Between ₹12.75 Lakh and ₹18 Lakh

This is the battleground zone. If you have HRA, 80C investments, and a home loan, the old regime almost certainly wins. If your deductions are limited to just the standard deduction, the new regime may be comparable or marginally better. Running the actual calculation is non-negotiable at this income level.

Income Above ₹18–20 Lakh

For higher income brackets, the new regime’s lower slab rates begin to overpower the benefit of deductions but only if your total deductions are below a certain threshold. The break-even point varies depending on your HRA amount and home loan outstanding. Adwani and Company, has observed that even at ₹20 lakh+ income, taxpayers with substantial home loans and maximum 80C investments often fare better in the old regime.

Critical Mistakes to Avoid When Choosing Your Tax Regime

Mistake 1: Not Informing Your Employer Before April 1

The new tax regime is the default. If you want the old regime, you must proactively inform your employer before the start of the financial year. Failure to do so means TDS will be deducted under the new regime throughout the year potentially resulting in either a year-end tax demand or the hassle of claiming a refund.

Mistake 2: Deciding Based on Slab Rates Alone

Comparing tax regimes using published slab tables without running your actual income and deductions is like comparing cars by looking only at the price tag. Always calculate your net taxable income under both regimes before deciding.

Our tax advisory team offers this comparison service as part of every annual tax planning engagement.

Mistake 3: Ignoring the NPS Employer Contribution in the New Regime

Section 80CCD(2) allows a deduction for your employer’s NPS contribution up to 14% of your basic salary even in the new regime (versus 10% for private sector in the old regime). Many employees overlook this during CTC negotiation. Restructuring your salary to maximize this benefit is one of the smartest tax moves available under the new regime, and one that Adwani and Company actively helps clients implement.

Mistake 4: Forgetting the Business Income Switching Rule

Taxpayers with business or professional income who file under ITR3 or ITR4 face a critical restriction: they can switch from the new regime back to the old regime only once in their lifetime. After reverting to the new regime, they cannot switch back to old. This rule under Section 115BAC is frequently misunderstood and can result in irreversible tax decisions. Salaried individuals have no such restriction they can switch every year freely.

Mistake 5: Assuming the Same Answer as Last Year Still Applies

Your income changes. Your deductions change. Interest rates change. The regime that was optimal in FY 2024–25 may not be optimal in FY 2025–26. Annual reassessment ideally before April is essential. The Income Tax Department’s official calculator at incometax.gov.in is updated for each assessment year and provides a reliable starting point.

Old vs New Tax Regime for Freelancers and Business Owners

Self-employed individuals, consultants, and business owners operate under a different set of rules. The ability to claim business expenses rent, travel, depreciation, professional fees, and utilities as deductions against income makes tax planning more nuanced for this group.

For businesses with turnover up to ₹3 crore, the presumptive taxation scheme under Section 44AD is compatible with the new regime and offers simplicity without the burden of maintaining detailed books purely for deduction purposes. Similarly, professionals with receipts up to ₹75 lakh can opt for Section 44ADA presumptive taxation.

Importantly, your business structure whether you operate as a proprietorship, LLP (registered under the Ministry of Corporate Affairs), or private limited company significantly affects how income is taxed. The regime choice applies to individual promoters on their personal income; companies and LLPs are taxed under separate corporate rates and are not directly subject to the old vs new regime choice. Read our detailed guide on Company Formation and Tax Structuring for a complete breakdown.

A 5-Step Framework to Choose the Right Tax Regime Recommended by Dr. Haresh Adwani

Dr. Haresh Adwani recommends the following structured approach for every individual taxpayer before each financial year begins:

- Step 1 : Project your total income: Include salary, rental income, business income, capital gains, and any other sources for the year.

- Step 2 : List every deduction you will legitimately claim: HRA, 80C investments, 80D premiums, home loan interest, NPS, LTA, and any other applicable items.

- Step 3 : Compute net taxable income under both regimes: Subtract your applicable deductions from gross income under the old regime; subtract only the standard deduction and eligible items under the new regime.

- Step 4 : Apply slab rates to each and calculate total tax: Include surcharge (if applicable) and the 4% health and education cess as specified by the Income Tax Department.

- Step 5 : Choose the lower outcome and communicate it: Inform your employer before April 1 if you are salaried, or record your regime choice in your ITR filing.

This entire process, with a CA’s guidance, can be completed in under 30 minutes yet it directly determines how many thousands of rupees stay in your pocket every year.

Conclusion: Old vs New Tax Regime : Make a Decision, Not a Guess

The old vs new tax regime debate is not a philosophical discussion it is a mathematical calculation. And yet, year after year, lakhs of Indian taxpayers make this choice on instinct, peer advice, or sheer inertia.

Your tax planning is deeply personal. The deductions you claim, the salary structure you have, the investments you maintain these are unique to you. The regime that saves your colleague ₹45,000 could cost you ₹70,000, and vice versa. With the Income Tax Act, 2025 and the new default regime now in play, the consequences of an uninformed choice are larger than ever before. The framework is simple: project your income, list your deductions, calculate tax under both regimes, and choose the lower number. Do this before April 1 every year, communicate it to your employer, and revisit it annually as your income and life situation evolve

1: Which is better old vs new tax regime for a ₹10 lakh salary?

At ₹10 lakh gross salary, the answer depends on your deductions. If you claim HRA, 80C, and 80D, the old regime typically results in lower tax. If your deductions are minimal, the new regime’s lower rates may be beneficial. Always calculate both before deciding one size does not fit all.

2: Can I switch between old and new tax regime every year?

Yes, if you are a salaried employee. You can switch your regime preference every financial year by informing your employer or selecting the regime at the time of ITR filing. Taxpayers with business or professional income, however, can switch from the new regime to the old regime only once after reverting to the new regime, they cannot switch back.

3: Is HRA exempt in the new tax regime?

No. House Rent Allowance exemption under Section 10(13A) is not available in the new tax regime. For employees renting homes in metro cities where HRA forms a significant part of CTC, this is often the single biggest reason the old regime turns out cheaper.

4: What deductions are actually allowed in the new tax regime?

The new regime permits the standard deduction of ₹75,000 for salaried employees, employer NPS contributions under Section 80CCD(2) up to 14% of basic salary, and a few other specific allowances like transport and conveyance. Most other major deductions 80C, 80D, HRA, LTA, 24(b) home loan interest are not available.

5: Is income up to ₹12 lakh completely tax-free in 2025?

Under the new tax regime for FY 2025–26, taxpayers with income up to ₹12 lakh may enjoy zero tax liability due to the Section 87A rebate (rebate of up to ₹60,000). For salaried individuals, the ₹75,000 standard deduction additionally pushes the effective zero-tax threshold to ₹12.75 lakh. Eligibility depends on the specific nature of income consult a CA to confirm your individual situation.

6: What happens if I forget to inform my employer about regime choice?

Your employer will default to deducting TDS under the new regime. If the old regime would have resulted in lower tax for you, you may have excess TDS deducted throughout the year which you can claim as a refund when filing your return. Conversely, if the old regime results in higher tax and TDS has been deducted at new regime rates, you may face a tax demand at filing time. Informing your employer before the financial year begins avoids both scenarios.

7: Should I consult a CA to choose my tax regime?

Absolutely especially if your annual income exceeds ₹10 lakh, if you have business income, a home loan, HRA, NPS, or investment income. A qualified Chartered Accountant like those at Adwani and Company can conduct a precise, personalized comparison across both regimes and help you legally structure your income for maximum savings year after year.

About the Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.

Don’t leave money on the table. Don’t assume. Don’t defer. Run the calculation today and if you need expert guidance, Adwani and Company is ready to help.