The 120-Day Rule That Is Silently Taxing Thousands of NRIs in India :Are You at Risk?

Dr. Haresh Adwani April 2026 14 min read

Imagine spending decades building your career abroad, sending money home faithfully, and then one day discovering that a brief holiday visit to India has quietly triggered a massive tax liability on your global income. This is not a hypothetical scenario

It is the harsh reality being faced by thousands of Non Resident Indians (NRIs) who are completely unaware of the 120 day NRI tax rule in India. One seemingly harmless overstay, and you could find yourself reclassified as a tax resident, with your foreign salary, overseas investments, and global savings suddenly falling within the reach of the Indian Income Tax Department.

According to Dr. Haresh Adwani, of Adwani and Company a leading Chartered Accountancy firm trusted by NRIs across the globe this rule has become one of the most misunderstood and dangerous provisions in Indian tax law today. “We see clients every year who did not even know the 120-day threshold existed,” he says. “By the time they find out, the damage is already done.” This comprehensive guide breaks down the 120-day NRI residency rule in India, explains how NRI taxation works, and shows you exactly what steps to take to stay protected. You can check on Income Tax India

What Exactly Is the 120-Day NRI Tax Rule in India?

Before the Finance Act of 2020, the residency threshold for NRIs was straightforward: if you stayed in India for fewer than 182 days in a financial year (April 1 to March 31), you were classified as a Non-Resident Indian for tax purposes. Under this classification, only your income earned or received in India was taxable. Your overseas salary, foreign bank interest, and global investments were beyond the reach of Indian tax authorities.

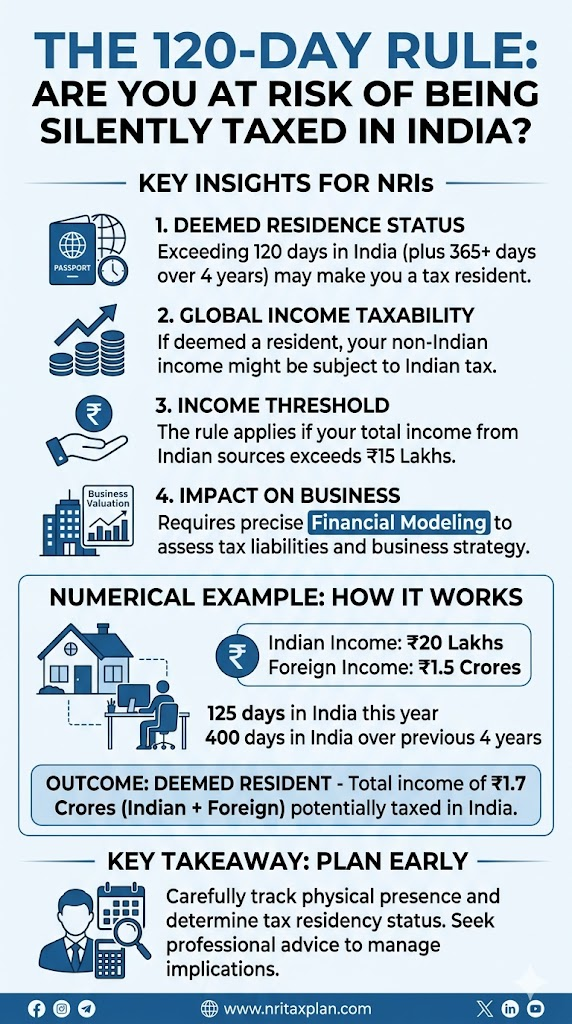

However, the Finance Act 2020 introduced a critical amendment that changed the game entirely for high-income NRIs. Under the revised rules, if your total taxable income from Indian sources exceeds ₹15 lakhs in a financial year, the residency threshold drops significantly from 182 days to just 120 days. In other words, if you earn more than ₹15 lakh from Indian sources (such as rent from Indian property, fixed deposit interest, capital gains on Indian investments, or salary for services rendered in India) and you stay in India for 120 days or more in that financial year, the Income Tax Department can classify you as a Resident but Not Ordinarily Resident (RNOR) and eventually even as a full Resident.

As the Income Tax Department of India notes under Section 6 of the Income Tax Act, 1961, an individual’s residential status is determined each financial year based on physical presence in India and other prescribed criteria. The 2020 amendment brought this provision into sharper focus for NRIs with substantial Indian income.

The Three Residential Status Categories Every NRI Must Know

Understanding the 120-day rule requires understanding how the Indian Income Tax Act classifies individuals into three distinct residential categories:

1. Non-Resident Indian (NRI)

An NRI is someone who does not qualify as a resident under the Income Tax Act. As an NRI, you pay taxes only on income that arises, accrues, or is received in India. Your foreign earnings are entirely outside Indian tax jurisdiction. This is the most tax-efficient status for Indians living abroad.

2. Resident but Not Ordinarily Resident (RNOR)

This is the middle ground and often where the 120-day NRI tax rule pushes unsuspecting NRIs. An RNOR is treated somewhat like a resident but still enjoys limited tax protection: foreign income is generally not taxable unless it is derived from a business controlled from India or a profession set up in India. You qualify as RNOR if you have been a non-resident for nine out of the ten preceding financial years, or if you have stayed in India for 729 days or fewer during the last seven financial years.

3. Resident and Ordinarily Resident (ROR)

This is the most tax heavy classification. As a full resident, your worldwide income salary earned in the UK, interest from US bank accounts, dividends from Canadian stocks all become taxable in India. This is why the 120-day rule can be so financially devastating for NRIs who unknowingly cross this threshold.

How the 120-Day NRI Residency Rule Works:

A Practical Example

Let us take the example of Mr. Rajesh Mehta, a software engineer based in Dubai for the past twelve years. He owns a flat in Mumbai that generates rental income of ₹18 lakhs per year, and he has a fixed deposit in an Indian bank earning additional interest of ₹2 lakhs annually. His total Indian taxable income is ₹20 lakhs well above the ₹15 lakh threshold.

In Financial Year 2023-24, Rajesh decided to extend his India visit due to a family function and medical check ups. Without realising it, his total stay reached 128 days. He also checks whether he spent 365 days or more in India during the preceding four financial years (FY 2019-20 to FY 2022-23). If he did say, due to COVID-related lockdowns he gets classified as RNOR for FY 2023-24.

As an RNOR, Rajesh still escapes full global income taxation for now. But if he continues to stay beyond the 182-day mark in subsequent years or fails to meet the RNOR conditions, he could quickly become a full resident and his Dubai salary, overseas savings, and international investments would all become taxable in India. A scenario Dr. Haresh Adwani describes as “a ticking tax time bomb that most NRIs do not even know is ticking.”

The Deemed Residency Trap: Even Zero Days in India Is Not Safe

Here is something that shocks most NRIs: you can be classified as a tax resident of India even if you did not step foot in the country during that financial year. This is what is known as the “deemed residency” provision under the Finance Act 2020.

If you are an Indian citizen whose total taxable Indian income exceeds ₹15 lakhs, and you are not liable to pay income tax in any other country (for example, if you reside in a tax-free jurisdiction like the UAE, Bahrain, or Qatar), then you will be automatically classified as a Resident but Not Ordinarily Resident in India even with zero days of physical presence.

This provision was specifically designed to close a longstanding loophole where high-earning Indians would move to tax-free countries, maintain their NRI status, and avoid paying taxes both in India and abroad. While the objective is logical, it has caught many well-intentioned NRIs completely off guard.

Adwani and Company has encountered several such cases where clients living in Dubai or Abu Dhabi with significant Indian rental or investment income were deemed Indian tax residents without ever realising it. According to Dr. Haresh Adwani, “The deemed residency rule is the hidden clause of the 120-day rule. Most NRIs in the Gulf region have never heard of it yet they may already be non-compliant.”

Also Read: Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

What Income Is Taxable for NRIs in India?

As long as you maintain your NRI status, the following types of income earned or received in India are taxable under the Indian Income Tax Act:

- Salary received in India or for services rendered in India

- Rental income from properties located in India

- Capital gains from the sale of Indian assets (property, shares, mutual funds)

- Interest earned on NRO (Non-Resident Ordinary) accounts NRE and FCNR account interest remains tax-free

- Dividends from Indian companies (now taxable in the hands of shareholders)

- Income from business or profession set up in India

- Any income received or deemed to be received in India

Importantly, interest earned on NRE accounts and FCNR deposits continues to be exempt from Indian taxation, even for returning NRIs, until they acquire the status of Resident and Ordinarily Resident. This makes strategic account management a key tool for NRI tax planning something the experts at Adwani and Company can help you navigate effectively.

Learn more about our NRI Taxation & Compliance Services https://www.adwaniandco.com/services/global-delivery-model

How to Calculate Your Days in India : And Why Precision Matters

Day counting sounds simple, but it is far more nuanced than most NRIs assume. The Income Tax Act requires that you count both the day of arrival and the day of departure as days spent in India. This means a visit from July 1 to December 31 which feels like six months is actually 184 days, not 183. A single day’s miscalculation near the 120-day boundary could be the difference between being an NRI and being reclassified.

Additionally, you need to look back at the four preceding financial years to determine whether your cumulative stay in India has crossed 365 days. Even if you stayed well under 120 days in the current year, a longer stay in earlier years could trigger residency classification when combined with your current year’s visit. This multi-year calculation is something that requires expert guidance, not guesswork.

Dr. Haresh Adwani recommends that every NRI maintain a detailed travel log flight tickets, boarding passes, hotel receipts, and entry/exit stamps to create a paper trail that can be presented to tax authorities if your residential status is ever questioned.

Smart Strategies to Stay Safe from the 120-Day NRI Tax Trap

If your Indian income is approaching or exceeds the ₹15 lakh mark, here are the key strategies that Dr. Haresh Adwani and the team at Adwani and Company recommend:

1. Monitor Your Days in India in Real Time

Do not wait until the end of the financial year to count your days. Use a travel tracker and set alerts when you approach the 100-day mark. This gives you a 20-day buffer to plan your departure before crossing the 120 day threshold.

2. Manage Your Indian Taxable Income Below ₹15 Lakhs

If your Indian income is close to ₹15 lakhs, consider restructuring it. For instance, investing in NRE fixed deposits rather than NRO deposits, or shifting rental income through tax-efficient vehicles, could help keep your taxable Indian income below the threshold that activates the 120 day rule.

3. Leverage the Double Tax Avoidance Agreement (DTAA)

India has signed Double Tax Avoidance Agreements (DTAAs) with over 90 countries. If you are residing in one of these treaty nations, you can submit a Tax Residency Certificate (TRC) from your country of residence to claim DTAA benefits and avoid double taxation. This is especially critical for NRIs who get reclassified as RNOR under the 120-day rule.

4. Time Your Return to India Strategically

If you are planning to return to India permanently, consider returning after October 2 of the financial year. This limits your days in India to under 182 during that transition year, potentially allowing you to retain NRI or RNOR status for one more year giving you time to restructure your overseas finances without global tax exposure.

Read our detailed guide on NRI Return to India Tax Planning https://www.adwaniandco.com/blog/nri-tax-rules-10-critical-questions-before-returning-to-india

What Changed with the Income Tax Bill 2025 : And How It Affects NRIs from April 2026

In February 2025, the Central Government introduced the Income Tax Bill 2025, a sweeping overhaul of India’s tax system. While the Bill retains the core NRI residency rules including the 120-day rule it brings significant structural simplifications. The bill consolidates the existing framework from 819 sections into 536 clauses, making compliance somewhat cleaner, but the substantive rules remain unchanged.

Key takeaways for NRIs under the new bill (effective April 1, 2026): The 120-day rule continues to apply for high-income NRIs with Indian income exceeding ₹15 lakhs. The deemed residency provision remains intact for Indian citizens in tax-free jurisdictions. RNOR status is preserved, ensuring foreign income remains untaxed at that intermediate stage. Enhanced tax recovery provisions mean authorities now have greater powers to recover dues from Indian assets of NRIs who fail to comply.

Given these strengthened enforcement mechanisms, proactive tax planning for NRIs is not optional it is essential. The professionals at Adwani and Company stay updated with every policy change from the Ministry of Finance, the Income Tax Department, and relevant government portals to ensure their NRI clients remain fully compliant.https://www.adwaniandco.com/

Conclusion

The 120day NRI tax rule in India is not just a technicality buried in the fine print of the Income Tax Act it is a real and growing tax risk for millions of NRIs worldwide. Whether you are a professional in the Gulf, a businessperson in the UK, or an IT consultant in the United States, if you earn significant income from India and visit home regularly, this rule directly affects your financial future.

The good news is that with the right planning precise day counting, income structuring, DTAA utilisation, and timely return filing you can legally and effectively protect your wealth from unintended Indian tax exposure. The critical first step is awareness, and the second is action.

Frequently Asked Questions

Q1. Who does the 120-day rule apply to?

The 120-day NRI tax rule applies to Indian citizens or Persons of Indian Origin (PIOs) whose total taxable income from Indian sources exceeds ₹15 lakhs in a given financial year. If you cross both the income threshold (₹15 lakhs) and the stay threshold (120 days or more in India), and have also spent 365 days or more in India in the preceding four years, you may be classified as RNOR.

Q2. What income counts toward the ₹15 lakh threshold?

Only income that is sourced from India counts rental income, capital gains from Indian assets, interest on NRO accounts, salary for services rendered in India, and dividends from Indian companies. Interest on NRE accounts and FCNR deposits is exempt and does not count toward the ₹15 lakh threshold.

Q3. If I am classified as RNOR, will my overseas salary be taxed in India?

Generally, no. As an RNOR, your foreign income salary earned abroad, interest from foreign banks, dividends from foreign companies is not taxable in India, unless it is derived from a business controlled from India or a profession set up in India. Only your Indian-sourced income is taxable during the RNOR phase.

Q4. I live in Dubai (a tax-free country). Am I automatically an Indian tax resident?

Not automatically, but potentially yes. Under the deemed residency provision, if you are an Indian citizen living in a tax-free country like the UAE and your taxable Indian income exceeds ₹15 lakhs, you will be classified as RNOR in India even if you did not visit India at all during that financial year. This is a crucial provision that NRIs in Gulf countries must be aware of.

Q5. Can I use a DTAA to avoid double taxation as an NRI?

Yes. India has DTAA agreements with over 90 countries. If you are a tax resident of a treaty nation, you can submit a Tax Residency Certificate (TRC) to claim DTAA benefits and avoid being taxed on the same income in both countries. This is one of the most effective tools for NRI tax optimisation and should be part of every NRI’s tax strategy.

Q6. Does the 120-day rule apply if my Indian income is below ₹15 lakhs?

No. If your taxable Indian income is below ₹15 lakhs, the old 182-day rule continues to apply. You can stay in India for up to 181 days without triggering residency. The 120 day threshold is triggered only when your Indian income crosses the ₹15 lakh limit.

Q7. Do I need to file an income tax return in India as an NRI?

Yes, if your annual Indian income before deductions and exemptions exceeds the basic exemption limit of ₹2.5 lakhs, you are required to file an Income Tax Return in India. The deadline is typically July 31 of the assessment year. Even if TDS has already been deducted, filing a return is often beneficial for claiming refunds or availing treaty benefits under the DTAA.

Author

Dr. Haresh Adwani

PhD (Commerce) · Adwani & Company, Pune

Dr. Haresh Adwani is a PhD holder in Commerce with over 20 years of experience in NRI taxation, FEMA compliance, international financial advisory, and tax notice resolution. He is one of Pune’s most trusted NRI tax advisors, specialising in residential status assessment, DTAA planning, and cross-border compliance for professionals returning from the US, UK, UAE, Canada, and Australia.