Form 16 for ITR Filing

Every June, millions of salaried employees across India receive one document from their employer and immediately assume their tax homework is done. That document is Form 16. And that assumption? It is one of the most common and costliest tax filing mistakes of the year.

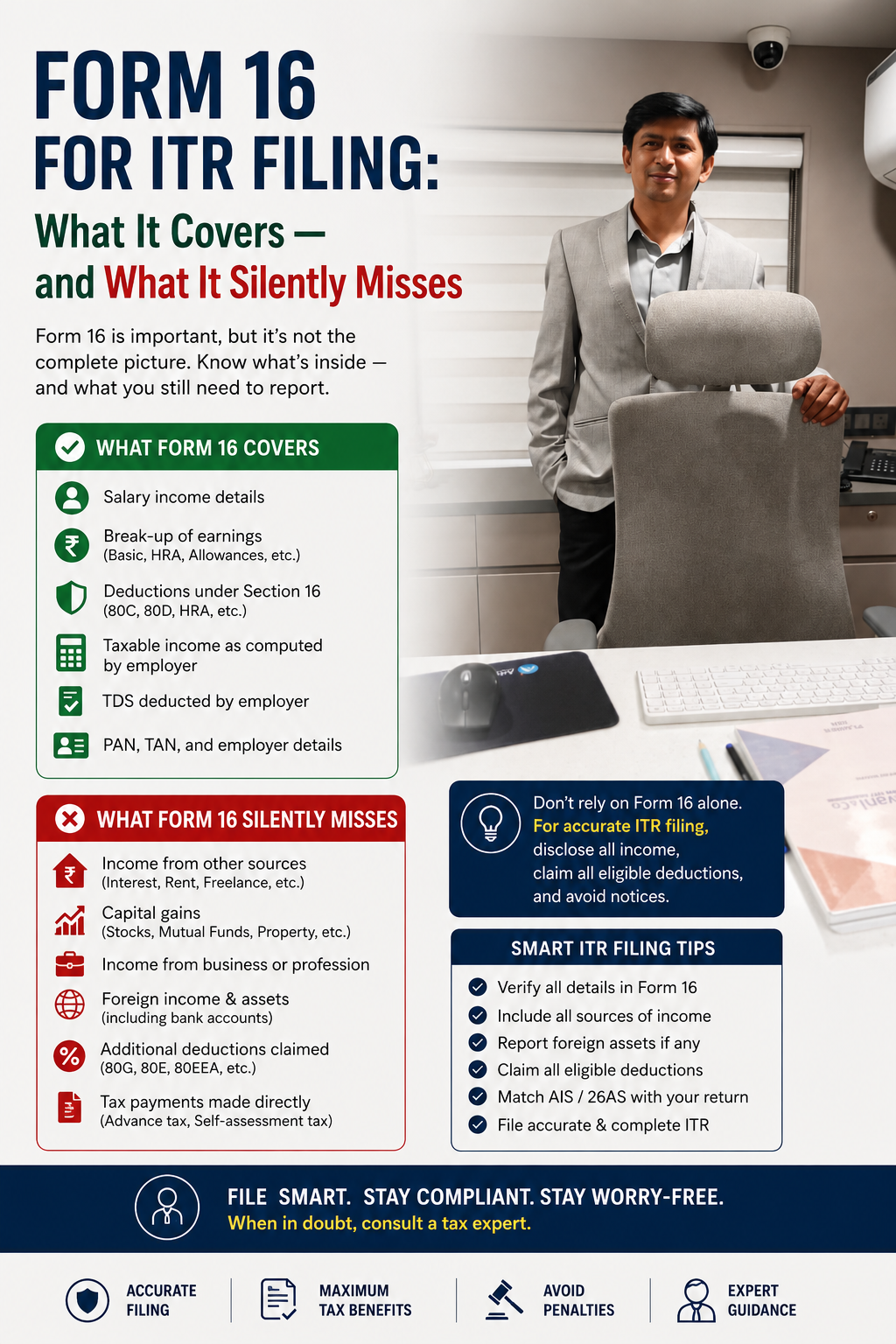

Form 16 for ITR filling is important. But it is not the complete picture. For AY 2026-27, filing your Income Tax Return based only on Form 16 can leave out significant taxable income, trigger a mismatch with your Annual Information Statement (AIS), and even invite an income tax notice. This guide breaks down exactly what Form 16 covers, what it misses, and what you must do before hitting ‘Submit’ on the income tax portal.

What Is Form 16 for ITR filling and Why Do Salaried Employees Receive It?

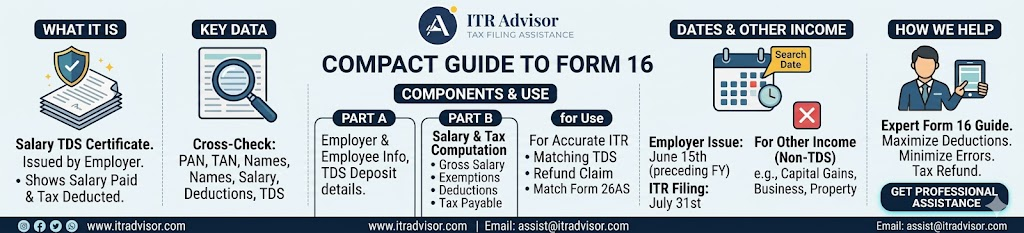

Form 16 is a TDS certificate issued by your employer under Section 203 of the Income Tax Act, 1961. It certifies the amount of tax deducted at source (TDS) from your salary and deposited with the government on your behalf. As per the Income Tax Department, every employer who has deducted TDS from salary payments is required to issue Form 16 to employees by June 15 of the assessment year.

The document has two parts:

Part A : The TDS Summary

Part A Covers:

- Employer and employee PAN and TAN details

- Quarter-wise TDS deducted and deposited

Certificate number issued by TRACES (the government’s TDS reconciliation portal

Part B : The Salary Breakdown

Part B Covers:

- Gross salary and allowances

- Exempt allowances (HRA, LTA, etc.)

- Deductions claimed under Chapter VIA (80C, 80D, 80G, etc.)

- Net taxable salary and final tax computed

Tax regime chosen (old or new)

Also Read our Detailed guide on :Old vs New Tax Regime 2025: Stop Guessing, Start Calculating

Together, Parts A and B give you a structured view of your salary income and the tax your employer calculated. But and this is critical Form 16 only reflects what your employer knows about your finances.

What Form 16 for ITR filling Does NOT Cover: Income That Belongs in Your ITR

This is where most salaried taxpayers go wrong when filing their ITR for AY 2026-27. Your employer can only deduct TDS on the salary they pay you. Any income earned outside of that employment relationship is completely invisible to them and therefore absent from Form 16.

Here is income that will not appear in your Form 16 but must be disclosed in your ITR:

- Interest income from savings accounts, fixed deposits, recurring deposits, and post office schemes often reported by banks to the Income Tax Department via Statement of Financial Transactions (SFT)

- Capital gains from the sale of shares, equity mutual funds, debt funds, or property taxed at different rates under LTCG and STCG rules

- Rental income from residential or commercial property let out during the year

- Freelance, consulting, or professional income earned over and above your salary

- Income from previous employers if you changed jobs during the financial year

- Dividend income from shares and mutual funds now fully taxable in the hands of the investor

- Winnings from online gaming, lottery, or other speculative sources

Practical Example: Ramesh is a salaried IT professional in Pune earning ₹14 lakh annually. His employer deducts TDS and issues Form 16 reflecting zero additional tax liability. However, Ramesh also has ₹85,000 in FD interest and ₹1.2 lakh in STCG from selling equity mutual funds. None of this appears in his Form 16. If he files his ITR based only on Form 16 and ignores these, his AIS (Annual Information Statement) will show the mismatch and the Income Tax Department may send him a notice under Section 143(1)(a) for under-reporting of income.

Form 16 vs AIS: Why a Mismatch Can Trigger an Income Tax Notice

The Income Tax Department’s AIS and Form 26AS now capture a comprehensive view of your financial transactions far beyond what your employer reports. Banks report interest income. Brokers report capital gains. Mutual fund houses report redemptions. Registrars report property transactions.

Before filing your ITR for AY 2026-27, always cross-verify your Form 16 with your AIS and Form 26AS available on the Income Tax e-filing portal. Any mismatch between what you declare and what the department already knows through third-party reporting can result in a defective return notice or tax demand.

If you find a discrepancy, the correct approach is to file an accurate return reflecting your true total income not simply what Form 16 shows.

How to File ITR Using Form 16 Correctly for AY 2026-27

Here is a structured approach for salaried employees to use Form 16 as a starting point not an endpoint for ITR filing:

Step 1: Download and Verify Form 16

Ensure your Form 16 has a valid TRACES watermark and matches the TDS reflected in your Form 26AS. Part A details must be TRACES-generated; do not accept manually typed versions from employers.

Step 2: Collect All Income Sources

Gather interest certificates from all banks and NBFCs, capital gains statements from your broker or mutual fund house (from Consolidated Account Statement), and rent receipts if applicable.

Step 3: Compute Total Income

Add all sources to your salary income from Form 16. This gives you your actual gross total income, which may be significantly higher than what Form 16 reflects.

Step 4: Choose the Right ITR Form

If you only have salary and interest income, ITR-1 applies. If you have capital gains, you need ITR-2. Business or professional income alongside salary means ITR-3 or ITR-4. Read our detailed guide on ITR-1 vs ITR-2 vs ITR-4 for AY 2026-27.

Step 5: File Before the Deadline

The ITR filing deadline for AY 2026-27 for salaried individuals is July 31, 2026. Late filing attracts a penalty under Section 234F of up to ₹5,000, plus interest under Section 234A on any tax due.

Key Takeaways

- Form 16 is issued by your employer and covers only your salary income and TDS it is the starting point for your ITR, not the complete picture.

- Income from FDs, capital gains, rent, freelancing, and dividends is NOT reflected in Form 16 but must be declared in your ITR.

- A mismatch between Form 16 and your AIS/Form 26AS can trigger an income tax notice under Section 143(1)(a).

- Always verify your Form 16 against your AIS before filing. The ITR deadline for AY 2026-27 is July 31, 2026.

Choose the right ITR form based on your complete income not just your salary.

As Dr. Haresh Adwani, PhD in Commerce and a practicing law graduate with decades of tax advisory experience, often emphasizes to his clients: “Form 16 tells you what your employer reported. Your ITR must tell the government the complete truth and those two numbers are rarely the same for most urban professionals.”

Frequently Asked Questions

1. Is Form 16 mandatory to file ITR for salaried employees?

Form 16 is not legally mandatory to file ITR, but it is the most reliable document to report salary income accurately. You can file using salary slips and Form 26AS if your employer has not issued Form 16.

2. Can I file ITR using only Form 16 without checking AIS?

Filing without checking your AIS is risky. The Income Tax Department uses AIS data to auto-verify returns, and any mismatch can result in a defective return notice or demand for additional tax.

3. What income is not included in Form 16 for ITR filing?

FD interest, savings account interest, capital gains on shares and mutual funds, rental income, dividend income, and freelance earnings are not included in Form 16 and must be added separately while filing ITR.

4. What happens if I file ITR based only on Form 16 and miss other income?

The Income Tax Department may issue a notice under Section 143(1)(a) for under-reporting. You may also face additional tax demand with interest under Sections 234A, 234B, and 234C.

5. Which ITR form should I use if I have capital gains along with salary income?

If you have capital gains (LTCG or STCG) from shares or mutual funds along with salary, you must file ITR-2. ITR-1 does not allow disclosure of capital gains income.

Conclusion:

Form 16 is one of the most important tax documents an Indian salaried employee receives. But treating it as the only input for your Income Tax Return is a mistake that thousands of taxpayers repeat every year. From capital gains on mutual fund redemptions to bank FD interest quietly accumulating in your accounts your total taxable income is almost always larger than what your employer has captured.

Filing an accurate, complete ITR protects you from notices, demands, and penalties and ensures you claim every refund you legitimately deserve. Take the time this season to check your AIS, gather all income sources, and file a return that truly reflects your financial year.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

Need Help with NRE/NRO Taxation?

Whether you are an NRI, OCI holder, overseas employee, or a returning Indian, understanding the tax implications of NRE and NRO accounts is critical.

At ITRAdvisor.in, we help NRIs and returning Indians with:

✔️ NRE and NRO taxation

✔️ Residential status determination

✔️ Returning NRI tax planning

✔️ DTAA advisory

✔️ Foreign asset reporting

✔️ NRI Income Tax Return filing

✔️ Tax notice handling

✔️ Capital gains and property taxation

If you are unsure whether your NRE interest is taxable, whether you need to file an ITR in India, or how to handle NRO income, professional guidance can help avoid costly mistakes.

Visit ITRAdvisor.in to schedule a consultation and get clarity on your NRI tax obligations.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

A prominent “File Your ITR Now” button near the top and again at the end of the article.

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.