Section 143(2) Notice After ITR-U

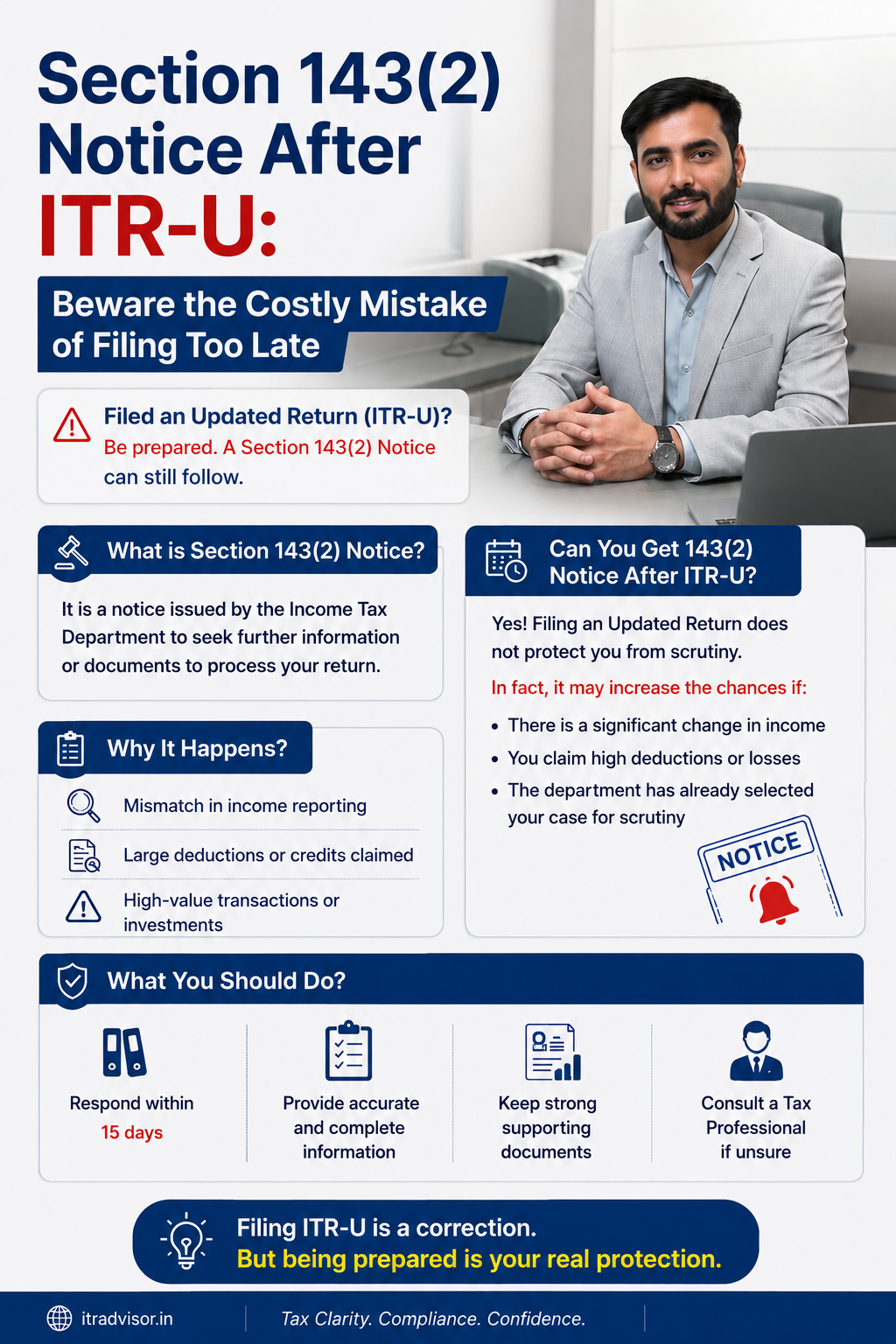

You filed an ITR-U an Updated Return under Section 139(8A) thinking you had corrected your earlier mistake. You breathed easy. Then, a few weeks later, a notice arrived: Section 143(2). Your stomach dropped. If this sounds familiar, you are not alone. Thousands of taxpayers across India are receiving income tax scrutiny notices after filing updated returns, and most of them made one simple but costly mistake they filed too late, or without fully understanding what triggers a 143(2) notice in this context.

What Is Section 143(2) and Why Does It Follow Your ITR-U?

Section 143(2) of the Income Tax Act, 1961 empowers the Assessing Officer (AO) to issue a scrutiny notice when the department believes a return needs closer examination. This is not a penalty it is an invitation to prove that the income you declared is correct and supported by evidence.

When a taxpayer files an ITR-U (Updated Return) under Section 139(8A), the Income Tax Department does not automatically accept the revised figures. In fact, according to the Income Tax Department’s procedural guidelines, updated returns are subject to a higher level of automated and manual scrutiny precisely because they represent a change from the originally filed return.

In plain terms: filing an ITR-U places your return under a magnifying glass. And if the department finds discrepancies in income, deductions, or timing a 143(2) scrutiny notice is almost inevitable.

The Costly Mistake: Filing Your ITR-U Too Late

Section 139(8A) allows a taxpayer to file an updated return within 24 months from the end of the relevant assessment year but each passing year comes with a higher additional tax burden:

| When ITR-U is Filed | Additional Tax Payable | Scrutiny Risk Level |

| Within 12 months from end of AY | 25% of additional tax + interest | Moderate |

| Between 12–24 months from end of AY | 50% of additional tax + interest | High |

| After 24 months (not permitted) | Not allowed under law | Return Invalid |

This table tells a clear story: the later you file, the more you pay and the greater the chance of receiving a Section 143(2) notice after filing the ITR-U. The Income Tax Department’s systems are calibrated to flag late updated returns for scrutiny because they often indicate suppression of income in the original filing.

Important Warning

A Section 143(2) notice after filing ITR-U must be responded to within the time specified in the notice typically 15 to 30 days. Failure to respond can lead to ex-parte assessment under Section 144, which can result in a best-judgment assessment with significantly higher tax demand.

Income Tax Notice Time Limit: What the Law Says for 143(2)

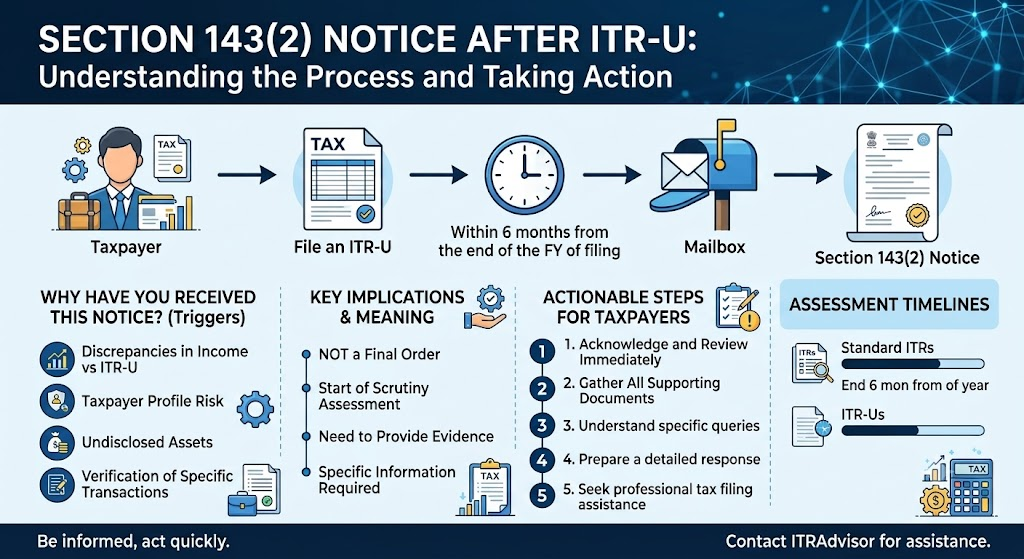

Under the Income Tax Act, the Assessing Officer must issue a Section 143(2) notice within six months from the end of the financial year in which the return was filed. This time limit applies to ITR-U as well. So if you filed your updated return in August 2024 (FY 2024-25), the department has time until 30 September 2025 to issue the 143(2) notice.

This income tax notice time limit is a critical legal protection for taxpayers. If a notice is issued beyond this window, it can be challenged. However, this requires prompt action ideally with professional guidance as courts have strict timelines for such objections.

Read our detailed guide on Income Tax Notice Time Limit to understand exactly when the department’s power to scrutinise expires.

How to Respond to a Section 143(2) Notice After Filing ITR-U

Receiving this notice does not mean you are in trouble — but ignoring it certainly will put you in trouble. Here is the step-by-step response process:

Step 1: Read the Notice Carefully

The notice will specify the assessment year under scrutiny, the issues flagged (income mismatch, deduction claims, etc.), and the deadline to respond. Identify whether the notice relates to your original ITR or the ITR-U specifically.

Step 2: Gather Supporting Documents

Compile Form 16, Form 26AS, AIS (Annual Information Statement), bank statements, investment proofs, and any other documents supporting the income and deductions declared in your updated return. Cross-check your ITR-U with these documents before submitting anything.

Step 3: Respond Through the E-Proceedings Portal

All responses to 143(2) scrutiny notices must be submitted through the Income Tax e-Filing portal (incometax.gov.in) under the ‘Pending Actions’ section. Physical responses are not accepted. Upload all documents clearly labelled and respond to each query point-by-point.

Step 4: Seek Professional Guidance

Income tax scrutiny proceedings can be complex, especially where they involve an updated return. According to Dr. Haresh Adwani, a seasoned tax professional with decades of experience in Indian tax compliance, “taxpayers who respond to 143(2) notices without professional support often provide more information than required, inadvertently opening new lines of inquiry for the Assessing Officer.”

Expert Tip

When responding to a Section 143(2) notice after ITR-U filing, always submit documents that directly address the query nothing more. Over-disclosure is a common mistake that extends scrutiny timelines unnecessarily. Learn more about our Tax Notice Response Service at ITRAdvisor.in.

Can You Avoid a 143(2) Notice After Filing ITR-U?

Not entirely the department has the right to scrutinise any return. But you can reduce the risk significantly by following these practices:

- File the ITR-U as early as possible within 12 months of the assessment year end if you can, when the additional tax burden is lower and scrutiny flags are fewer.

- Ensure full consistency between the ITR-U and your AIS/Form 26AS. Any mismatch between the two is a primary trigger for income tax scrutiny after an updated return.

- Disclose all income correctly partial disclosure in an ITR-U is treated very seriously by the department and can lead to income tax reassessment notice under Section 148 as well.

- Keep documentary evidence ready before you file, not after.

- Do not use the ITR-U to claim additional refunds the provision is specifically for taxpayers who have under-reported income or missed declaring income, not for claiming higher refunds.

READ OUR deTAILED GUIDE ON Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Key Takeaways

• ITR-U (Updated Return) under Section 139(8A) can be filed within 24 months from the end of the assessment year but later filing means higher tax burden and greater scrutiny risk.

• A Section 143(2) notice after ITR-U is issued when the department needs to verify the accuracy of your updated return.

• The income tax notice time limit for issuing 143(2) is six months from the end of the financial year in which the ITR-U was filed.

• Always respond through the Income Tax e-Filing portal (incometax.gov.in) within the deadline specified in the notice.

• Seek professional guidance before responding over-disclosure can create new problems in scrutiny proceedings.

• Filing ITR-U within 12 months is always preferred to minimise both cost and scrutiny risk.

Frequently Asked Questions (FAQs)

Q1. Can I get a Section 143(2) notice after filing ITR-U even if my return was complete?

Yes. Filing an ITR-U automatically flags your return for enhanced scrutiny. The department issues 143(2) notices based on automated and manual risk parameters, regardless of whether your updated return appears complete.

Q2. What is the income tax notice time limit for Section 143(2) after ITR-U?

The Assessing Officer must issue the 143(2) notice within six months from the end of the financial year in which the updated return was filed. Any notice issued beyond this period can be legally challenged.

Q3. What happens if I do not respond to the income tax scrutiny notice after ITR-U?

Non-response can result in an ex-parte assessment under Section 144, where the AO makes a best-judgment assessment often resulting in a much higher tax demand than what you actually owe.

Q4. Can filing ITR-U trigger an income tax reassessment notice under Section 148 as well?

Yes. If the department believes that income has been under-disclosed even in the ITR-U, they can initiate reassessment proceedings under Section 148. This is why accurate and complete disclosure in the ITR-U is essential.

Q5. Is it better to file ITR-U within 12 months or wait for 24 months?

Always file within 12 months if possible. The additional tax is lower (25% vs 50%), and earlier filing generally attracts less scrutiny compared to returns filed closer to the 24-month deadline.

Conclusion: Don’t Let Timing Become Your Tax Trap

The ITR-U provision was introduced to give taxpayers a second chance — to correct errors and come clean with the Income Tax Department. But this second chance comes with strings attached. A Section 143(2) notice after filing an updated return is not a punishment; it is the department doing its job. What matters is how prepared and professional your response is.

The single most important lesson here: do not delay your ITR-U. The longer you wait, the more you pay, and the greater the scrutiny you face. If you have already received a 143(2) notice, do not panic — but do not delay your response either.

📞 Get Expert Help Today

Confused by a Section 143(2) notice after filing ITR-U? Not sure how to respond without triggering further scrutiny?

Connect with the experts at ITRAdvisor.in today. Our professionals bring deep experience in income tax notice resolution, updated return compliance, and scrutiny proceedings — so you can respond with confidence. Visit: www.itradvisor.in | Expert tax guidance, simplified.

Author

CA. Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services.

Whether you have already received a credit card income tax notice or want to ensure you never do Adwani and Company is your trusted partner. Led by Dr. Haresh Adwani and a seasoned team of Chartered Accountants, Adwani and Company provides end-to-end income tax compliance, notice response, and financial planning services.

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform.The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP