25 June 2026•Dr. Haresh Adwani

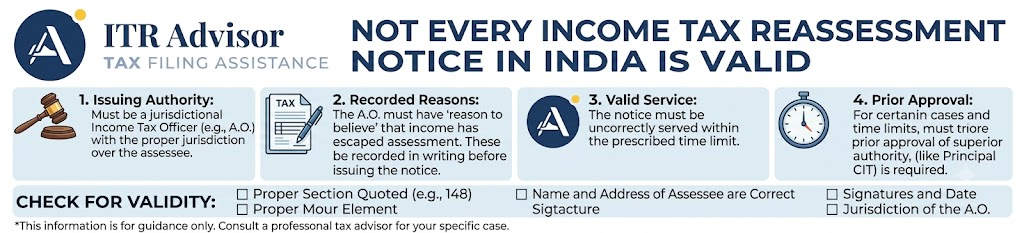

Not Every Income Tax Reassessment Notice in India Is Valid

You receive a notice from the Income Tax Department. Your first reaction? Panic. But here’s what most Indian taxpayers don’t know: not every income tax reassessment notice is legally valid. Many are issued outside the permitted time limit, without sufficient reason, or in violation of mandatory procedural safeguards. If you’ve received a Section 148 or Section 148A notice, you have every right and sometimes a strong legal case to challenge it before even responding on merit.

What Is an Income Tax Reassessment Notice Under Section 148?

Under the Income Tax Act, 1961 (applicable for AY 2025-26 and earlier; the Income Tax Act 2025 governs from AY 2026-27 onwards), the Assessing Officer (AO) can reopen a previously assessed return if they have “reason to believe” that income has escaped assessment. This is the legal basis for issuing a reassessment notice commonly referred to as a Section 148 notice or income tax reopening notice.

However, the Income Tax Department cannot simply reopen any year at will. The law imposes strict time limits and procedural conditions that must be satisfied before any valid reassessment notice can be issued. A failure to comply with even one of these conditions renders the income tax reassessment notice legally void.

Income Tax Reassessment Notice Time Limit: The Law Under Section 149

The income tax notice time limit for reopening an assessment is one of the most important safeguards available to taxpayers. As per Section 149 of the Income Tax Act, 1961:

Section 149 : Reassessment Time Limits Up to 3 years from end of relevant Assessment Year: General cases (escaped income up to ₹50 lakh) Up to 10 years from end of relevant AY: Cases where escaped income is ₹50 lakh or more AND the AO has ‘information’ as defined under Section 148 Note: No reassessment can be initiated beyond these limits, even if income has genuinely escaped.

Any income tax reassessment notice issued beyond the above income tax notice time limit is barred by limitation and is liable to be quashed a position consistently upheld by the Supreme Court and various High Courts across India.

The Mandatory Section 148A Process: Did the AO Follow It?

The Finance Act 2021 introduced a critical pre-notice safeguard Section 148A which made the reassessment process significantly more taxpayer-friendly. Before issuing a Section 148 reopening notice, the Assessing Officer is now required to:

- Provide the taxpayer with a copy of the ‘information’ that triggered the inquiry

- Issue a show-cause notice under Section 148A(b) and give the taxpayer a minimum 7-day opportunity to respond (extendable to 30 days)

- Consider the taxpayer’s reply and pass a reasoned order under Section 148A(d) before issuing the Section 148 notice

If the AO skips or short-circuits this Section 148A process, the subsequent income tax reassessment notice is procedurally defective and legally challengeable. This is not a technicality — it is a statutory mandate enforced by multiple High Court rulings

3 Grounds on Which an Income Tax Reopening Notice Can Be Challenged

1. Notice Issued Beyond the Limitation Period

If the income tax reassessment notice arrives after the income tax notice time limit prescribed under Section 149, you can challenge it on grounds of limitation before the AO, and if rejected, before the ITAT or High Court via writ jurisdiction.

2. No Tangible Material or ‘Escapement of Income’

The AO must have concrete, credible information not mere suspicion or a fishing expedition to believe income has escaped assessment. The Supreme Court in landmark rulings has held that ‘reason to believe’ must be based on tangible material. A reassessment notice based on change of opinion about already-disclosed income is invalid.

3. Non-Compliance with Section 148A Mandatory Procedure

As discussed, failure to follow the Section 148A show-cause notice procedure before issuing a Section 148 income tax reassessment notice is a fatal procedural error that courts have used to quash such notices.

Real-World Example

Scenario: Mr. Ramesh filed his ITR for AY 2019-20. In March 2026, he receives a Section 148 notice for that year, claiming escaped income of ₹8 lakh.

Issue: AY 2019-20 falls beyond the 3-year general limit from March 2026, and the escaped income is under ₹50 lakh — so the 10-year extended limit does not apply. Result: This income tax reassessment notice is barred by limitation and can be successfully challenged.

Read our detalied guide on Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

What Should You Do If You Receive an Invalid Income Tax Reassessment Notice?

- Do not ignore the notice file a reply within the stipulated time, even while challenging its validity

- Raise preliminary legal objections regarding the income tax notice time limit and procedural defects in your written reply

- Rely on the Supreme Court’s ruling in GKN Driveshafts (India) Ltd. vs. ITO (2003) the AO must dispose of objections before proceeding

- If the AO overrules your objections without valid reasons, approach the High Court via a writ petition

- Consult a qualified tax professional to assess the strength of your challenge

Key Takeaway

- Not every income tax reassessment notice in India is valid or enforceable.

- Check the date: Is the notice within the income tax notice time limit under Section 149?

- Check the process: Did the AO follow the mandatory Section 148A procedure?

- Check the basis: Is there a tangible, specific reason — not mere suspicion?

If any of these conditions are not met, the income tax reopening notice may be legally challenged and quashed. Source: Income Tax Department (incometax.gov.in) and CBDT Circulars on Reassessment Guidelines.

Frequently Asked Questions

Q1. What is the time limit to receive an income tax reassessment notice under Section 149?

For escaped income up to ₹50 lakh, the reassessment notice must be issued within 3 years from the end of the relevant Assessment Year. For escaped income of ₹50 lakh or more (with prescribed information), the limit is 10 years.

Q2. Can I challenge an income tax reassessment notice on legal grounds without replying on merits?

Yes. You can raise preliminary legal objections such as limitation or procedural defects in your reply. The AO is bound to pass a speaking order on these objections before proceeding with reassessment.

Q3. Is Section 148A mandatory before every income tax reopening notice?

Yes. Post-Finance Act 2021, the Section 148A show-cause procedure is mandatory before a Section 148 notice can be validly issued. Skipping it is a fatal procedural defect.

Q4. What happens if I ignore an income tax reassessment notice?

Ignoring the notice does not make it go away it can lead to ex-parte assessment and hefty demand. Always respond within time, even if you are challenging its validity.

Q5. Can a reassessment notice be issued for a year where income was already disclosed?

No. The Supreme Court has ruled that a reassessment notice based on a mere change of opinion where the income was already disclosed and examined is invalid and liable to be quashed.

Conclusion:

An income tax reassessment notice can be intimidating but it is not automatically final or correct. The Income Tax Act provides robust safeguards: a strict income tax notice time limit under Section 149, mandatory procedural steps under Section 148A, and the requirement of tangible material before reopening. As tax expert Dr. Haresh Adwani has consistently emphasized, taxpayers must evaluate every reassessment notice for legal validity before responding on merit because a legally defective notice deserves a legal challenge, not just a compliance reply.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP. pant, or someone navigating all three simultaneously — your tax treatment, ITR form selection, and loss utilisation strategy need to be correct, consistent, and complete.

Learn more about our Income Tax Filing Services for Traders & Investors — covering ITR-3 filing, tax audit support under Section 44AB, F&O turnover calculation, and capital gains reconciliation with your broker’s statement.

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later

If you or someone you know has received a Section 148 income tax reassessment notice, do not panic but do act quickly and smartly. The law is on your side, provided you know where to look.

📞 Take Action Today

Need help evaluating whether your income tax reassessment notice is valid?

Connect with the experts at itradvisor.in for a detailed assessment of your notice, legal objection drafting, and end-to-end reply support. Visit: www.itradvisor.in | Powered by Adwani & Co LLP