10 June 2026• Haresh Adwani

NRI International Tax India 2026

A person can live in one country, earn income in another, invest in a third and still get their taxes completely wrong. That is not an exaggeration. It is the reality for thousands of NRIs and globally mobile professionals navigating India’s international tax landscape in 2026.

NRI international tax in India is no longer a niche concern limited to large corporations or ultra high net worth individuals. Remote work, cross-border investments, overseas employment, and returning Indians have brought concepts like DTAA, FEMA compliance, tax residency, and foreign asset disclosure into everyday financial planning.

And the Income Tax Department, through enhanced data sharing with foreign jurisdictions and AI driven scrutiny, is paying closer attention than ever before.

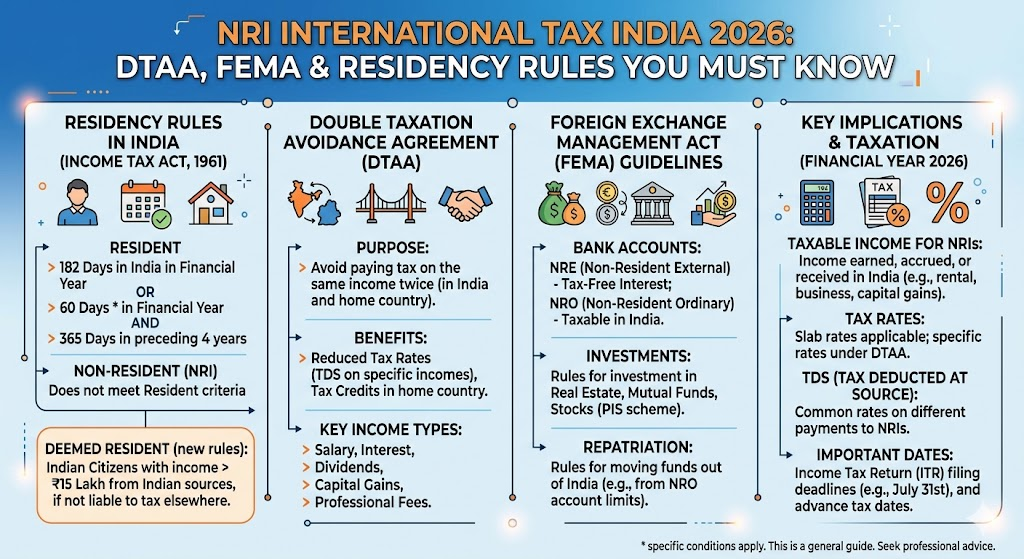

NRI Residency Rules India 2026: The Foundation of Everything

Before any tax planning, one question must be answered correctly: are you an NRI under the Indian Income Tax Act for the relevant financial year?

Your residential status determines which income is taxable in India. Get it wrong, and every deduction, DTAA claim, and exemption you rely on may unravel.

NRI Residency Rules India 2026 : Quick Reference

Resident (ROR): Present in India ≥ 182 days in the FY, OR ≥ 60 days in the FY + ≥ 365 days across the prior 4 years. All global income taxable in India.

NRI: Does not meet the above thresholds. Only India-sourced income is taxable.

RNOR (Resident but Not Ordinarily Resident): Transitional status for returning NRIs. Foreign income largely exempt for 2–3 years after return.

120-Day Rule (2020 onwards): An Indian citizen earning above ₹15 lakh from Indian sources who is not taxable in any country becomes a deemed resident. The 120-day rule was introduced to prevent ‘stateless’ tax planning.

The 120 day NRI rule, introduced to counter residency manipulation, has quietly increased the tax exposure of many professionals who assumed they were safe staying under the traditional 182 day threshold. If you are in this category, your stay planning requires careful day-counting and documentation.

Read our detailed guide on NRI Residency Rules and the 120-Day Rule Explained.

DTAA India 2026: How to Claim Your Tax Treaty Benefits Correctly

India has Double Taxation Avoidance Agreements (DTAA) with over 90 countries. For NRIs earning in India whether through dividends, interest, capital gains, or professional fees a DTAA can significantly reduce withholding tax rates and prevent the same income from being taxed twice.

But DTAA benefits in India are not automatic. To claim them, you need:

- A valid Tax Residency Certificate (TRC) from the country of your tax residence

- Form 10F filed with the Indian tax authorities

- A self-declaration confirming beneficial ownership of the income

- Disclosure in your Indian ITR if filing is required

One of the most common and expensive errors NRIs make is assuming the lower DTAA rate will be applied automatically by the payer. It will not unless you have submitted the required documentation before payment. Without it, TDS is deducted at the standard Indian rate (often 20–30%), and a refund claim requires filing an ITR and going through the refund process.

Foreign Asset Disclosure and Schedule FA in ITR: Non Negotiable for Residents

Once your residential status changes to Resident (ROR), a critical obligation kicks in: declaring all foreign assets in Schedule FA of your ITR, regardless of whether those assets generate income.

This includes overseas bank accounts, foreign securities and mutual funds, immovable property abroad, beneficial ownership in foreign entities, and signing authority over foreign accounts. Failure to disclose attracts severe penalties under the Black Money (Undisclosed Foreign Income and Assets) Act with a base penalty of ₹10 lakh per undisclosed asset.

As per disclosures and compliance frameworks available through the Income Tax Department portal (incometax.gov.in), India now participates in the Common Reporting Standard (CRS) and FATCA information exchange. The department receives foreign financial account data from over 100 countries annually. This is not a theoretical risk.

FEMA Compliance for NRIs: The Non-Tax Obligation That Gets Ignored

Most NRIs focus on income tax. Few give equal attention to FEMA the Foreign Exchange Management Act which governs how Indian residents hold and manage foreign assets, bank accounts, and investments.

Key FEMA obligations that NRIs frequently mismanage:

- NRE and NRO accounts must be re-designated or closed when an NRI returns to India and becomes a resident this must happen within a specific timeline

- Overseas Direct Investment (ODI) and Overseas Portfolio Investment (OPI) have separate RBI-governed limits and reporting requirements

- Immovable property acquired abroad or in India must comply with FEMA’s acquisition and repatriation provisions

- Failure to comply with FEMA can result in penalties up to three times the value of the transaction involved

RBI guidelines on FEMA compliance (available at rbi.org.in) are detailed, and NRIs dealing with large offshore account balances or cross-border investment structures need to treat FEMA compliance as seriously as income tax planning.

NRI Returning to India: Tax Checklist for 2026

Returning to India after years abroad triggers a series of tax and compliance obligations that most people underestimate. The RNOR status is a valuable transitional protection under it, foreign income is largely not taxable in India for 2–3 years depending on your prior NRI history. But it must be claimed correctly and documented.

According to Dr. Haresh Adwani, a PhD holder in Commerce and law graduate whose practice at Adwani & Co LLP covers NRI and cross-border tax advisory, the most common mistake returning NRIs make is treating the RNOR window as automatic protection without understanding what ‘foreign income’ actually means for this purpose and what income from India-based sources remains taxable throughout.

| NRI Returning to India : Key Tax Obligations ✔ Determine RNOR status eligibility based on prior NRI years ✔ Re-designate NRE/NRO accounts to resident accounts within the deadline ✔ Begin disclosing all foreign assets in Schedule FA from the first year of ROR status ✔ Evaluate DTAA implications for income continuing to arrive from the previous country of residence ✔ Review FEMA permissions for continued holding of overseas investments |

Read our complete NRI Returning to India Tax Checklist — RNOR Status, NRE/NRO, and FEMA Rules.

Key Takeaways

| NRI International Tax India 2026 : What to Remember ✔ Residential status is the starting point get it right before any tax planning. ✔ The 120-day rule has made day counting critical for Indian citizens with global income above ₹15 lakh. ✔ DTAA benefits require advance documentation TRC, Form 10F, and beneficial ownership declaration. ✔ Foreign asset disclosure in Schedule FA is mandatory for all ROR residents, with severe penalties for non-disclosure. ✔ FEMA compliance is a separate obligation from income tax — and equally important for NRIs holding offshore accounts or returning to India. ✔ RNOR status provides a transitional window for returning Indians — but it must be claimed and managed correctly. |

Conclusion:

The world has become genuinely borderless for income, investment, and mobility. Indian tax law through residency provisions, DTAA frameworks, FEMA regulations, and foreign asset disclosure requirements has evolved to reflect that reality. The question is whether your tax planning has kept pace.

For NRIs, returning Indians, digital nomads, and globally mobile professionals, NRI international tax in India 2026 is not a topic you can afford to leave to assumptions. The Income Tax Department’s data exchange partnerships, the introduction of the 120-day deemed residency rule, and the penalties under the Black Money Act have raised the stakes considerably.

Understanding the rules and acting on them before a notice arrives is always less costly than responding to one after.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.