10 June 2026• Nidhi Adwani

Section 139(9) Defective Return Notice Received?

Have you received an email or SMS from the Income Tax Department stating that your Income Tax Return (ITR) is “Defective” under Section 139(9) of the Income Tax Act?

Don’t panic.

A Section 139(9) Notice does not automatically mean that you have concealed income or committed tax evasion. However, it is a notice that requires immediate attention because failure to respond within the prescribed time may result in your Income Tax Return being treated as invalid.

In simple terms, it may be as if you never filed your return at all.

In this article, we explain what a Section 139(9) Defective Return Notice means, why it is issued, common reasons, real-life examples, and how to respond correctly.

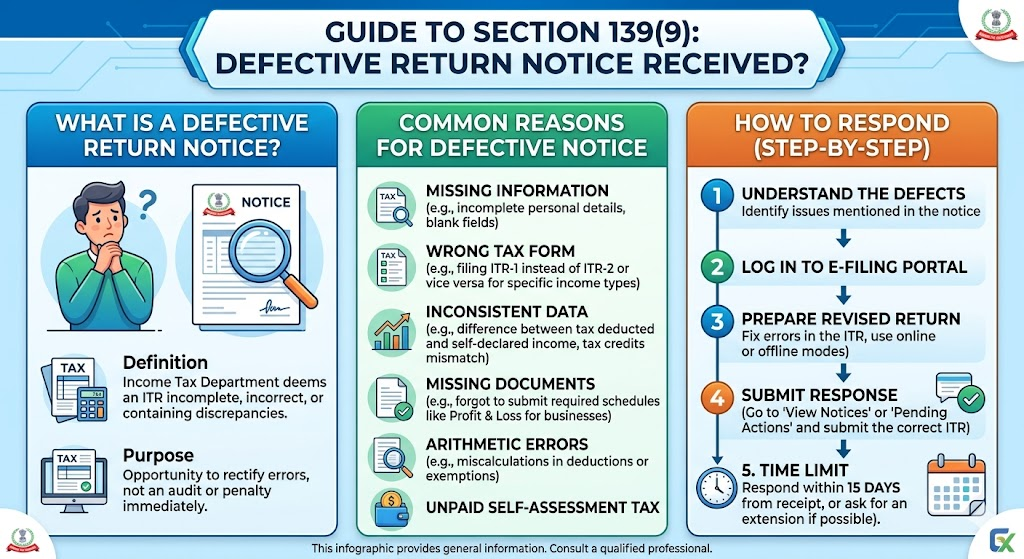

What is a Section 139(9) Defective Return Notice?

A Section 139(9) Notice is issued when the Income Tax Department finds defects, inconsistencies, omissions, or incomplete information in the Income Tax Return filed by a taxpayer.

The department provides an opportunity to correct the defect within the prescribed period.

Once the defect is corrected and submitted, the return continues to be treated as a valid return.

However, if the defect is not corrected, the return may become invalid.

Why is a Section 139(9) Defective Return Notice Issued?

The Income Tax Department processes millions of returns every year using automated systems.

If certain information is missing or inconsistent, a defective return notice may be generated.

Common Reasons for Section 139(9) Notice

- Wrong ITR Form Selected

This is one of the most common mistakes.

Example:

A taxpayer sold mutual funds and earned capital gains but filed ITR-1 instead of the appropriate ITR form.

The department may issue a defective return notice.

- Business Income Not Properly Reported

Taxpayers declaring business or professional income may fail to provide mandatory financial details.

Example:

A consultant reports professional income but does not provide the required Profit & Loss Account information.

- Mismatch Between Income and TDS

Income reported in the return may not match TDS information available in Form 26AS.

- Missing Balance Sheet Details

In some cases, taxpayers are required to disclose balance sheet information but fail to do so.

- Incomplete Capital Gains Reporting

Sale transactions may be reported without proper capital gains computation.

- Incorrect Claim of Losses

Business losses or capital losses may be claimed without furnishing required details.

- Incomplete Foreign Asset Reporting

Taxpayers required to disclose foreign assets may fail to provide complete information.

Also Read :Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Real-Life Example of a Section 139(9) Notice

Case Study:

Salaried Employee with Mutual Fund Transactions

Mr. Rahul, a software engineer from Pune, filed his Income Tax Return using ITR-1 because he believed he only had salary income.

However, during the financial year he had redeemed mutual funds worth ₹8 lakh.

Although the actual capital gain was small, the transaction itself required reporting under the appropriate ITR form.

A few weeks after filing, he received a Section 139(9) Defective Return Notice stating that the return was defective due to the use of an incorrect ITR form.

After reviewing the notice, the return was corrected and re-submitted using the correct form within the prescribed time.

The matter was resolved without penalty.

What Happens if You Ignore a Section 139(9) Notice?

Ignoring a defective return notice can create serious consequences.

The Income Tax Department may treat the return as invalid.

This can lead to:

- Loss of refund claims

- Late filing consequences

- Interest liability

- Loss of carry-forward of losses

- Additional compliance issues

In simple words, it may be treated as if no valid return was filed

How to Respond to a Section 139(9) Notice?

Step 1: Read the Notice Carefully

Identify the exact defect mentioned by the department.

Step 2: Download the Notice

Review all instructions and defect codes.

Step 3: Gather Required Information

Depending on the defect, you may need:

- Form 16

- AIS

- Form 26AS

- Capital gains statements

- Business records

- Foreign asset information

Step 4: Correct the Defect

Update the return and provide the information requested by the department.

Step 5: Submit Response Within Time

Always ensure that the response is submitted within the specified timeline.

Most Common Defective Return Mistakes in 2026

Based on practical experience, the following mistakes are increasingly common:

✔️ Filing ITR-1 despite having capital gains

✔️ Ignoring AIS information

✔️ Not reporting FD interest

✔️ Not reporting dividend income

✔️ Incorrect business income disclosures

✔️ Missing foreign asset information

✔️ Wrong selection of ITR form

✔️ Incomplete capital gains schedules

Can a Defective Return Notice Be Resolved?

Yes.

Most Section 139(9) notices can be resolved successfully if the defect is identified and corrected promptly.

The key is understanding the issue and taking timely action.

Frequently Asked Questions

Is a Section 139(9) Notice serious?

It should not be ignored. While it is generally a compliance-related notice, failure to respond can invalidate the return.

Does a defective return notice mean scrutiny assessment?

No.

A Section 139(9) Notice is different from a scrutiny notice under Section 143(2).

Can I get a refund if my return is defective?

The defect usually needs to be resolved before processing can continue.

Can I handle the notice myself?

Simple defects may be corrected independently. However, where capital gains, business income, foreign assets, or multiple issues are involved, professional guidance can be beneficial.

Why Taxpayers Should Seek Professional Help

Many taxpayers attempt to resolve defective return notices without understanding the underlying issue.

A wrong response can result in:

- Invalid return status

- Delayed refunds

- Additional notices

- Loss of tax benefits

Professional review can help identify the actual defect and ensure that the return is corrected properly.

Final Thoughts

A Section 139(9) Notice is one of the most common notices issued by the Income Tax Department. In most cases, it is not an allegation of tax evasion but an opportunity to correct errors in the return.

The sooner the defect is identified and corrected, the smoother the resolution process will be.

If you are unsure about the notice, seeking expert advice can help protect your refund, maintain compliance, and avoid unnecessary complications.

About the Author – Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Received a Section 139(9) Notice? Consult ITRAdvisor.in

If you have received a Section 139(9) Defective Return Notice, do not ignore it.

At ITRAdvisor.in, we regularly assist taxpayers with:

✔️ Defective Return Notices

✔️ AIS Mismatch Issues

✔️ Capital Gains Reporting

✔️ Wrong ITR Form Selection

✔️ Revised Returns

✔️ NRI Taxation

✔️ Income Tax Notices

✔️ Return Rectification and Compliance

Whether your notice relates to capital gains, business income, foreign assets, AIS mismatches, or an incorrect ITR form, our team can help you understand the issue and prepare an appropriate response.

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.