Section 143(1) Notice Received? Here’s What It Means and What You Should Do

8 June 2026•Dr. Haresh Adwan

A Section 143(1) Notice

Receiving an Income Tax Notice can be stressful, especially when you see “Section 143(1)” mentioned in the communication from the Income Tax Department. Many taxpayers panic, assuming they are under scrutiny or facing a tax investigation.

The good news is that a Section 143(1) Notice is usually not a tax raid, assessment, or investigation. In most cases, it is simply an intimation sent after the Income Tax Department processes your Income Tax Return (ITR).

In this article, we explain what a Section 143(1) Notice means, why you received it, and what actions you should take.

What is a Section 143(1) Notice?

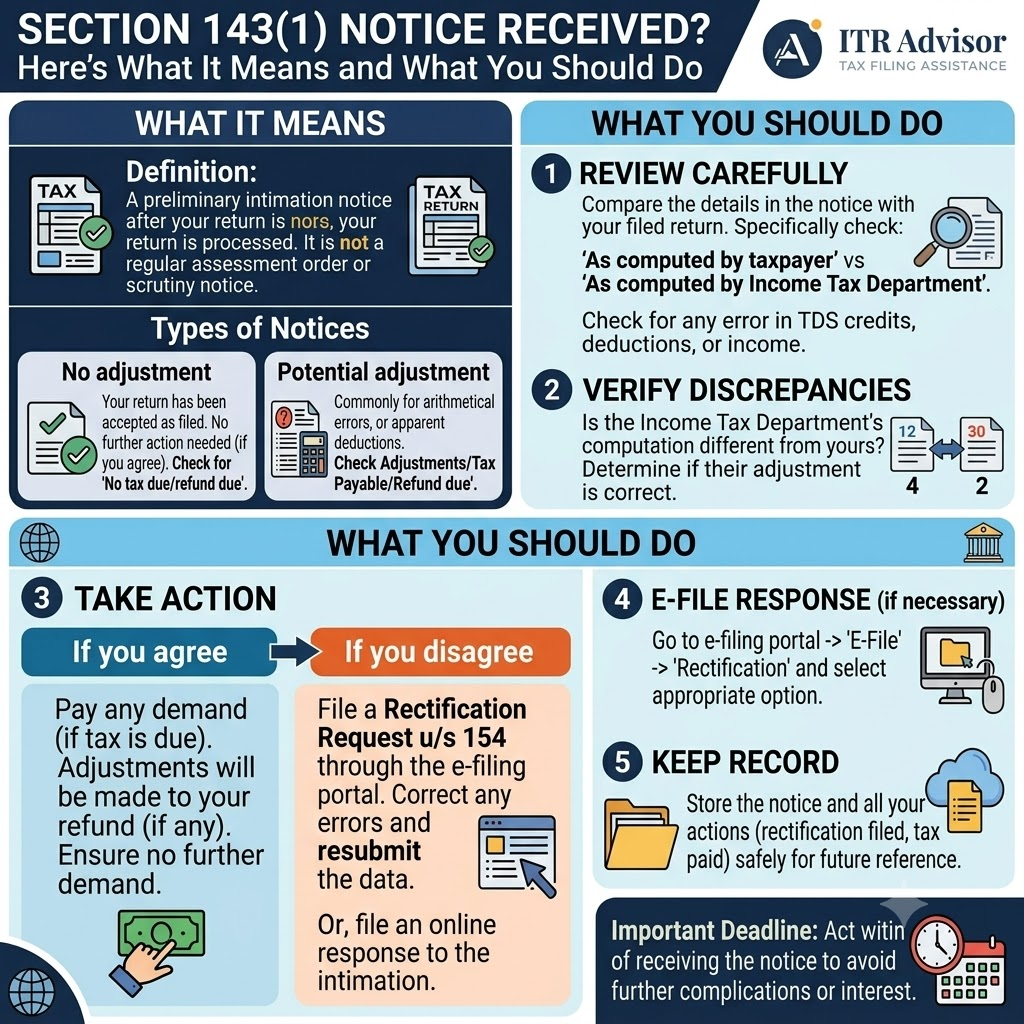

A Section 143(1) Notice, commonly known as an Intimation under Section 143(1), is issued after the Income Tax Department processes your Income Tax Return.

The department compares:

- Income reported in your ITR

- Information available in Form 26AS

- Annual Information Statement (AIS)

- Tax Deducted at Source (TDS) records

- Other financial information available with the department

After processing, the department may:

- Accept your return as filed

- Determine additional tax payable

- Grant a refund

- Adjust the refund against existing tax demand

The result is communicated through an Intimation under Section 143(1).

Is Section 143(1) Notice a Serious Notice?

In most cases, .

NO

A Section 143(1) Notice is generally a routine communication and does not necessarily indicate any wrongdoing.

However, taxpayers should carefully review the notice because it may contain:

- Tax demand

- Reduction in refund

- Disallowance of deductions

- Mismatch in income reporting

Ignoring the notice can create future complication

Why Did I Receive a Section 143(1) Notice?

Some common reasons include:

- Mismatch in TDS

The TDS claimed in your ITR may not match the TDS reported by deductors.

- Interest Income Not Reported

Banks report FD interest to the Income Tax Department.

If the interest reflected in AIS is not reported in the ITR, the department may make adjustments.

- Incorrect Deduction Claims

Deductions claimed under sections such as:

- 80C

- 80D

- 80G

may be disallowed if discrepancies are identified.

- Mathematical Errors

Simple calculation mistakes can also result in adjustments during processing.

- Income Mismatch with AIS

The department increasingly relies on AIS data.

Differences between AIS and the ITR can trigger adjustments under Section 143(1).

Types of Intimations Under Section 143(1)

Return Accepted

The department accepts the return without any changes.

No further action is generally required.

Refund Determined

The department confirms that a refund is due and initiates the refund process.

Tax Demand Raised

The department determines that additional tax is payable.

Taxpayers should verify the reasons before making payment.

How to Check Section 143(1) Notice Online

You can check the notice by logging into the Income Tax e-Filing Portal.

Steps:

- Login to your account.

- Go to “e-Proceedings” or “View Filed Returns.”

- Download the Intimation under Section 143(1).

- Review the comparison between the filed return and processed return.

What Should You Do After Receiving a Section 143(1) Notice?

Step 1: Read the Notice Carefully

Identify whether:

- No demand exists

- Refund is granted

- Additional tax demand is raised

Step 2: Compare with Your ITR

Review:

- Form 26AS

- AIS

- Form 16

- Bank interest records

- Capital gains statements

Step 3: Verify the Adjustment

Determine whether the department’s adjustment is correct.

Step 4: Respond Appropriately

If you agree with the demand:

- Pay the tax

- Update records

If you disagree:

- File a rectification request under Section 154 if applicable

- Seek professional advice

Can You Ignore a Section 143(1) Notice?

Ignoring the notice is not advisable.

Failure to address a valid demand may result in:

- Interest liability

- Future refund adjustments

- Recovery proceedings in certain cases

Always review and understand the notice before deciding on the next step.

Section 143(1) Notice vs Section 143(2) Notice

Many taxpayers confuse these notices.

Section 143(1)

- Automated processing

- Routine communication

- No detailed scrutiny

Section 143(2)

- Scrutiny assessment

- Detailed examination of income and deductions

- Additional documents may be requested

A Section 143(2) notice is generally more significant than a Section 143(1) intimation.

Also Read: Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Frequently Asked Questions (FAQs)

1.Is Section 143(1) Notice a scrutiny notice

No. It is generally an intimation issued after processing the return.

2.Can I receive a refund after a Section 143(1) Notice?

Yes. Many taxpayers receive refunds through the Section 143(1) intimation process.

3.What if the demand raised is incorrect?

You should review the notice and consider filing a rectification request if the adjustment is incorrect.

4.How long does it take to receive a Section 143(1) Intimation?

The timeline varies depending on return processing by the Income Tax Department.

Conclusion

Receiving a Section 143(1) Notice is common and should not automatically cause concern. However, taxpayers should carefully review the notice to ensure that income, deductions, TDS credits, and other information have been correctly considered.

If you have received a Section 143(1) Notice and are unsure how to interpret the tax demand, refund adjustment, or income mismatch, professional guidance can help avoid future disputes and unnecessary tax liabilities.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.