GST Composition Scheme 2026: The Complete Small Business Guide Eligibility, Rates, and Compliance

Dr. Haresh Adwani April 2026 10 min read

What Is the GST Composition Scheme?

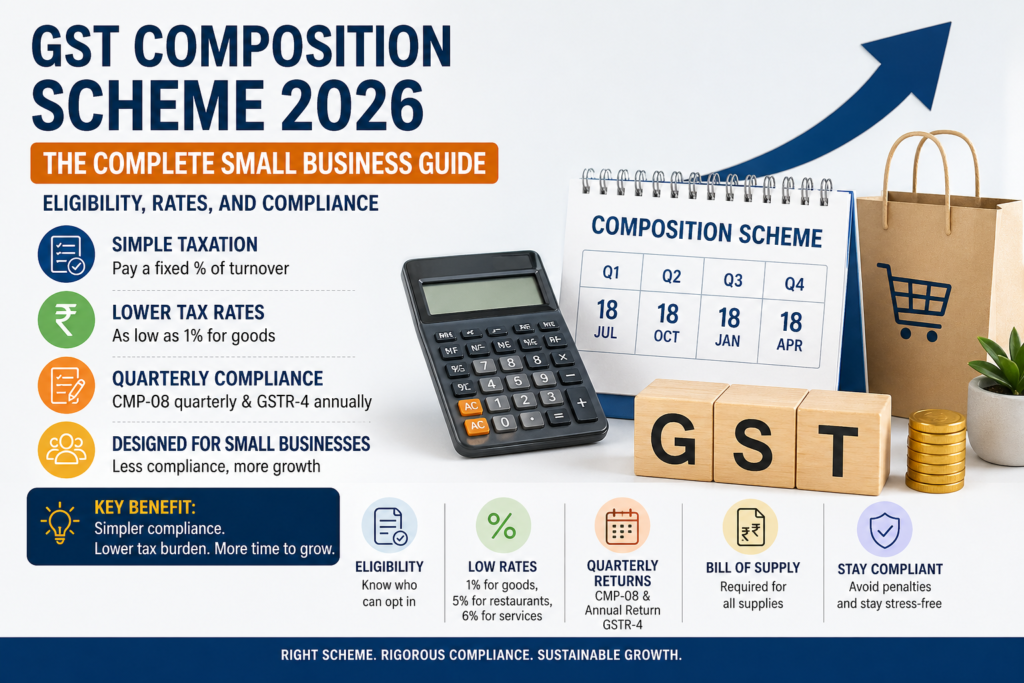

The GST Composition Scheme, governed by Section 10 of the Central Goods and Services Tax (CGST) Act 2017, is a simplified taxation option for small businesses. Instead of calculating GST on every individual invoice, tracking ITC, filing monthly returns, and reconciling supplier data, eligible businesses pay a single flat percentage of their total quarterly turnover as GST.

GST Composition Scheme Eligibility 2026: Who Can and Cannot Opt In

Turnover Thresholds (FY 2026-27)

| Business Category | Turnover Limit (All-India PAN) | Special Category States |

| Manufacturers and traders of goods | Rs. 1.5 crore | Rs. 75 lakh |

| Restaurants (not serving alcohol) | Rs. 1.5 crore | Rs. 75 lakh |

| Service providers | Rs. 50 lakh | Rs. 50 lakh |

Who Cannot Opt for the GST Composition Scheme (Statutory Exclusions)

- Manufacturers of ice cream, pan masala, aerated beverages, or tobacco and tobacco products.

- Businesses making inter-state outward supplies of goods (you may purchase from other states, but not sell).

- E-commerce operators required to collect Tax Collected at Source (TCS) under Section 52 of the CGST Act.

- Non-resident taxable persons and casual taxable persons.

- Businesses supplying goods through an e-commerce operator (sellers on Amazon, Flipkart, Meesho, etc.).

GST Rates Under the GST Composition Scheme 2026

| Business Type | Total GST Rate | CGST Component | SGST Component | Returns Required |

| Manufacturers of goods | 1% | 0.5% | 0.5% | CMP-08 + GSTR-4 |

| Traders and retailers of goods | 1% | 0.5% | 0.5% | CMP-08 + GSTR-4 |

| Restaurants (not serving alcohol) | 5% | 2.5% | 2.5% | CMP-08 + GSTR-4 |

| Service providers | 6% | 3% | 3% | CMP-08 + GSTR-4 |

Should Your Business Choose the GST Composition Scheme? A Decision Framework

Choose the GST Composition Scheme If…

- All or most of your customers are end consumers (B2C) who do not need GST tax invoices to claim ITC.

- Your business is localised you do not supply goods to customers in other states.

- Input costs are low relative to sales you would not benefit significantly from ITC claims.

- You want to reduce monthly compliance costs and professional fees.

- Your turnover is comfortably below the threshold with no expectation of crossing it mid-year.

Do NOT Choose the GST Composition Scheme If...

- You sell primarily to other GST registered businesses (B2B) composition dealer status prevents buyers from claiming ITC, making you commercially less competitive.

- You have high input purchases where ITC claims would significantly reduce your net tax burden.

- You sell goods to buyers in other states inter-state outward supply disqualifies you entirely.

- Your turnover is close to the threshold and growing mid-year disqualification creates significant compliance complications.

- You sell goods through e-commerce platforms such as Flipkart, Amazon, or Meesho.

Also Read:

https://itradvisor.in/blog/gst-compliance-checklist-india-2026

GST Compliance Requirements Under the Composition Scheme

CMP-08: Quarterly Statement-Cum-Challan

| Quarter | Period | CMP-08 Due Date |

| Q1 | April to June | 18th July |

| Q2 | July to September | 18th October |

| Q3 | October to December | 18th January |

| Q4 | January to March | 18th April |

Late payment penalty: Interest at 18% per annum from due date + late filing fee of Rs. 50 per day (Rs. 25 CGST + Rs. 25 SGST), subject to a maximum of Rs. 2,000 per return.

GSTR-4: Annual Return

GSTR4 is the annual return consolidating all CMP-08 filings. Due date: 30th April of the following financial year. For FY 2025-26, the due date is 30 April 2026. Late fee: Rs. 200 per day (Rs. 100 CGST + Rs. 100 SGST), maximum Rs. 5,000. The GST portal auto-populates CMP-08 data, making this return straightforward.

Bill of Supply: The Mandatory Billing Document

Composition dealers cannot issue a GST tax invoice. Every sale must be recorded on a Bill of Supply that prominently displays: “Composition Taxable Person, not eligible to collect tax on supplies.” Issuing a regular tax invoice or showing GST as a separate charge on the bill is a direct violation of Section 10(4) of the CGST Act and attracts penalty proceedings.

How to Opt Into the Composition Scheme for FY 2026-27

- Log in to www.gst.gov.in using your GSTIN credentials.

- Navigate to: Services → Registration → Application to Opt for Composition Levy.

- File Form GST CMP 02 and select your business category.

- Accept the eligibility declaration and submit using DSC (companies/LLPs) or EVC/OTP (proprietors/partnerships).

- Within 60 days of opting in, file Form ITC-03 to reverse any ITC balance held under the regular scheme.

The 5 Costliest Composition Scheme Compliance Mistakes

Mistake 1: Not Tracking Aggregate Turnover Across All GST Registrations

The Rs. 1.5 crore (or Rs. 50 lakh for services) threshold applies to combined turnover under your PAN not per GSTIN. Business owners with multiple businesses frequently discover they are ineligible only after an audit. Implement a monthly consolidated turnover tracking system.

Mistake 2: Collecting GST Separately From Customers

Composition dealers bear the GST from their own margin it cannot be charged separately to customers. Collecting GST on composition dealer bills violates Section 10(4), exposes you to penalty proceedings, and means buyers cannot claim ITC on those amounts.

Mistake 3: Missing Reverse Charge Mechanism (RCM) Obligations

Even though composition dealers cannot claim ITC, they remain liable for GST under the Reverse Charge Mechanism on specified inward supplies such as services from unregistered vendors or notified categories. RCM tax must be paid in cash at regular GST rates and declared in CMP 08.

Mistake 4: Missing the CMP 08 Deadline

Interest at 18% per annum starts accumulating the day after the due date. Beyond the financial cost, repeated late filings are a compliance risk signal that increases the probability of audit selection.

Mistake 5: Continuing in the Scheme After Crossing the Turnover Limit

If your aggregate turnover crosses Rs. 1.5 crore (or Rs. 50 lakh for services) and you do not switch to the regular scheme within 7 days by filing Form CMP 04, every invoice issued after the threshold date is treated as irregular. GST demand, interest at 18% p.a., and penalty on the entire excess period turnover applies. This is the single most consequential composition scheme mistake.

Frequently Asked Questions

Q1. When must a business switch from the Composition Scheme to regular GST?

Immediately when aggregate annual turnover crosses Rs. 1.5 crore (Rs. 50 lakh for services) during the financial year, or when the business begins making inter-state outward supplies of goods. File Form CMP04 within 7 days of crossing the threshold.

Q2. Can a composition dealer issue an e-invoice?

No. Composition dealers issue Bills of Supply not tax invoices or e invoices. There is no GST to report to the Invoice Registration Portal (IRP) because composition dealers do not collect GST from customers.

Q3. Is GST payable under the Reverse Charge Mechanism for composition taxpayers?

Yes. RCM obligations apply to composition taxpayers on specified inward supplies. This tax must be paid in cash at regular GST rates and declared in CMP08. ITC cannot be claimed against this RCM liability.

Q4. Is the composition scheme beneficial for service based businesses?

It depends on the profile. If your service business is B2C (retail clients who do not need ITC), has annual turnover comfortably below Rs. 50 lakh, and carries low input costs, the composition scheme reduces compliance burden significantly. If you serve businesses that need to claim ITC on your invoices, the regular scheme is commercially necessary.

Conclusion:

The GST Composition Scheme is a powerful compliance simplification tool for eligible small businesses but only if chosen correctly and administered rigorously. The five mistakes outlined in this guide can collectively result in demands, penalties, and forced switch to the regular scheme under adverse conditions.

Adwani & Company assists small businesses in evaluating scheme eligibility, filing CMP02, managing CMP08 and GSTR4 filings, and switching to the regular scheme when necessary. Visit www.itradvisor.in for a consultation.

About the Author

Dr. Haresh Adwani | Founder, Adwani & Company Ph.D. in Commerce | 20+ years in Tax, FEMA & Financial Advisory Expert in: GST advisory · Income tax litigation · FEMA compliance · NRI taxation · F&O taxation · Corporate structuring .

Website: www.itradvisor.in

For consultations, schedule via the website.