Late Filing Penalty for AY 2026-27 : Fees, Interest & Consequences

Every year, lakhs of Indian taxpayers scramble to file their Income Tax Returns just before the deadline. Some miss it. And that’s when things get complicated.

Missing the ITR filing deadline for AY 2026-27 isn’t just an administrative lapse it has real financial consequences. From a late filing fee under Section 234F to interest under Section 234A, the cost of delay adds up quickly. There’s also the risk of income tax notices, loss of refunds, and the permanent loss of certain tax benefits.

Whether you’re a salaried employee, freelancer, business owner, or NRI, this guide covers everything you need to know about the late filing penalty for AY 2026-27.

What Is the ITR Filing Due Date for AY 2026-27?

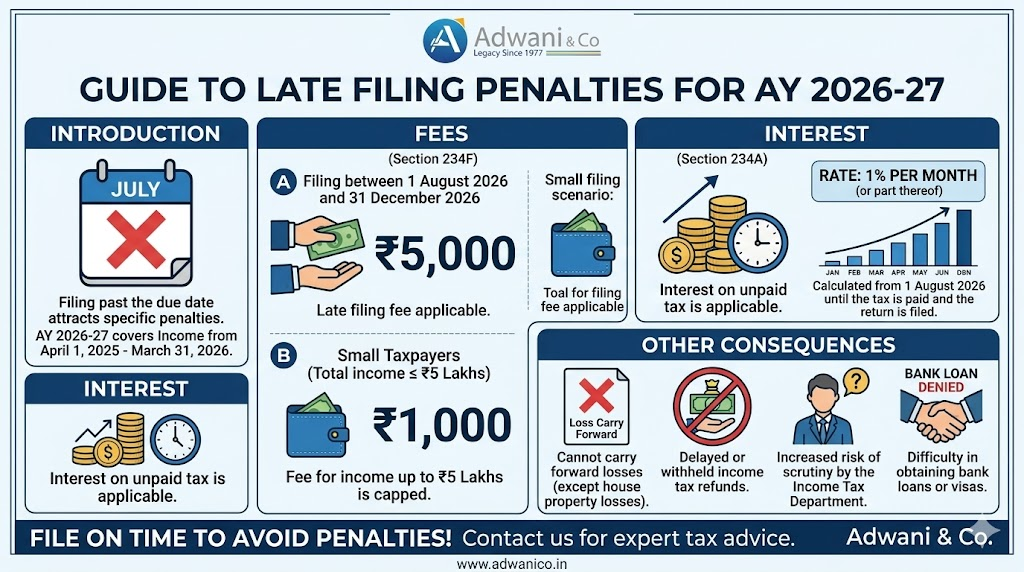

The Assessment Year (AY) 2026-27 corresponds to income earned during the Financial Year (FY) 2025-26 from 1 April 2025 to 31 March 2026.

For most individual taxpayers including salaried employees, freelancers, and small businesses not subject to tax audit the standard due date for filing an ITR is 31 July of the assessment year.

So for AY 2026-27, the general due date is 31 July 2026.

| Taxpayer Category | ITR Filing Due Date (AY 2026-27) |

| Salaried Individuals & HUFs (no audit) | 31 July 2026 |

| Businesses requiring tax audit (Section 44AB) | 31 October 2026 |

| Companies requiring audit | 31 October 2026 |

| Transfer pricing cases (Section 92E) | 30 November 2026 |

| Revised Return | 31 December 2026 |

| Belated / Late Return (Section 139(4)) | 31 December 2026 |

Important: Due dates are subject to CBDT notifications and extensions. Always verify the latest notification on the Income Tax India portal or ITRAdvisor.in before filing.

What Is Section 234F? Late Filing Fee Explained

Section 234F was inserted into the Income Tax Act, 1961, with effect from AY 2018-19. It introduced a mandatory late filing fee for taxpayers who miss the due date but still want to file a belated return.

Before Section 234F, there was no direct fee for late filing only interest. The section was introduced to encourage timely compliance.

Section 234F Late Filing Fee Structure for AY 2026-27

| Filing Date | Total Income Above Rs. 5 Lakh | Total Income Up to Rs. 5 Lakh |

| On or before 31 July 2026 (due date) | NIL | NIL |

| After 31 July 2026 up to 31 Dec 2026 | Rs. 5,000 | Rs. 1,000 |

| After 31 December 2026 (if extended) | Rs. 5,000 | Rs. 1,000 |

Key Point: Even if your tax liability is zero or you are eligible for a full refund, the late filing fee under Section 234F still applies unless your total income is below the basic exemption limit (i.e., below Rs. 3 lakh under the new regime for FY 2025-26).

Who Is Exempt from Section 234F Late Filing Fee?

- Individuals whose total income is below the basic exemption limit

- Individuals not required to file ITR under the law (though voluntary filing is advisable)

- Returns filed within the prescribed due date

Section 234A : Interest on Late Filing When Tax Is Due

Section 234F is a fee. But if you also have unpaid tax liability at the time of filing, you will additionally be charged interest under Section 234A of the Income Tax Act.

How Is Section 234A Interest Calculated?

- Rate: 1% simple interest per month or part of a month

- Calculated on the outstanding tax payable (i.e., tax due minus TDS, advance tax, and self-assessment tax paid)

- Period: From the day after the due date till the date of actual filing or payment

Example: If you file your ITR on 30 September 2026 (due date 31 July 2026) with Rs. 50,000 outstanding tax, you will pay 2 months of 234A interest = Rs. 1,000. Plus Rs. 5,000 under Section 234F. Total additional outgo: Rs. 6,000.

Section 234B and 234C: Additional Interest Traps

If you are required to pay advance tax but haven’t paid it correctly, you may also face:

- Section 234B –:Interest for default in payment of advance tax (if advance tax paid is less than 90% of the total tax liability)

- Section 234C Interest for deferment of advance tax instalments

| Section | Nature of Default | Interest Rate | Calculation Period |

| 234A | Late ITR filing with outstanding tax | 1% per month | Due date to actual filing date |

| 234B | Advance tax less than 90% of tax due | 1% per month | 1 April to date of filing |

| 234C | Underestimated advance tax instalments | 1% per month | Per each instalment default |

Beyond Penalty: Other Consequences of Late ITR Filing

1. Loss of Carry Forward of Losses

2. Delay in Income Tax Refund

3. Inability to Revise the Return

4. Difficulty in Loan Approvals and Visa Applications

5. Income Tax Notices for Non-Filing

What Is a Belated Return? Can You Still File After the Deadline?

Yes. If you miss the 31 July 2026 due date, you can still file a belated return under Section 139(4) of the Income Tax Act, 1961 up to 31 December 2026.

A belated return carries the Section 234F fee and applicable interest. However, it is far better to file a belated return than not to file at all.

What You Can and Cannot Do in a Belated Return

| Feature | Original Return (by 31 Jul 2026) | Belated Return (by 31 Dec 2026) |

| Filing allowed | Yes | Yes |

| Late filing fee (Section 234F) | Nil | Rs. 1,000 or Rs. 5,000 |

| Carry forward of capital/business losses | Allowed | NOT Allowed |

| Claim deductions u/s 80C, 80D, etc. | Allowed | Allowed |

| Revision of return u/s 139(5) | Allowed (up to 31 Dec 2026) | Allowed (up to 31 Dec 2026) |

| Refund claim | Allowed | Allowed (but may be delayed) |

Practical Examples: How the Penalty Adds Up

Example 1 : Salaried Employee, No Outstanding Tax

Rajan is a salaried employee with total income of Rs. 8 lakh. His full tax has been deducted at source by his employer. He forgets to file his ITR and files it on 15 September 2026.

- Section 234F fee: Rs. 5,000 (income above Rs. 5 lakh, filed after 31 July 2026)

- Section 234A interest: Nil (no outstanding tax payable)

- Total additional payment: Rs. 5,000

Example 2 : Freelancer with Outstanding Tax

Priya is a freelancer with total income of Rs. 12 lakh and advance tax of Rs. 40,000 paid. Total tax liability is Rs. 1,20,000. She files her return on 1 October 2026.

- Outstanding tax = Rs. 80,000

- Section 234F fee = Rs. 5,000

- Section 234A interest = 2 months x 1% x Rs. 80,000 = Rs. 1,600

- Total additional payment = Rs. 6,600

- Plus: she cannot carry forward any capital losses (if applicable)

Example 3 – Low Income Taxpayer

Sunita is a retired individual with pension income of Rs. 4.5 lakh. She files her return on 20 August 2026.

- Section 234F fee: Rs. 1,000 (income below Rs. 5 lakh)

- Section 234A interest: Nil (no outstanding tax after standard deduction)

- Total additional payment: Rs. 1,000

Common Mistakes That Lead to Late Filing

- Waiting for Form 16 to arrive before starting the process

- Assuming no tax liability means no need to file

- Not reconciling AIS and Form 26AS before filing, causing last-minute corrections

- Forgetting to include income from fixed deposits, rental income, or freelance work

- NRIs not tracking their Indian income sources properly

- Not updating bank account details, causing failure to receive refunds even after filing

- Misunderstanding the ITR form applicable to their income type (ITR1 vs ITR2 vs ITR4)

- Also Read : ITR 1 vs ITR 2 vs ITR 3 vs ITR 4: The Definitive Guide to Picking the Right Income Tax Return Form for AY 2026-27

How to Avoid Late Filing Penalties: A Practical Checklist

- Collect all income documents : Form 16, Form 16A, rental agreements, freelance invoices

- Download and reconcile your AIS (Annual Information Statement) from the Income Tax Portal

- Verify TDS credit in Form 26AS matches your actual tax deductions

- Calculate advance tax liability if you have income beyond salary (freelance, rent, capital gains)

- Identify the correct ITR form for your income type

- File on or before 31 July 2026 to avoid Section 234F fee

- If you discover any errors post-filing, file a revised return by 31 December 2026

- If you have capital losses or business losses, timely filing is non-negotiable

NRI Taxpayers: Special Note on Late Filing

Non-Resident Indians (NRIs) with income arising in India rent, capital gains from sale of property or securities, interest from NRO accounts are also required to file ITR if their Indian income exceeds the basic exemption limit.

For NRIs, the same Section 234F fee applies if the return is filed late. Additionally, NRIs dealing with property transactions often receive TDS at higher rates (such as 20%+ on LTCG). If they fail to file returns, excess TDS deducted cannot be claimed as refund.

If you are an NRI who sold property in India in FY 2025-26, filing your ITR on time is critical to reclaiming excess TDS. A late return not only delays the refund but also attracts Section 234F fee.

NRIs should also be aware of the 120day rule those who visit India for 120 days or more and whose Indian income exceeds Rs. 15 lakh may be classified as Resident but Not Ordinarily Resident (RNOR), which has separate filing obligations.

Read our Guide on The 120-Day Rule That Is Silently Taxing Thousands of NRIs in India :Are You at Risk?https://itradvisor.in/blog/the-120-day-rule-silently-taxing-nris

Key Takeaways

- File your ITR for AY 2026-27 by 31 July 2026 to avoid late filing fee under Section 234F

- Late filing fee is Rs. 5,000 for income above Rs. 5 lakh and Rs. 1,000 for income up to Rs. 5 lakh

- Section 234A interest applies at 1% per month on unpaid taxes from the due date to the filing date

- Capital losses and business losses cannot be carried forward if the return is filed late

- Belated returns (up to 31 December 2026) are better than no return at all

- NRIs must also file returns on time to avoid penalties and claim excess TDS refunds

- Even nil-tax returns should be filed on time for compliance, refund claims, and loan documentation

Frequently Asked Questions (FAQs)

Q1. What is the last date to file ITR for AY 2026-27?

The last date for filing the original ITR for most individuals (salaried, freelancers, non-audit cases) is 31 July 2026. For belated returns, the deadline is 31 December 2026. Dates may be extended by CBDT via official notification.

Q2. Is Section 234F applicable if there is no tax liability?

Yes. Section 234F applies based on whether the return is filed after the due date it is not linked to tax liability. However, if your total income is below the basic exemption limit no fee applies.

Q3. Can I carry forward capital losses if I file the return late?

No. If you file your return after the due date, capital losses (both STCG and LTCG losses) and business losses cannot be carried forward to future years. This is one of the most significant financial consequences of late filing.

Q4. Is there any penalty for non-filing of ITR (not even a belated return)?

Yes. Under Section 276CC of the Income Tax Act, willful failure to file an ITR is a criminal offence result ing in imprisonment ranging from 3 months to 2 years, with possible extension to 7 years in cases of significant tax evasion. Additionally, the Assessing Officer can also impose a penalty, which can result in a higher tax demand.

Q5. Can I file an ITR after 31 December 2026?

After 31 December 2026, the window for filing a belated return for AY 2026-27 generally closes. However, in certain circumstances may be required or permitted to file a late return. For updating income post-assessment, you may use an Updated Return within two years from the end of the relevant assessment year.

Conclusion: File On Time — There Is No Good Reason to Delay

The late filing penalty for AY 2026-27 is not just about the Rs. 5,000 fee. It’s about losing carry-forward benefits that could save you thousands of rupees in future taxes. It’s about delayed refunds that you are rightfully entitled to. It’s about the risk of notices that create unnecessary stress and professional fees.

The income tax system in India is increasingly data-driven. With AIS capturing your bank transactions, mutual fund purchases, property deals, and more — there is very little that the Income Tax Department does not know. Filing your return accurately and on time is no longer just an option. It’s the only sensible financial decision.

If you are unsure about which ITR form to use, how to reconcile your AIS, or whether you have any outstanding tax liability — seek professional guidance well before 31 July 2026. The cost of advice is always less than the cost of a penalty.

Timely ITR filing = Avoided penalties + Protected benefits + Peace of mind.

Conclusion: File On Time

The late filing penalty for AY 2026-27 is not just about the Rs. 5,000 fee. It’s about losing carry-forward benefits that could save you thousands of rupees in future taxes. It’s about delayed refunds that you are rightfully entitled to. It’s about the risk of notices that create unnecessary stress and professional fees.

The income tax system in India is increasingly data driven. With AIS capturing your bank transactions, mutual fund purchases, property deals, and more there is very little that the Income Tax Department does not know. Filing your return accurately and on time is no longer just an option. It’s the only sensible financial decision.

ITR filing = Avoided penalties + Protected benefits + Peace of mind.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.