Self-Invoice for RCM: The GST Step Too Many Businesses Skip

Self-Invoice for RCM

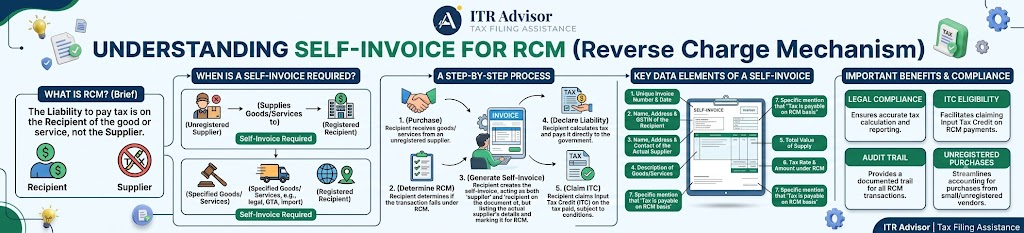

You paid GST under Reverse Charge Mechanism (RCM) on time. Good. But did you also issue a self-invoice for that RCM transaction? If not, your ITC claim and your audit file may already be at risk.

Many businesses treat RCM as a payment obligation and stop there. In reality, a self-invoice for RCM is a separate, mandatory document and skipping it is one of the most common GST compliance gaps we see at ITRAdvisor.in.

What Is a Self-Invoice for RCM?

Under Section 31(3)(f) of the CGST Act, when a registered person receives taxable goods or services from an unregistered supplier and is liable to pay GST under RCM, the recipient not the supplier must issue the invoice. This is the self-invoice for RCM. It exists because an unregistered supplier cannot legally issue a GST-compliant tax invoice, so the law shifts that responsibility to you.

Why the Self-Invoice for RCM Actually Matters

- It supports the GST you paid in cash under RCM.

- Without it, you cannot claim ITC on that RCM payment under Rule 36(1)(b).

- It strengthens your documentation trail during GST audits and scrutiny.

- It closes a gap officers routinely check, since RCM leaves no supplier-side trail.

The 30-Day Deadline Most Businesses Miss

Since Rule 47A took effect on 1st November 2024, a self-invoice for RCM must be issued within 30 days of receiving the goods or services not at month-end, and not whenever convenient. Miss this window and you risk interest on delayed tax and penalty exposure under Section 122, on top of ITC disputes.

The self-invoice must also be reported in Table 13 of GSTR-1, paired with a payment voucher under Section 31(3)(g) when payment is actually made to the unregistered supplier.

Common Self-Invoicing Mistakes Under RCM

- Paying RCM tax correctly but never generating the self-invoice.

- Issuing it weeks late, well outside the 30-day window.

- Not labelling it clearly as a self-billed invoice.

Forgetting the accompanying payment voucher.

Key Takeaways

- A self-invoice for RCM is mandatory under Section 31(3)(f) whenever you buy from an unregistered supplier under reverse charge.

- You must issue it within 30 days of receipt, under Rule 47A.

- No self-invoice generally means no valid ITC claim on that RCM payment.

Read our detailed guide on GST Compliance Checklist India 2026: 7 Essential Rules to Avoid Notices and Penalties

Frequently Asked Questions on Self-Invoice for RCM

1. Is a self-invoice for RCM always required?

Yes, whenever you’re liable to pay GST under RCM on a supply from an unregistered supplier.

2. What happens if I don’t issue a self-invoice for RCM?

You may lose your ITC claim on that RCM payment and face questions during a GST audit.

3. What is the deadline to issue a self-invoice under RCM?

Within 30 days of receipt, as mandated by Rule 47A effective 1st November 2024.

4. Is a payment voucher the same as a self-invoice?

No. The self-invoice records the supply; the payment voucher separately records the payment.

Conclusion: Don’t Let Paperwork Undo Correct Tax Payment

Paying GST under RCM is only half the compliance story. Issuing a proper, timely self-invoice for RCM is what protects your ITC, your audit trail, and your peace of mind. As Dr. Haresh Adwani, founding expert at Adwani & Co LLP, often points out, GST compliance is not just about depositing tax it is about proving that tax was correctly deposited, with the right document, at the right time.

Learn more about our GST Compliance Checklist 2026, or read our detailed guide on GST Input Tax Credit Rules 2026.

For the official framework, refer to the GST Portal and the Central Board of Indirect Taxes and Customs for the latest notifications on invoicing and reverse charge.

About the Author – Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.