Thousands of NRIs pay more tax than they legally need to, and most don’t find out until a refund gets stuck, a notice lands, or a property sale turns complicated. If you live abroad but still earn even a rupee of income in India, NRI ITR filing isn’t a formality you can skip. It’s the one step that decides whether you overpay the taxman or claim back what’s rightfully yours.

Do NRIs Really Need NRI ITR Filing While Living Abroad?

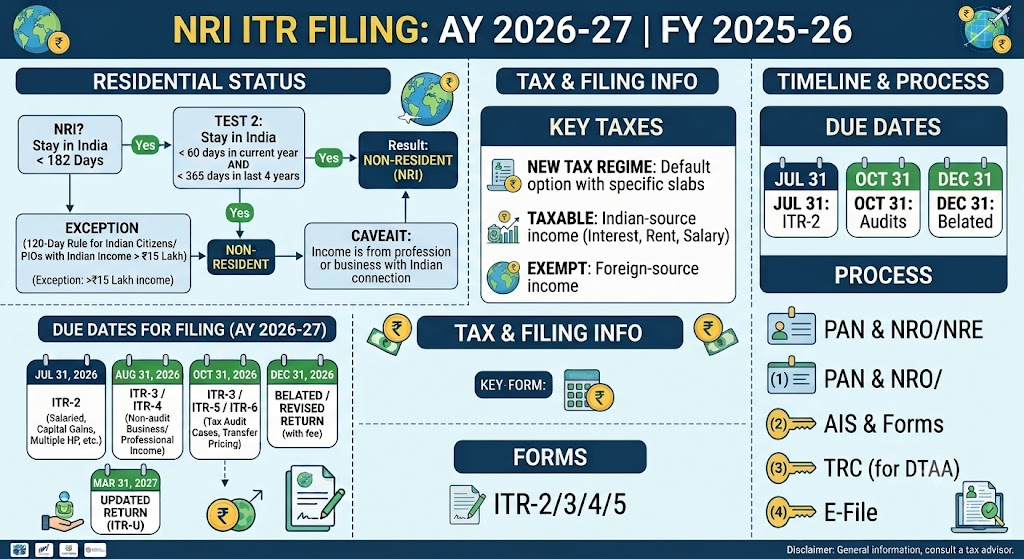

This is the single biggest myth in NRI taxation. Living outside India does not exempt you from Indian tax law the moment income actually arises here. NRI ITR filing becomes mandatory whenever you have rental income from an Indian property, capital gains, or interest income, regardless of how small the amount seems. And here’s the part most NRIs miss: TDS being deducted at source does not close the matter. If the flat TDS rate is higher than your actual tax liability, skipping NRI ITR filing means walking away from a refund you’re legally entitled to.

The NRI ITR Filing Questions We Hear Every Season

Every filing season, the questions from NRI clients follow a familiar pattern:

Do I need to file an ITR if I only earn rental income from India?

TDS has already been deducted on my income. Do I still need to file a return?

I sold a property in India. Can I claim a refund of excess TDS?

My NRO account earned interest. Is it taxable?

I transferred money between my NRE and NRO accounts. Is there any tax implication?

Can I claim deductions under Section 80C or 80D as an NRI?

What documents do I need to keep ready before filing?

Will NRI ITR filing help me in future property transactions, loans, or repatriation of funds?

Each of these has a concrete, individual answer, and getting it wrong is exactly what leads to overpaid tax or a delayed refund.

NRI ITR Filing After a Property Sale: Claiming Your TDS Refund

When an NRI sells property in India, the buyer typically deducts TDS at a much higher rate than the actual capital gains tax owed. Without NRI ITR filing, that excess amount simply sits with the government. Filing a return lets you compute the real capital gains, apply eligible exemptions, and claim back the difference as a refund, often a meaningful sum on a mid-sized property transaction.

NRO Interest, NRE-NRO Transfers, and NRI ITR Filing

Interest earned on an NRO account is fully taxable in India and usually carries TDS close to 30%. NRE account interest, by contrast, is exempt for a genuine non-resident. A common point of confusion is transferring funds between your own NRE and NRO accounts. This movement, by itself, is not a fresh taxable event, but it should be documented carefully since it can surface during AIS or Form 26AS reconciliation, and accurate NRI ITR filing keeps that record clean and defensible.

Deductions and Documents for Smooth NRI ITR Filing

NRIs remain eligible for several deductions under the Income Tax Act, including Section 80C (life insurance, ELSS, children’s tuition fees) and Section 80D (health insurance premiums), subject to certain conditions. Before NRI ITR filing, keep the following ready: PAN, passport copy confirming residential status, NRE and NRO bank statements, Form 26AS and AIS, TDS certificates, and the sale deed if a property transaction is involved. Proper NRI ITR filing today also strengthens your position for future loans, property purchases, and smooth repatriation of funds through proper banking channels.

Key Takeaway

• NRI ITR filing is mandatory once taxable Indian income exists, TDS deduction alone does not end the obligation.

• Property sales, NRO interest, and rental income are the most common triggers for NRI ITR filing.

• Timely NRI ITR filing is the only route to recovering excess TDS as a refund. • Good documentation today prevents AIS/Form 26AS mismatch notices tomorrow.

For nearly five decades, Adwani & Co LLP has guided NRI clients through exactly these questions, under the stewardship of Dr. Haresh Adwani, who holds a PhD in Commerce and is also a law graduate. That depth of experience is precisely why a few weeks of planning ahead of the filing season routinely saves NRIs from unnecessary tax outflow and months of avoidable follow-up with the Income Tax Department.

Frequently Asked Questions

1.Can I claim a TDS refund through NRI ITR filing after selling property?

Yes. If TDS deducted exceeds your actual capital gains tax, NRI ITR filing is how you claim that excess amount back.

2.Is interest on an NRO account taxable for NRIs?

Yes, NRO interest is fully taxable in India, unlike NRE account interest, which is generally exempt.

3.Do NRE to NRO fund transfers attract tax?

Not by themselves, but they should be documented properly to avoid mismatches during NRI ITR filing and AIS reconciliation.

4.Can NRIs claim deductions under Section 80C and 80D?

Yes, subject to certain conditions, making accurate NRI ITR filing essential to actually claim

Conclusion: Make NRI ITR Filing Work in Your Favour

NRI ITR filing isn’t just about compliance, it’s about not leaving your own money on the table. Rental income, property sales, NRO interest, and fund transfers all carry tax implications that only proper filing can resolve in your favour. If you’re an NRI with income, investments, or property in India, review your tax position before the filing rush begins.

Dr. Haresh Adwani is a PhD holder in Commerce with over 20 years of experience in NRI taxation, FEMA compliance, international financial advisory, and tax notice resolution. He is one of Pune’s most trusted NRI tax advisors, specialising in residential status assessment, DTAA planning, and cross-border compliance for professionals returning from the US, UK, UAE, Canada, and Australia.

Disclaimer:

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

If you want expert guidance on NRI ITR filing, connect with itradvisor.in today, and take the guesswork out of your Indian tax compliance.

You donated money to a political party, claimed the Section 80GGC deduction in your Income Tax Return, and thought that was the end of it. Then one morning, a message from the Income Tax Department lands in your inbox your deduction has been flagged for scrutiny, and you are now asked to justify a claim worth lakhs of rupees. If this sounds alarming, it should. And it is happening to thousands of Indian taxpayers right now.

The Income Tax Department has significantly intensified scrutiny of Section 80GGC deductions in recent assessment cycles. Salaried professionals, business owners, and HUFs who claimed political donation deductions are receiving SMS alerts, scrutiny notices, and in some cases, full disallowance of their claims — with penalties that can reach 200% of the tax evaded. Yet, Section 80GGC is a completely legitimate, government-sanctioned provision that rewards transparent political funding with meaningful tax benefits.

The problem is not the section itself. The problem is how — and whether it has been used correctly. In this comprehensive guide, the expert team at Adwani and Company walks you through everything: what Section 80GGC actually allows, who qualifies, what conditions must be met, why deductions get disallowed, how to protect your claim, and what to do if you have already received a notice under this provision.

Whether you are filing your ITR 2026 for the first time with a political donation or are already facing scrutiny for a past claim, this is the guide you need to read fully, carefully, and right now.

What Is Section 80GGC? The Income Tax Deduction on Political Donations Explained Clearly

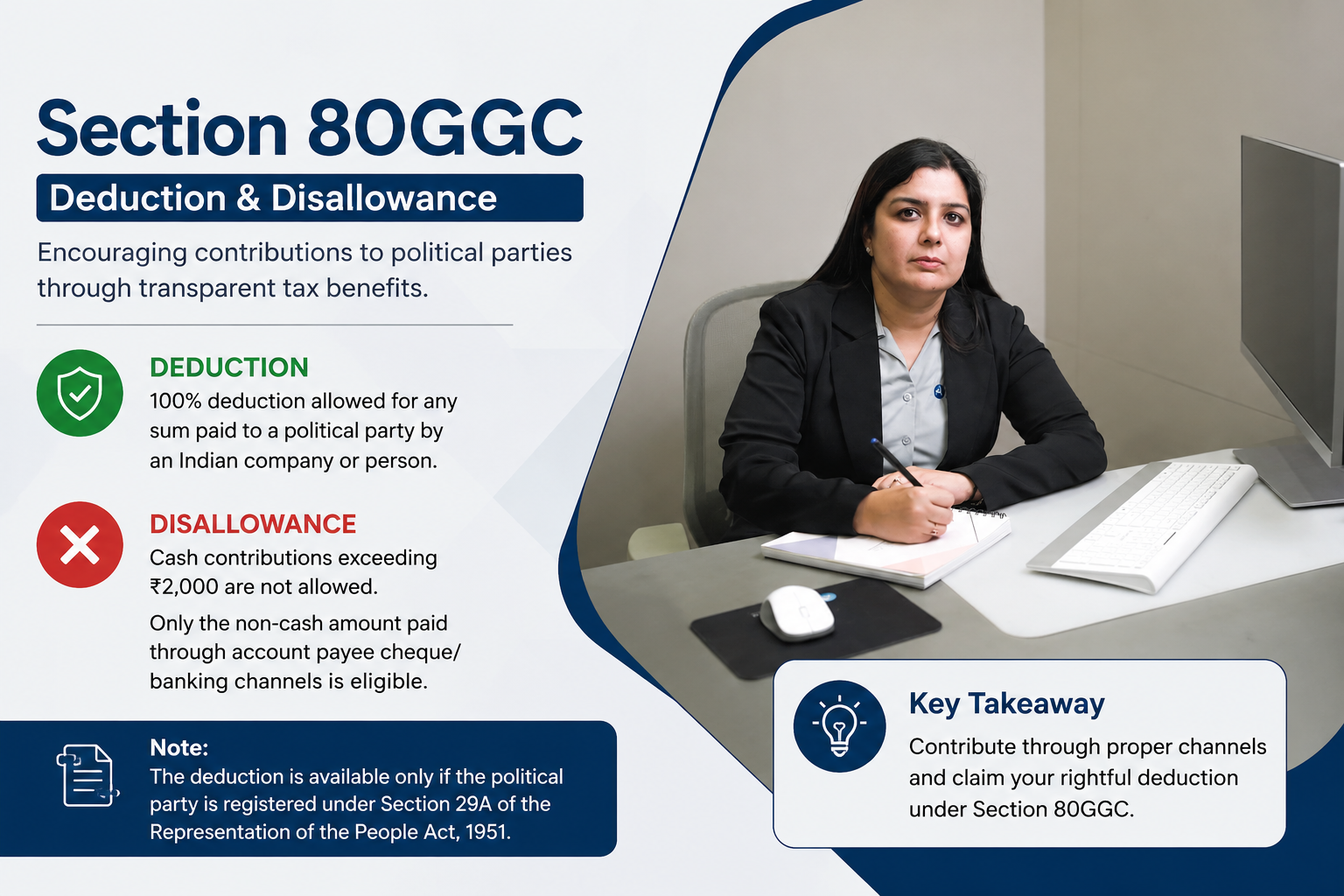

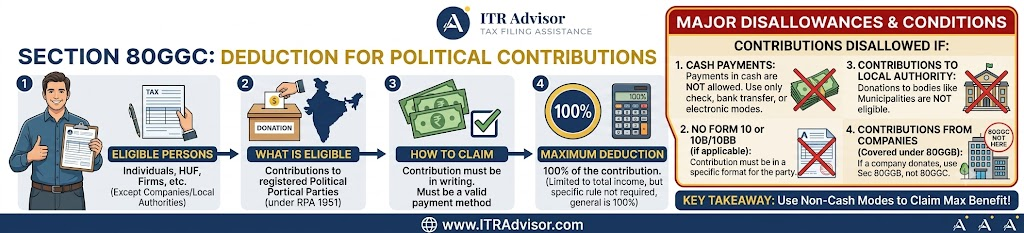

Section 80GGC of the Income Tax Act, 1961 now also reflected in the newly enacted Income Tax Act 2025 is a provision under Chapter VI-A that allows eligible taxpayers to claim a deduction for contributions made to registered political parties or approved electoral trusts. The deduction covers 100% of the amount donated, making it one of the most generous deductions available to individuals under Indian tax law.

The purpose of this section is rooted in democratic policy: to encourage transparent, traceable, and formally documented political funding. By providing a tax incentive for political contributions, the government aims to reduce unaccounted cash flowing into political campaigns and push donors toward legitimate, banking-channel-based contributions.

However, the very generosity of this deduction 100% of the donated amount with no fixed upper cap in rupee terms has made it a target for misuse, which is precisely why the Income Tax Department’s scrutiny of Section 80GGC claims has intensified dramatically in 2025 and 2026.

Section 80GGC vs. Section 80GGB : Key Differences You Must Know

Feature

Section 80GGB

Section 80GGC

Who can claim

Indian companies only

Individuals, HUFs, Firms, AOPs — NOT companies

Deduction limit

100% of donation

100% of donation (max = total taxable income)

Cash donations allowed?

No

No — banking channels mandatory

Tax regime

Old regime only

Old regime only

Mode of payment

Cheque, DD, banking channels

Cheque, DD, UPI, net banking, cards

As Dr. Haresh Adwani, Managing Partner at Adwani and Company, explains to clients: “Many taxpayers confuse 80GGC with 80GGB or assume companies can use this provision. They cannot. Section 80GGC is exclusively for non-corporate assessees. Allowing a company to claim under 80GGC is an error that will invite immediate disallowance.”

Who Is Eligible to Claim Section 80GGC Deduction? Eligibility Criteria for 2026

Before claiming this deduction in your ITR, verify that you meet each of the following conditions without exception:

Eligible Assessees Under Section 80GGC

Individual taxpayers : salaried, self-employed, professional, or retired

Hindu Undivided Families (HUFs)

Firms : partnership firms and LLPs

Association of Persons (AOP) and Body of Individuals (BOI)

Artificial juridical persons NOT wholly or partly funded by the government

Who is explicitly NOT eligible:

Indian companies they must claim under Section 80GGB instead

Local authorities and government-funded entities

Foreign entities or non-residents donating to Indian political parties

Eligible Recipients Where Must the Donation Go?

Your contribution must be made to one of the following:

A political party registered under Section 29A of the Representation of the People Act, 1951 verified by the Election Commission of India at eci.gov.in

An electoral trust approved under Section 13B of the Income Tax Act and notified by the CBDT

Donations to NGOs, social welfare organisations, independent candidates, or any party not registered with the Election Commission of India do not qualify and this is one of the most common triggers for disallowance.

Mode of Payment : Only Non-Cash Contributions Qualify

This is a hard, non-negotiable statutory rule. Cash donations are completely ineligible for Section 80GGC deduction. Only these modes are accepted:

Cheque or demand draft

Internet banking (NEFT / RTGS)

UPI transfer

Debit card or credit card

Wire transfer through legitimate banking channels

“The moment a client tells me they donated in cash or that a party arranged the receipt afterward, I know we have a serious problem. Cash donations are not just disallowed — they can trigger fraud allegations and penalties of up to 200%.” Adwani and Company

How to Claim Section 80GGC Deduction in Your ITR :Step-by-Step Process for 2026

Claiming the Section 80GGC deduction is straightforward if your contribution is genuine and well-documented. Here is the step-by-step process:

Step 1 : Verify party registration: Before making any contribution, confirm on eci.gov.in that the party is duly registered under Section 29A of the Representation of the People Act, 1951. Note the party’s PAN you will need it while filing.

Step 2 : Donate via banking channels only: Transfer the amount via cheque, bank transfer, UPI, or card. Retain your bank statement showing the debit. Never use cash or a middleman.

Step 3 : Obtain the official donation receipt: The political party must issue a formal receipt containing the donor’s name, donation amount, date, mode of payment, party PAN, and party TAN. This receipt is your primary evidence for claiming and defending the deduction.

Step 4 : Choose the old tax regime: Section 80GGC is unavailable under the new tax regime under new income tax rules April 2026. Your regime choice must be made at the time of filing.

Step 5 : Declare in the correct ITR field: Navigate to the Chapter VI-A deductions section of your ITR form and enter the Section 80GGC amount accurately, including party PAN and payment details.

Step 6 : Inform your employer (salaried taxpayers): Submit the donation proof to your employer so they can include it in Form 16 and adjust TDS. Discrepancies between Form 16 and your ITR are a common scrutiny trigger.

Step 7 : Preserve all documentation for 6 years: Receipts are not uploaded while filing but must be retained — the Income Tax Department can open scrutiny for up to 6 prior years.

Section 80GGC Deduction : A Practical Numerical Example

Mr. Arjun Mehta is a salaried professional in Mumbai with an annual gross total income of ₹12,00,000 for Financial Year 2025-26 (Tax Year 2025-26 under the Income Tax Act 2025 / AY 2026-27 under the older terminology). He donates ₹1,50,000 via UPI to a registered political party’s bank account and receives an official receipt with the party’s PAN and TAN.

Gross Total Income: ₹12,00,000

Section 80GGC Deduction Claimed: ₹1,50,000 (100% of donation fully deductible)

Taxable Income after deduction: ₹10,50,000

Approximate tax saved at 30% slab: ₹45,000

Effective cost of the donation to Mr. Mehta: ₹1,05,000 after tax benefit

Now contrast this with a problematic scenario: Mr. Vikram Shah donates ₹2,00,000 in cash to a local party that is not registered under Section 29A. He claims ₹2,00,000 under Section 80GGC. During scrutiny, the department finds the donation was cash-based and the party is unregistered. Result: full disallowance, the ₹2,00,000 added back to his income, and a penalty under Section 270A potentially ranging from ₹60,000 to ₹1,20,000 plus interest under Sections 234A, 234B, and 234C.

The difference between Mr. Mehta and Mr. Shah is not the amount donated — it is the process followed. Documentation and compliance are everything.

Section 80GGC Disallowance : Why the Income Tax Department Is Rejecting Claims in 2026

The Income Tax Department has made Section 80GGC one of its top scrutiny priorities. The CBDT and the department’s Investigation Wing have conducted coordinated searches on political parties and related entities, uncovering widespread misuse of this provision. Here are the core reasons deductions are being disallowed:

Reason for Disallowance

Risk Level

Consequence

Cash or kind donation

Very High

100% disallowance + penalty under Section 270A

Donation to unregistered party

Very High

Full disallowance no appellate relief

Missing receipt / party PAN

High

Deduction rejected at scrutiny stage

Donation exceeds total taxable income

Medium

Excess amount disallowed

Accommodation entry / fake donation

Extreme

Disallowance + 200% penalty + prosecution risk

Claimed under new tax regime

High

Deduction invalid added back to income

The Accommodation Entry Problem : What Every Donor Must Understand

In numerous cases across India, certain small or obscure registered political parties have been found operating as accommodation entry conduits. A taxpayer ‘donates’ money via bank transfer to such a party, receives a receipt, and the funds are routed back through intermediaries — minus a commission. The donor claims a 100% tax deduction while effectively retaining the money. This is structured tax fraud.

Courts including multiple ITATs and the CBDT have taken a firm stance: a Section 80GGC disallowance based on accommodation entry findings is legally valid even when the receipt exists and the payment was non-cash if the department can demonstrate that the donation was systematically layered and returned to the donor.

In a documented case, the Ahmedabad ITAT upheld the disallowance of ₹1,13,51,000 claimed as Section 80GGC deduction after establishing that the political parties involved used bank accounts for systematic fund layering and routing through intermediaries. The assessee could not rebut this evidence, and the deduction was denied in full.

What the Income Tax Department Is Actively Doing Right Now

As confirmed by tax practitioners and reported by CNBC-TV18, the Income Tax Department has sent SMS and email alerts to thousands of taxpayers who claimed Section 80GGC deductions in AY 2024-25 and AY 2025-26, asking them to verify and rectify their claims by filing an Updated ITR (ITR-U). The red flags that trigger scrutiny include:

Donation amounts disproportionately high relative to gross income (such as donating 40–50% of annual earnings)

Donations to political parties with no visible public activity, elections contested, or verifiable presence

Multiple taxpayers from the same organisation or locality claiming identical donation amounts to the same obscure party

Donations made through intermediaries rather than directly to the party’s officially registered bank account

Receipts lacking the party’s PAN, TAN, or official seal

How to Protect Your Section 80GGC Deduction Claim and Avoid Disallowance

If your claim is genuine, you have every right to defend it and with proper documentation and professional support, most genuine claims can be successfully protected. Here is what Adwani and Company recommend:

Verify party registration before donating: Check eci.gov.in to confirm the party is registered under Section 29A of the Representation of the People Act, 1951. Do this before transferring any money. Take a screenshot as evidence.

Maintain a complete paper trail: Your bank statement must show the exact amount debited on the exact date, to the party’s officially registered bank account. Keep this along with the donation receipt, party PAN, party TAN, and your ITR acknowledgment.

Never route through intermediaries: Make the transfer directly from your personal bank account to the party’s official account. Any middleman creates a legal vulnerability the department will exploit.

File correctly under the old tax regime: Confirm your regime choice before filing. Section 80GGC is unavailable under the new regime — claiming it while under the new tax regime results in automatic disallowance.

Act on ITD SMS alerts promptly: If you receive an SMS or email from the Income Tax Department questioning your Section 80GGC claim, consult a qualified CA immediately. Filing a voluntary Updated ITR (ITR-U) within one year attracts only 25% additional tax on the shortfall far less painful than waiting for a full scrutiny notice.

How Adwani and Company Helps Taxpayers Navigate Section 80GGC Claims and Notices

At Adwani and Company, Section 80GGC advisory both pre-filing guidance and post-notice defence is a core part of the firm’s income tax practice. Dr. Haresh Adwani and his specialist team work with individual taxpayers, HUFs, and business owners across India to ensure political donation claims are made correctly, defensibly, and in full compliance with the Income Tax Act 2025 and the latest CBDT guidelines.

If you have received a scrutiny notice, an SMS alert, or a proposed disallowance relating to your Section 80GGC claim, the team at Adwani and Company can:

Conduct a detailed legal review of your claim, documentation, and the department’s query

Assess whether the political party you donated to is at risk of accommodation entry classification

Prepare a comprehensive, legally sound written response to the Income Tax Department or Assessing Officer

Represent you before the AO, CIT(Appeals), or ITAT as required

Guide you on whether filing an Updated ITR is appropriate and financially advantageous

Advise on penalty mitigation strategies under Sections 270A and 271AAC

As Dr. Haresh Adwani notes: “A genuine claim, properly documented and professionally presented, stands up under scrutiny. The clients who face real damage are those who either made the donation incorrectly or responded to the notice without expert guidance. Both problems are entirely avoidable.”

Frequently Asked Questions About Section 80GGC Deduction and Disallowance

1: Is Section 80GGC available under the new tax regime 2026?

No. Section 80GGC is a Chapter VI-A deduction available only under the old tax regime. If you have opted for the new tax regime under the Income Tax Act 2025 or new income tax rules April 2026, you cannot claim this deduction. Claiming it while under the new regime leads to disallowance and interest.

2: What is the maximum deduction limit under Section 80GGC?

Section 80GGC allows a 100% deduction on the amount donated, with no fixed rupee upper cap. However, the total deduction cannot exceed your total taxable income for the year. Contributions beyond that amount will be partly disallowed.

4: What happens if my Section 80GGC deduction is disallowed?

The donated amount is added back to your taxable income, creating a higher tax demand. On top of the additional tax, you face interest under Sections 234A, 234B, and 234C, plus a penalty under Section 270A ranging from 50% to 200% of the under-reported tax. You retain the right to appeal the disallowance before CIT(Appeals) and ITAT.

FAQ 5: Can I claim Section 80GGC if I donate to an electoral trust?

Yes, provided the electoral trust is approved under Section 13B of the Income Tax Act and notified by the CBDT. Verify its approval status before donating. The same conditions apply non-cash payment, proper receipt, and filing under the old tax regime.

7: How is the Section 80GGC deduction different from Section 80C deduction?

Section 80C allows deductions for investments like PPF, ELSS, life insurance premiums, and home loan principal repayment capped at ₹1.5 lakh per year. Section 80GGC allows deductions specifically for political party donations with a 100% deduction and no fixed rupee cap. Both deductions are independent and can be claimed simultaneously under the old tax regime. Read our detailed guide on the Old Tax Regime Deductions List 2026 at itradvisor.in for a full comparison.

Conclusion : Section 80GGC Is Powerful, But Only When Used Correctly

Section 80GGC is not a problematic provision it is a powerful, legitimate tool for tax planning that simultaneously supports transparent political funding in India. The issue arises when it is misused, inadequately documented, or claimed without meeting the statutory conditions. In 2026, with the Income Tax Department actively scrutinising these claims and the CBDT empowered to issue compliance alerts to lakhs of taxpayers, the cost of getting this wrong has never been higher.

If your Section 80GGC claim is genuine made to a registered party, via banking channels, with a proper receipt, and declared under the old tax regime you have nothing to fear. A well-documented, professionally presented claim will withstand scrutiny. But if there are gaps in your process, acting quickly through a voluntary Updated ITR or a strong professional response to any notice received is far better than waiting.

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

Freelancer ITR Filing AY 2026-27: Everything You Need to Know

You deliver world-class work design, code, content, consulting and then comes the one thing that trips up almost every freelancer in India: tax filing. If you’ve been Googling ‘how to file ITR for freelancer’ or wondering which ITR form freelancers must use for AY 2026-27, you’re not alone. And you’ve landed in exactly the right place.

Freelancers, independent consultants, and self-employed professionals face a unique tax situation. Unlike salaried individuals whose employer handles TDS and Form 16, freelancers must manage their own advance tax, deductions, GST obligations, and ITR filing. The good news? India’s tax law has a powerful provision Section 44ADA that makes freelancer tax compliance far simpler and more tax-efficient than most people realize.

This guide walks you through every critical step of freelancer ITR filing for AY 2026-27 from selecting the right form to claiming deductions and filing before the deadline without stress.

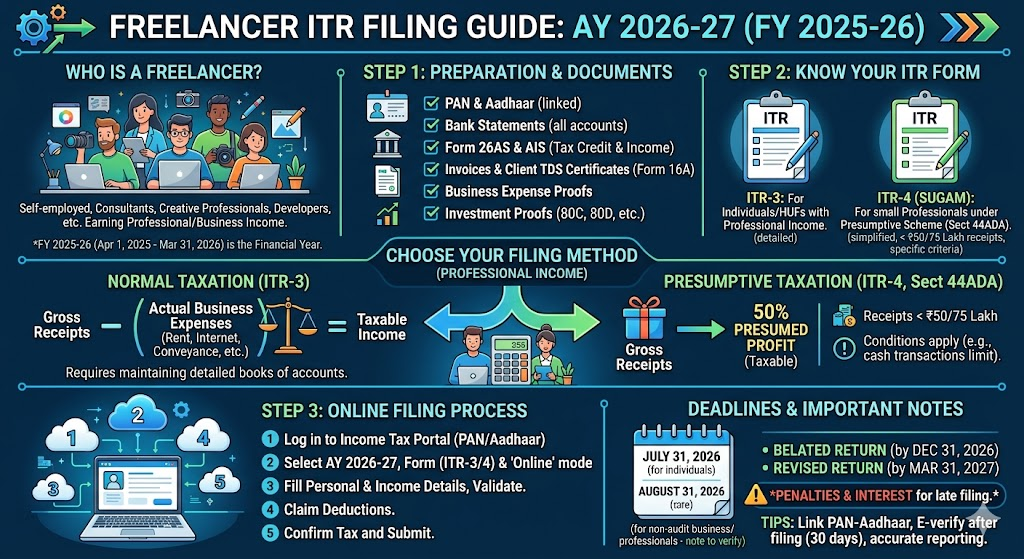

Which ITR Form Should a Freelancer File for AY 2026-27?

This is the most common question and getting it wrong can lead to a defective return notice from the Income Tax Department. Here’s what you need to know:

ITR-4 (Sugam): This is the correct form for most freelancers and self-employed professionals who opt for the Presumptive Taxation Scheme under Section 44ADA. If your gross professional receipts are up to ₹75 lakh in FY 2025-26, ITR-4 is your go-to form.

ITR-3: If you maintain books of accounts, have multiple income sources (business + capital gains + house property), or your receipts exceed ₹75 lakh, you must file ITR-3.

ITR-1 (Sahaj): Not applicable for freelancers. Do not make this common mistake.

Understanding Section 44ADA: The Freelancer’s Best Tax Friend

Section 44ADA of the Income Tax Act is a game changer for freelance professionals such as doctors, lawyers, architects, engineers, designers, content writers, software consultants, and other notified professionals. Under this presumptive taxation scheme for AY 2026-27:

50% of your gross professional receipts is deemed as your net taxable income (profit).

You do not need to maintain detailed books of accounts.

No requirement for a tax audit (unless you declare profit lower than 50% and your income exceeds the basic exemption limit).

The gross receipt limit for Section 44ADA is ₹75 lakh for FY 2025-26.

Example: If a freelance graphic designer earned ₹12 lakh in FY 2025-26, only ₹6 lakh (50%) is treated as taxable income. After applying the standard deduction of ₹75,000 under the new tax regime, the effective taxable income drops further, making Section 44ADA an exceptionally tax-efficient route.

Advance Tax for Freelancers: Deadlines You Cannot Miss in FY 2026-27

One of the most overlooked compliance areas for freelancers is advance tax. Since no TDS is deducted on most freelance payments (or TDS is deducted at a lower rate), you are required to pay advance tax if your total tax liability exceeds ₹10,000 in a year.

Advance Tax Due Dates FY 2026-27 for Freelancers:

15th June 2026: Pay at least 15% of total estimated tax

15th September 2026: Cumulative 45% of total estimated tax

15th December 2026: Cumulative 75% of total estimated tax

15th March 2027: 100% of total estimated tax

Important: Freelancers opting for Section 44ADA can pay 100% advance tax in one installment by 15th March a significant compliance relief compared to regular businesspersons.

Missing advance tax deadlines attracts interest under Sections 234B and 234C of the Income Tax Act. Read our detailed guide on Advance Tax Due Dates FY 2026-27 for complete installment schedules and penalty calculations.

Smart Tax Deductions Every Freelancer Must Claim in AY 2026-27

Even if you opt for Section 44ADA, certain deductions are still available to freelancers that can significantly reduce your final tax liability. According to guidelines from the Income Tax Department, the following deductions apply:

Standard Deduction of ₹75,000 under the new tax regime (from FY 2025-26 onwards)

Section 80C: Up to ₹1.5 lakh via PPF, ELSS, LIC, NSC applicable only under the old regime

Section 80D: Health insurance premium for self and family

Section 80CCD(1B): Additional ₹50,000 via NPS contribution available under old regime

Home loan interest under Section 24(b) if applicable

If you are under the old tax regime: Learn more about our Tax Planning Service to identify the most beneficial deductions for your specific income profile.

Dr. Haresh Adwani, a practising chartered accountant and founder of Adwani & Co LLP, advises freelancers to carefully model both old and new tax regimes before AY 2026-27 filing, especially given the enhanced standard deduction under the new regime.

Step-by-Step: How to File Freelancers ITR for Online for AY 2026-27

Here’s a simplified step-by-step filing process for freelancers ITR in India following the workflow outlined on incometax.gov.in:

Step 1 : Collect Your Financial Records: Gather all invoices raised, payments received, TDS certificates (Form 16A), and your bank statements for FY 2025-26.

Step 2 : Download and Verify Form 26AS & AIS: Log in to the Income Tax portal. Match your TDS credits, high-value transactions, and income details. Any mismatch here is a red flag. Read our detailed guide on Form 26AS vs AIS vs TIS: Key Differences & How to Match Them Before Filing ITR.

Step 3 : Choose Your Tax Regime: Decide between old and new tax regime. For most freelancers earning under ₹15 lakh without major deductions, the new regime is now more favourable.

Step 4 : Select ITR-4 (If Section 44ADA Applies): Login to incometax.gov.in → e-File → Income Tax Returns → File Income Tax Return → Select AY 2026-27 → ITR-4.

Step 5 : Fill in Income Details: Under the ‘Business/Profession’ schedule in ITR-4, enter your gross receipts and declare 50% as profit under 44ADA.

Step 6 : Claim Deductions & Compute Tax: Enter eligible deductions and let the system compute your final tax payable.

Step 7 : Pay Self-Assessment Tax (If Any): If tax is payable after TDS and advance tax, pay it via Challan 280 before filing.

Step 8 : Verify and Submit: e-Verify via Aadhaar OTP, net banking, or DSC. Your ITR is filed!

Read our detailed guide on How to File ITR Online 2026: Step-by-Step Guide for Salaried & Freelancers for a more detailed walkthrough with screenshots.

GST Registration for Freelancers: Do You Need It?

A frequently misunderstood area for freelancers is GST compliance. Under current GST rules:

GST registration is mandatory if your aggregate turnover exceeds ₹20 lakh (₹10 lakh for special category states) in a financial year.

If you provide services to clients outside India (export of services), you are exempt from GST but registration may still be beneficial for claiming refunds on input tax credits.

Freelancers registered under GST must file GSTR-1 and GSTR-3B returns regularly.

Non-compliance with GST obligations can attract notices under the GST portal (gstn.gov.in). Learn more about our GST Compliance Service to stay audit-proof.

Key Takeaways

What Every Freelancer Must Remember for AY 2026-27

File ITR-4 if your gross professional receipts are up to ₹75 lakh Section 44ADA makes it simple.

Only 50% of your gross receipts is taxable under Section 44ADA a powerful built-in deduction.

Pay advance tax on time to avoid interest under Sections 234B and 234C.

Verify Form 26AS and AIS before filing mismatches can trigger scrutiny notices.

The ITR filing last date for AY 2026-27 (non-audit cases) is 31st July 2026 file on time to avoid penalties.

GST registration is mandatory once your annual receipts cross ₹20 lakh.

Frequently Asked Questions (FAQs)

Q1. Which ITR form should a freelancer file for AY 2026-27?

Most freelancers should file ITR-4 (Sugam) if their gross receipts are up to ₹75 lakh and they opt for the presumptive taxation scheme under Section 44ADA. ITR-3 applies if receipts exceed this limit or if books of accounts are maintained.

Q2. What is Section 44ADA and who is eligible in AY 2026-27?

Section 44ADA allows notified professionals (doctors, lawyers, engineers, consultants, designers, etc.) to declare 50% of gross receipts as taxable income without maintaining books. Eligibility requires gross professional receipts of up to ₹75 lakh in FY 2025-26.

Q3. Do freelancers need to pay advance tax for FY 2026-27?

Yes, if total tax liability exceeds ₹10,000 in the year. Freelancers under Section 44ADA enjoy the benefit of paying 100% of advance tax in a single installment by 15th March 2027, unlike regular taxpayers who pay in four installments.

Q4. Is GST registration mandatory for all freelancers in India?

GST registration is mandatory only if your aggregate annual turnover exceeds ₹20 lakh (₹10 lakh in special category states). Freelancers providing export services to foreign clients are generally exempt but may benefit from voluntary GST registration for ITC refunds.

Q5. What is the last date for freelancer ITR filing for AY 2026-27?

The due date for ITR filing AY 2026-27 for non-audit cases (including most freelancers under Section 44ADA) is 31st July 2026. A late filing fee of up to ₹5,000 under Section 234F applies if you miss this deadline.

Conclusion: File Right, Save More, Stay Compliant

Freelancing gives you freedom and with the right tax knowledge, it also gives you the freedom to keep more of what you earn. The ITR filing process for freelancers in India for AY 2026-27 is far more streamlined than most people think, especially with the powerful benefits of Section 44ADA and the new tax regime.

The key is to start early: reconcile your Form 26AS and AIS now, decide your tax regime, calculate your advance tax liability, and file before the 31st July 2026 deadline. Don’t let procrastination convert a simple filing into a panic-driven exercise with penalties.

🚀 Need Expert Help with Your Freelancer ITR? Stop second-guessing your taxes. Connect with the experts at itradvisor.in today for personalised guidance on freelancer ITR filing, Section 44ADA, advance tax planning, and GST compliance — all in one place. 👉 Visit itradvisor.in | Expert Tax Guidance. Zero Confusion.