GST Compliance Checklist for Small Businesses in Pune

Running a small business in Pune whether it is a trading shop in Chinchwad, a manufacturing unit in Bhosari MIDC, a restaurant in Koregaon Park, or a service firm in Baner means navigating one of the most compliance-dense tax frameworks in India. GST is not a one-time registration event; it is a continuous, monthly, quarterly, and annual cycle of filings, reconciliations, and record-keeping. Miss a deadline and the penalties start adding up. Miss a reconciliation and your Input Tax Credit evaporates. Miss a compliance threshold and you risk GST notices, scrutiny, or worse, cancellation of your GST registration. This checklist exists so that Pune’s small business owners never have to miss a step.

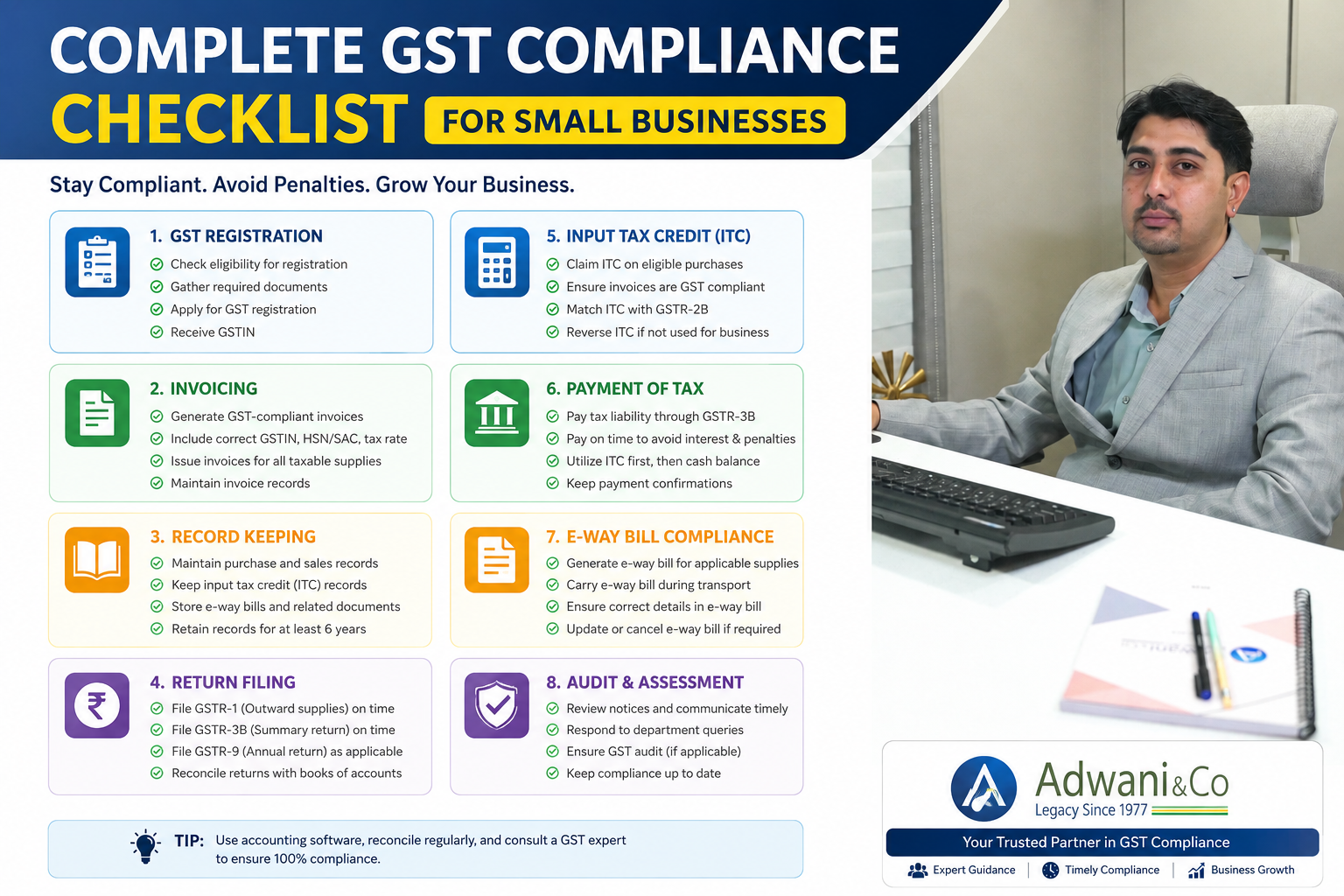

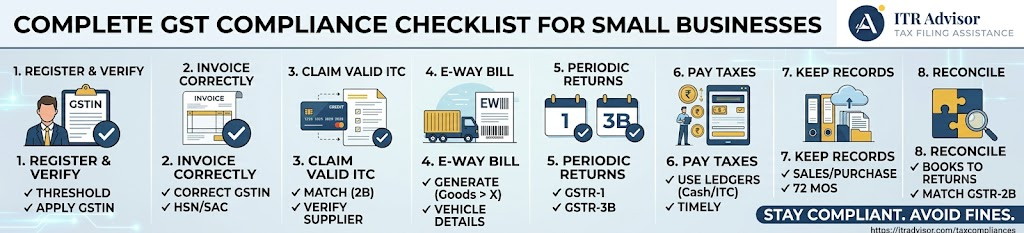

Step 1: GST Registration Compliance for Small Businesses in Pune

Before anything else, confirm that your GST registration status is current and accurate. Under the GST Act, registration is mandatory if your annual aggregate turnover exceeds ₹40 lakh (for goods suppliers) or ₹20 lakh (for service providers) in Maharashtra. Businesses making inter-state supplies, e-commerce sellers, and those liable for reverse charge mechanism (RCM) must register regardless of turnover.

GST compliance checklist for registration:

- Verify that your GSTIN is active on the GST Portal (gst.gov.in) under the ‘Search Taxpayer’ function.

- Ensure all business addresses including godowns, branches, or additional Pune locations are declared as additional places of business in your GST registration.

- Confirm that your principal place of business, HSN/SAC codes, and authorised signatory details are up to date.

- If your turnover has crossed the mandatory threshold during FY 2026-27, apply for GST registration immediately — delayed voluntary registration is treated as non-compliance.

- If you opted for the GST Composition Scheme (available for eligible Pune traders and manufacturers with turnover up to ₹1.5 crore), verify you are filing CMP-08 quarterly and GSTR-4 annually.

Step 2: GST Return Filing Deadlines for FY 2026–27 : Complete Calendar for Pune Businesses

The most common cause of GST notices for small businesses in Pune is missed or delayed return filings. The GST return compliance calendar for FY 2026-27 is as follows:

| Return / Filing | Who Must File | Due Date (FY 2026-27) | Penalty for Late Filing |

| GSTR-1 (Monthly) | Regular taxpayers with turnover > ₹5 crore | 11th of following month | ₹50/day (nil return ₹20/day), max ₹10,000 |

| GSTR-1 (Quarterly/IFF) | QRMP scheme taxpayers (turnover ≤ ₹5 crore) | 13th of month after quarter-end | ₹50/day, max ₹10,000 |

| GSTR-3B (Monthly) | Regular taxpayers (auto-populated from FY 2025-26) | 20th/22nd/24th (based on state/zone) | ₹50/day + 18% interest on tax due |

| GSTR-3B (Quarterly) | QRMP scheme taxpayers | 22nd/24th after quarter-end | ₹50/day + 18% interest on tax due |

| GSTR-9 (Annual Return) | Turnover > ₹2 crore (FY 2025-26 basis) | 31st December 2026 | ₹200/day, max 0.25% of turnover |

| GSTR-9C (Reconciliation) | Turnover > ₹5 crore | 31st December 2026 | Same as GSTR-9 penalty structure |

| CMP-08 (Composition) | Composition scheme taxpayers | 18th of month after quarter-end | ₹50/day, max ₹2,000 |

| GSTR-4 (Composition Annual) | Composition scheme taxpayers | 30th April 2027 | ₹50/day, max ₹2,000 |

For Pune businesses on the QRMP (Quarterly Return Monthly Payment) scheme, note that tax must still be paid monthly either through the Fixed Sum Method or Self-Assessment Method even though the return itself is quarterly. QRMP is generally the right choice for Pune MSMEs and small traders with turnover below ₹5 crore.

Step 3: Input Tax Credit (ITC) Reconciliation: The Most Critical GST Compliance Task

Input Tax Credit is the primary financial benefit of GST registration for small businesses in Pune. But ITC can be claimed only if the conditions under Section 16 of the CGST Act are satisfied and this is where most Pune small business owners inadvertently lose money.

ITC GST Compliance Checklist for FY 2026-27

- Reconcile GSTR-2B (auto-generated ITC statement) with your purchase register and books of accounts every month before filing GSTR-3B.

- ITC is available only if the supplier has filed GSTR-1 and the invoice appears in your GSTR-2B. Follow up actively with non-compliant suppliers whose invoices are missing.

- Ensure ITC is claimed within the time limit: for FY 2025-26 invoices, the deadline to claim ITC is the earlier of the due date of September 2026 GSTR-3B or the date of filing the annual return.

- Do not claim ITC on blocked credits under Section 17(5) of the CGST Act these include motor vehicles (with exceptions), food and beverages, personal use goods, and construction services.

- If you have both taxable and exempt supplies, calculate and reverse ineligible ITC under the proportionate method as required by the CGST Rules.

Step 4: E-Invoicing Compliance for Pune Small Businesses

The GST e-invoicing threshold has been progressively lowered by CBIC. As of FY 2026-27, e-invoicing under the GST framework is mandatory for all registered taxpayers with aggregate annual turnover exceeding ₹5 crore in any preceding financial year. For many growing Pune traders, manufacturers, and service exporters, this threshold is now a near-term reality.

E-invoicing GST compliance checklist:

- Verify whether your FY 2024-25 or FY 2025-26 turnover crossed ₹5 crore if yes, e-invoicing is mandatory for all B2B transactions from the applicable date.

- Ensure your accounting or ERP software is integrated with the Invoice Registration Portal (IRP) at einvoice1.gst.gov.in to generate an IRN (Invoice Reference Number) and QR code for each B2B invoice.

- E-invoices issued without an IRN are invalid for ITC purposes — your buyer in Pune or elsewhere cannot claim ITC on such invoices, which can damage your business relationships.

- Retain copies of all e-invoices with IRN for at least six years as required under the GST record-keeping rules.

Step 5: GST Record-Keeping and Audit Trail Requirements

Under Section 35 of the CGST Act, every registered taxpayer must maintain a complete set of records at the principal place of business — or at each additional place of business in Pune — for a minimum of six years from the due date of the annual return for that year.

Records that must be maintained for GST compliance checklist:

- Purchase invoices, sales invoices, debit notes, and credit notes for all inward and outward supplies.

- Stock registers showing opening stock, purchases, production/manufacture, sales, and closing stock with HSN classification.

- Input Tax Credit ledger, Electronic Cash Ledger, and Electronic Liability Register (accessible on the GST Portal).

- Bank statements reconciled with GST turnover for the year.

- For exporters and SEZ suppliers: shipping bills, LUTs (Letter of Undertaking), and refund applications filed.

Key Takeaways:

• GST registration is mandatory for Pune businesses with turnover above ₹40L (goods) or ₹20L (services). Verify your GSTIN is active on gst.gov.in.

• File GSTR-1 and GSTR-3B on time every month or quarter. Late filing penalties start at ₹50/day and interest at 18% on unpaid tax accrues daily.

• Reconcile GSTR-2B with your purchase register monthly before filing GSTR-3B this is the single most important step to protect your ITC.

• E-invoicing is mandatory for businesses with turnover above ₹5 crore. Invoices without a valid IRN from the IRP portal are ineligible for ITC.

• Composition scheme taxpayers in Pune must file CMP-08 quarterly and GSTR-4 annually by April 30, 2027.

• Maintain all GST records for six years. The GST Department conducts audits and scrutiny up to six years from the relevant annual return due date.

Step 6: Common GST Compliance Mistakes That Pune Small Businesses Must Avoid

Reconciliation skipped: Filing GSTR-3B without cross-checking GSTR-2B leads to incorrect ITC claims, reversal demands, and scrutiny notices.

Turnover under-reporting: GST officers increasingly use e-way bill data, e-invoicing records, and bank statement analysis to detect turnover mismatches.

RCM non-compliance: Reverse Charge Mechanism liability on services like legal fees, GTA freight, and import of services is often missed by small businesses.

HSN code errors: Incorrect HSN/SAC classification leads to wrong tax rate application and potential demand with interest.

Debit/Credit note delays: Credit notes for sales returns or rate revisions must be issued and declared within the prescribed time limits to avoid ITC reversal complications for your buyers.

Read our detailed guide on GST Compliance Checklist India 2026: 7 Essential Rules to Avoid Notices and Penalties

Expert Insight: GST Compliance Is Not Annual It’s a Monthly Discipline

Dr. Haresh Adwani, a PhD in Commerce and tax expert associated with ITRAdvisor.in, has a clear message for Pune’s small business community: ‘The biggest GST compliance mistake I see among small businesses in Pune is treating GST as a year-end activity. By the time December comes and the annual return deadline approaches, the reconciliation gaps have compounded for twelve months. GSTR-2B mismatches, missed ITC claims, and overlooked RCM liabilities become expensive to fix retroactively. The businesses that stay clean are the ones that close their GST books monthly, not annually.’

Frequently Asked Questions

Q1. What is the GST registration threshold for small businesses in Pune, Maharashtra?

In Maharashtra, GST registration is mandatory or businesses supplying goods with annual turnover above ₹40 lakh and for service providers above ₹20 lakh. Inter-state suppliers must register regardless of turnover.

Q2. Which GST return scheme is better for a small Pune business monthly or QRMP?

For Pune businesses with turnover below ₹5 crore, the QRMP (Quarterly Return Monthly Payment) scheme reduces return filing from 24 to 8 per year while still requiring monthly tax payments. Most small businesses find this significantly simpler.

Q3. Is e-invoicing mandatory for my Pune small business in FY 2026-27?

E-invoicing under GST is mandatory if your aggregate turnover in any preceding financial year exceeded ₹5 crore. Check your FY 2024-25 or FY 2025-26 turnover to confirm applicability for the current year.

Q4. What is the penalty for late GST return filing in India?

The late fee for delayed GSTR-1 or GSTR-3B filing is ₹50 per day (₹20/day for nil returns), subject to a maximum of ₹10,000. Interest at 18% per annum also accrues on unpaid GST liability from the due date.

Q5. When is the GSTR-9 annual return due for FY 2025-26?

The GSTR-9 annual return for FY 2025-26 is due by December 31, 2026. It is mandatory for businesses with turnover above ₹2 crore. GSTR-9C (reconciliation statement) applies to businesses above ₹5 crore.

Conclusion

GST compliance checklist for small businesses in Pune is not a checkbox exercise it is a continuous operational discipline that directly protects your cash flow, your Input Tax Credit, and your business reputation. The CBIC and GST Council have progressively tightened enforcement mechanisms: e-invoicing mandates, automated GSTR-2B mismatches, e-way bill data triangulation, and AI-driven scrutiny selection mean that gaps in GST compliance are increasingly difficult to hide and increasingly expensive to fix.

The good news is that the GST compliance framework, while demanding, is entirely manageable with the right processes. A monthly reconciliation routine, timely GSTR-1 and GSTR-3B filings, clean ITC documentation, and proper e-invoicing integration will keep your Pune business fully compliant and free from notices, penalties, and demand orders.

Is your Pune small business fully GST compliant for FY 2026-27?

ITRAdvisor.in provides clear, actionable guidance on GST registration, return filing, ITC reconciliation, e-invoicing, and GST notice responses for small businesses across Pune and Maharashtra. Whether you are a first-time GST registrant or an established business trying to clean up your compliance record, our resources are built for you.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

A prominent “File Your ITR Now” button near the top and again at the end of the article

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.