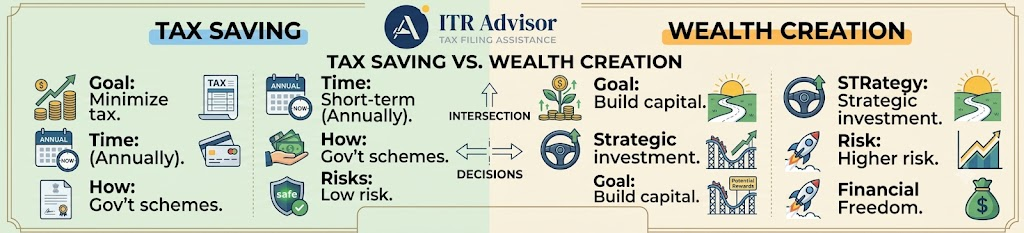

Tax Saving vs Wealth Creation

Every year, as March 31 approaches, millions of Indian taxpayers rush to ‘finish off’ their Section 80C limit. Life insurance premiums get paid. Tax-saving Fixed Deposits get booked. ELSS funds get subscribed sometimes at the last minute, without a second thought. But here is the uncomfortable question that very few people ask themselves: If there were no tax benefit attached to this investment, would you still make it? That single question is the difference between tax saving and genuine wealth creation in India and understanding it could be the most financially important thing you do this year.

The Section 80C Habit: How Tax Saving Became a Financial Reflex in India

For decades, tax saving and investing were treated as the same activity by most Indian middle-class households. The logic was simple and appealing: invest ₹1.5 lakh under Section 80C, reduce your taxable income, get a tax refund, and feel financially responsible. The products that became staples of this approach included:

- LIC traditional endowment and money-back policies

- 5-year tax-saving Fixed Deposits at banks and post offices

- ELSS (Equity Linked Savings Scheme) mutual funds with a 3-year lock-in

- Public Provident Fund (PPF) and National Savings Certificates (NSC)

- Employee Provident Fund (EPF) contributions

None of these instruments are inherently bad. But the problem arises when tax saving in India becomes the primary or only reason for investment decisions. When you invest because of a tax deadline rather than a financial goal, you are not building wealth. You are buying a deduction.

Warning: The Hidden Cost of Deadline-Driven Tax Saving

- You may lock money into products that earn 4–6% returns while inflation runs at 5–6% effectively zero real growth

- High-premium LIC policies taken for 80C often have poor surrender value if financial needs change

- Tax-saving FDs are fully taxable on maturity the tax saved upfront may be recovered by the government later

Investing under pressure in March reduces your ability to select the right product for your actual goals

How the New Tax Regime Has Changed the Tax Saving vs Wealth Creation Debate in India

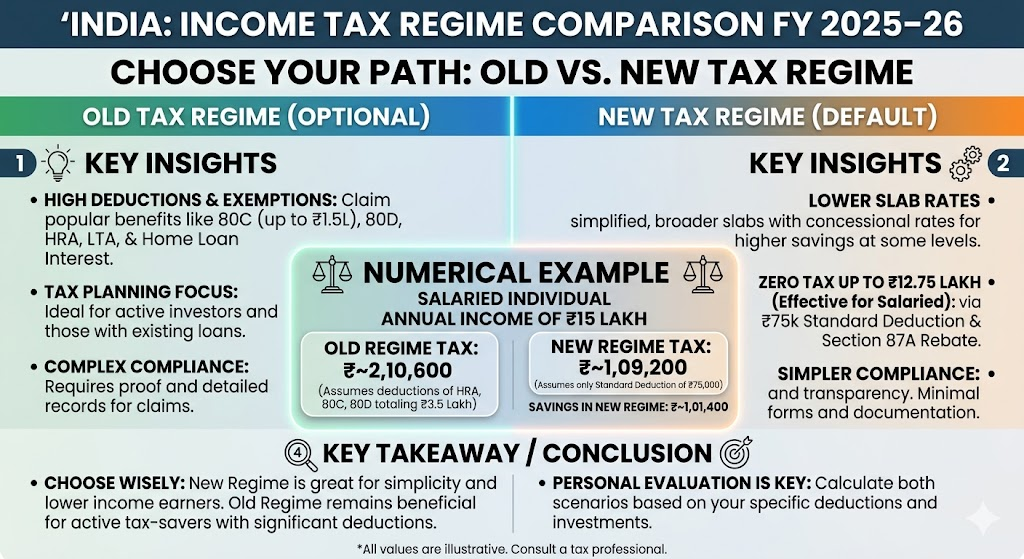

The Income Tax Department’s push toward the New Tax Regime backed by significant structural changes in Budget 2024 and continuing into AY 2026-27 has fundamentally altered the calculus of tax-saving investing in India. Under the new regime, most deductions including Section 80C, 80D, and HRA are not available. In exchange, taxpayers benefit from a zero-tax threshold on income up to ₹12 lakh under Section 87A (as announced in Budget 2025) and a revised standard deduction of ₹75,000 for salaried individuals.

This means that a large segment of Indian taxpayers — particularly those in the ₹8–15 lakh annual income bracket may already have a lower or even zero tax liability under the new regime, without making a single 80C investment. And yet, many continue to invest in lock-in products simply out of habit or peer pressure, without running the actual numbers.

According to guidance from the Income Tax Department of India (incometaxindia.gov.in), taxpayers can switch between the old and new tax regimes each year (subject to specific conditions for business income). This flexibility makes it more important than ever to evaluate whether your tax-saving investments are still serving a purpose or simply tying up capital that could be working harder for you.

Read our detailed guide on Old vs New Tax Regime 2025: Stop Guessing, Start Calculating

Tax Saving vs Wealth Creation in India: A Side-by-Side Comparison

Let us be specific. The table below captures the fundamental difference between a tax-saving approach and a wealth creation approach to investing in India:

| Dimension | Tax Saving Focus | Wealth Creation Focus |

| Primary Goal | Reduce tax liability this financial year | Grow net worth over 5, 10, 20 years |

| Decision Driver | March 31 deadline pressure | Life goals: retirement, home, education |

| Typical Products | LIC endowment, tax-saving FD, NSC | Equity mutual funds, NPS, direct equity, index funds |

| Risk Awareness | Often low safety prioritised over returns | Calibrated risk taken for inflation-beating returns |

| New Regime Impact | 80C deductions no longer available | Investment logic holds regardless of tax regime |

| Returns Expectation | 4–6% (often below inflation) | 10–14% CAGR over long term (equity-linked) |

| Real Wealth Built? | Moderate tax saved, but corpus modest | Significant compounding works powerfully over time |

The data is clear: wealth creation in India requires a different mindset, a different product selection process, and a different time horizon than tax saving. The two can overlap for example, ELSS mutual funds offer both but they should never be conflated

A Real Example: How Tax Saving Investments vs Wealth Creation Investments Perform Over 20 Years

Consider Rajesh, a 35-year-old salaried professional in Pune earning ₹15 lakh per annum. Every year, he invests ₹1.5 lakh under Section 80C in a traditional LIC endowment policy with an effective return of approximately 5% per annum. Over 20 years, his maturity corpus would be approximately ₹49–52 lakh.

Now consider his colleague Priya. She switches to the new tax regime (where 80C is irrelevant), and instead invests the same ₹1.5 lakh per year in a diversified equity mutual fund SIP averaging 12% CAGR consistent with long-term Nifty 50 returns over 15–20 year periods. After 20 years, Priya’s corpus would be approximately ₹1.37 crore nearly three times Rajesh’s corpus.

Rajesh saved tax. Priya built wealth. Both invested the same amount. The difference? Rajesh’s investment decision was driven by Section 80C. Priya’s was driven by a financial goal retirement.

Key Insight:

- ₹1.5 lakh/year at 5% for 20 years → ~₹50 lakh maturity corpus

- ₹1.5 lakh/year at 12% for 20 years → ~₹1.37 crore maturity corpus

- The difference of ₹87 lakh is the cost of investing for a deduction instead of for wealth

LTCG on equity mutual funds above ₹1.25 lakh per year is taxed at only 12.5% under Section 112A still far more tax-efficient than interest income

What Wealth Creation in India Actually Looks Like: Smart Investment Alternatives

The shift in conversations Dr. Haresh Adwani has observed at Adwani and Company during this ITR season is telling. Fewer clients are asking ‘How do I finish my Section 80C?’ and more are asking about mutual funds, equity SIPs, retirement planning, and financial independence. This is not just a trend it reflects a maturing financial culture in India.

Here are the wealth creation investment strategies that make sense with or without a tax benefit attached:

1. Equity Mutual Funds and SIPs for Long-Term Wealth Creation

Index funds and diversified equity mutual funds remain the most accessible and proven vehicle for wealth creation in India. With no lock-in (outside ELSS), full liquidity, and the power of compounding over 10–20 years, equity mutual funds outperform most tax-saving instruments by a significant margin. SEBI’s investor education portal (investor.sebi.gov.in) consistently highlights goal-based SIP investing as the most reliable path to long-term wealth for retail investors.

2. National Pension System (NPS) for Retirement Planning

NPS offers an additional deduction of ₹50,000 under Section 80CCD(1B) over and above the ₹1.5 lakh 80C limit and it remains available even under certain corporate tax arrangements. More importantly, it functions as a genuine retirement wealth-building vehicle with equity exposure and annuity options. For taxpayers under the new regime, NPS still has partial tax advantages, making it one of the smartest straddlers of both worlds.

3. Direct Equity Investing with LTCG Tax Efficiency

Post-Budget 2024 amendments, long-term capital gains (LTCG) on listed equity shares held for more than 12 months are taxed at 12.5% above ₹1.25 lakh of gains per year. This remains one of the most tax-efficient return profiles available to Indian investors. For individuals with the knowledge and risk appetite, building a portfolio of quality businesses over time is genuine wealth creation in India and it requires zero 80C motivation.

4. ELSS Mutual Funds: The Best of Both Worlds

For taxpayers who remain on the old tax regime and want to maximise both tax saving and wealth creation, ELSS mutual funds are still the most intelligent Section 80C instrument. They carry a mandatory 3-year lock-in, but are equity linked, historically return-positive over 5–10 year holding periods, and allow SIP investing. The tax benefit is a bonus not the reason to invest.

The 3 Questions That Separate Tax Savers from Wealth Creators in India

Dr. Haresh Adwani, PhD in Commerce and a law graduate with deep expertise in integrated tax and financial planning, advocates a three-question framework before every investment decision. This framework simple but powerful ensures that your investments serve your life goals rather than your tax receipt:

- Does this investment fit my financial goals? (Not just ‘Does it qualify for 80C?’)

- Do I fully understand the risks, lock-in, liquidity, and real returns of this product?

- Would I still invest in this if there was zero tax benefit attached to it?

If the answer to question three is a clear no, that is a signal worth paying attention to. You may be buying a deduction not building wealth.

Common Mistake: What Many Indian Investors Get Wrong About Tax Planning

- Treating tax planning as a year-end activity rather than a year-round financial strategy

- Confusing tax saving instruments with wealth-creating instruments they are not always the same

- Not comparing the new vs old tax regime before committing to 80C investments every April

- Ignoring the impact of inflation on low-return tax-saving products over a 15–20 year period

Missing the additional ₹50,000 NPS deduction under Section 80CCD(1B) a widely underutilised wealth-and-tax benefit

Frequently Asked Questions

Q: Is Section 80C investment still worth it under the new tax regime in India for AY 2026-27?

A: Under the new tax regime, Section 80C deductions are not available. If you opt for the new regime, focus on investments that deliver the best returns for your goals not tax deductions. Evaluate both regimes with a CA before deciding.

Q: What is the difference between tax saving and wealth creation in India?

A: Tax saving reduces your current year’s tax liability through specific investments or deductions. Wealth creation builds your long-term net worth through returns that compound over time ideally in a tax-efficient way.

Q: Which investments are best for wealth creation in India without depending on Section 80C?

A: Equity mutual funds, index funds, direct equity, NPS, and goal-based SIPs are the most powerful wealth creation vehicles in India. Their returns typically outperform 80C instruments significantly over a 10–20 year period.

Q: Can I switch between old and new tax regime every year in India?

A: Salaried individuals can switch between regimes each financial year. However, those with business or professional income face restrictions. Consulting a CA like the team at Adwani and Company is advisable before switching.

Q: How is LTCG on equity mutual funds taxed in India after Budget 2024?

A: Long-term capital gains on equity mutual funds held over 12 months are taxed at 12.5% above ₹1.25 lakh per year under Section 112A. This makes equity investing one of the most tax-efficient wealth creation strategies in India.

Q: What is the three-question framework for smart investing in India?

A: Before any investment, ask: Does it fit my financial goal? Do I understand its risk and return profile? Would I still invest in it without a tax benefit? If the last answer is ‘no’, reconsider your investment rationale.

Conclusion: Good Tax Planning Serves Wealth Creation : Not the Other Way Around

The conversation around tax saving vs wealth creation in India is evolving and that is a genuinely positive development. The fact that more taxpayers today are asking about mutual funds, retirement planning, equity investing, and financial independence, rather than just ‘how to finish 80C’, reflects a maturing financial consciousness across India’s working population.

But the shift must be made deliberately and with good information. Not all tax saving instruments are poor wealth creators. Not all wealth creation strategies ignore tax efficiency. The goal is alignment ensuring that every investment serves both your tax situation and your life goals simultaneously.

That alignment is exactly what Adwani and Company has been delivering to clients across Pune and India for nearly five decades. With Dr. Haresh Adwani’s integrated expertise in commerce, law, and taxation at the helm, the firm is uniquely positioned to help you answer the most important question in personal finance: Are you building wealth or just buying a deduction?

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP

Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP. pant, or someone navigating all three simultaneously your tax treatment, ITR form selection, and loss utilisation strategy need to be correct, consistent, and complete.

Learn more about our Income Tax Filing Services for Traders & Investors covering ITR-3 filing, tax audit support under Section 44AB, F&O turnover calculation, and capital gains reconciliation with your broker’s statement.

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later

If you or someone you know has received a Section 148 income tax reassessment notice, do not panic but do act quickly and smartly. The law is on your side, provided you know where to look.

📞 Take Action Today

Need help evaluating whether your income tax reassessment notice is valid?

Connect with the experts at itradvisor.in for a detailed assessment of your notice, legal objection drafting, and end-to-end reply support. Visit: www.itradvisor.in | Powered by Adwani & Co LLP