ESOP Valuation in India

An employee is told their ESOPs are worth Rs. 50 lakh. They celebrate. Two years later, at the time of exercise, a very different number appears on their tax statement. What went wrong? Nothing illegal. Just a number that was never properly understood or properly determined.

This is the quiet danger at the heart of ESOP valuation in India. And in 2026, as start up equity culture matures and the Income Tax Department sharpens its lens on perquisite taxation, getting this right is no longer optional for founders, CFOs, or the employees who accept these grants.

What Is ESOP Valuation in India and Why Does It Matter?

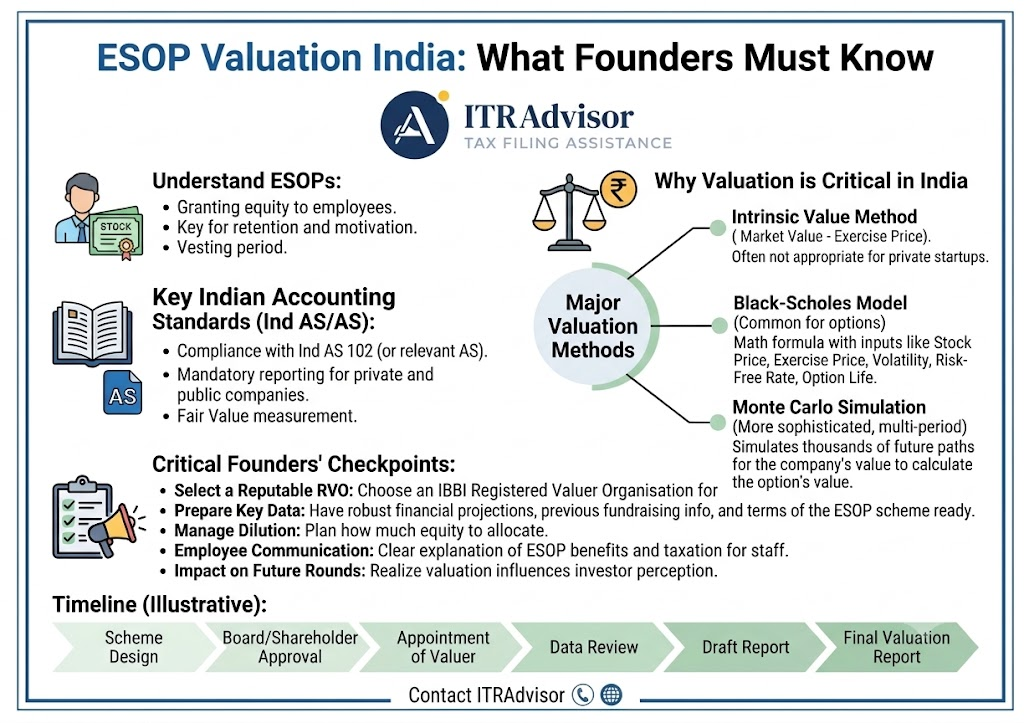

An Employee Stock Option Plan (ESOP) gives employees the right to purchase company shares at a pre-decided exercise price, typically lower than the fair market value (FMV). The difference between the FMV on the date of exercise and the exercise price is treated as a perquisite under the Income Tax Act, 1961, and is taxed as part of the employee’s salary income.

This is where ESOP valuation in India becomes critically important. The FMV on the date of exercise directly determines how much tax the employee pays. If the underlying valuation methodology is weak, arbitrary, or unsupported, it creates problems at multiple levels:

- The employee faces unexpected ESOP perquisite tax liability in India that they were not prepared for.

- The company faces questions during investor due diligence or SEBI scrutiny.

- Regulatory compliance under the Companies Act and FEMA (for ESOPs with foreign participation) becomes difficult to defend.

- Employee trust erodes when the promised equity value does not align with tax-time reality.

How Is ESOP Valuation Determined for Unlisted Companies in India?

For listed companies, the FMV of shares is straightforward it is the market price on the recognised stock exchange. For unlisted start ups, the process is more nuanced and more consequential.

As per the Income Tax Rules, the FMV of shares of an unlisted company for ESOP purposes is required to be determined by a SEBI-registered Category I Merchant Banker. This is not a valuation that the company can do internally or informally. A formally supported valuation report, applying recognised methodologies such as the Discounted Cash Flow (DCF) method or the Net Asset Value (NAV) approach, is the standard the Income Tax Department expects.

Common ESOP valuation methods for unlisted companies include:

- Discounted Cash Flow (DCF): Projects future cash flows and discounts them to present value, most relevant for growth-stage startups with revenue visibility.

- Comparable Company Multiples: Values the company basis revenue or EBITDA multiples of similar listed or recently funded peers.

- Net Asset Value (NAV): Based on the company’s book value of assets minus liabilities; typically applied for asset-heavy businesses.

The choice of methodology and its supporting assumptions must be defensible both to employees asking questions and to tax authorities examining records.

ESOP Tax Implications in India 2026: Two Points of Taxation

A frequently misunderstood aspect of ESOP tax implications in India is that employees are potentially taxed twice:

1: At Exercise Perquisite Tax

When an employee exercises their options, the spread between FMV and exercise price is treated as salary income (perquisite) and taxed at the employee’s applicable slab rate. For start up employees, where FMV may have grown significantly between the grant date and exercise date, this can result in a substantial tax liability even before a single share has been sold.

Budget 2020 introduced a deferred tax payment option for employees of eligible startups recognised by DPIIT, allowing this perquisite tax to be deferred up to 48 months from the exercise date, or until the employee leaves, or until the shares are sold whichever is earlier. Eligible employees should verify their employer’s DPIIT recognition status on the government’s startup portal.

2: At Sale : Capital Gains Tax

When the employee eventually sells the shares, the gain from sale price minus the FMV at exercise is treated as capital gain. If the shares have been held for more than 24 months (for unlisted company shares), the gains qualify as long-term capital gains, attracting a lower tax rate than short-term capital gains. For listed shares, the holding period threshold is 12 months.

Why a Well-Supported ESOP Valuation Protects Everyone

Dr. Haresh Adwani, PhD in Commerce and founding partner of Adwani & Co LLP, has consistently highlighted that in ESOP structuring, the valuation is not just a number it is a document of governance. A credible, independently prepared valuation:

- Gives employees a transparent, auditable basis for understanding the equity they receive.

- Helps the company comply with CBDT ESOP valuation rules and withholding tax obligations on perquisites.

- Strengthens the data room for the next funding round, where investors will scrutinise cap table and ESOP pool integrity.

- Reduces the risk of tax notices and disallowances arising from valuation disputes.

Key Takeaways

- ESOP valuation in India determines the perquisite tax an employee pays at the time of exercising options.

- For unlisted companies, FMV must be certified by a SEBI-registered Category I Merchant Banker as per Income Tax Rules.

- Employees of DPIIT-recognised startups may be eligible to defer ESOP perquisite tax by up to 48 months.

- Tax on ESOP arises at two stages: exercise (as perquisite/salary) and sale (as capital gain).

A defensible valuation report protects both the employee and the company during due diligence and tax assessments.

Read our detailed guide on Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Frequently Asked Questions on ESOP Valuation in India

Q1. What is the meaning of ESOP valuation in India and why does it affect my tax?

ESOP valuation determines the Fair Market Value (FMV) of your company’s shares at the time you exercise your options. The difference between FMV and your exercise price is taxed as a perquisite (salary income) under the Income Tax Act.

Q2. Who determines the ESOP valuation for unlisted companies in India?

As per Income Tax Rules, the FMV of shares of an unlisted company for ESOP purposes must be determined by a SEBI-registered Category I Merchant Banker. An informal or internally prepared valuation is not sufficient for tax compliance purposes.

Q3. Can ESOP perquisite tax be deferred for start up employees in India?

Yes. Employees of eligible startups recognised by DPIIT can defer the perquisite tax on ESOP exercise for up to 48 months from exercise, or until sale or separation whichever comes first. This benefit must be claimed correctly in the ITR.

Q4. At how many stages are ESOPs taxed in India?

ESOPs in India are potentially taxed at two stages: at exercise (the FMV-minus-exercise-price spread is taxed as salary/perquisite) and at sale (the profit from sale minus FMV at exercise is taxed as capital gains).

Q5. What ESOP valuation methods are used for start ups in India?

The most commonly applied ESOP valuation methods for unlisted Indian startups are the Discounted Cash Flow (DCF) method, Comparable Company Multiples, and the Net Asset Value (NAV) approach, with the choice depending on the company’s stage and business model.

Conclusion: The Valuation Behind the ESOP Is the Story

An ESOP is a promise of ownership. But the valuation behind that ESOP is a statement of how seriously a company takes its obligations to its employees, its investors, and the tax authorities who will eventually review the numbers.

In 2026, as ESOP culture deepens across India’s startup ecosystem, founders and CFOs who treat ESOP valuation as a compliance checkbox are taking an avoidable risk. And employees who accept ESOP grants without asking how the value was determined are leaving important questions unanswered.

The right question is not: ‘How many shares am I getting?’ It is: ‘How was this value determined, and what are my tax obligations when I exercise?’

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP

Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Get Expert Clarity on Your ESOP Valuation and Tax Obligations Whether you are a founder structuring an ESOP pool, an employee planning to exercise options, or a CFO managing ESOP compliance, visit itradvisor.in for authoritative, plain-language guidance on ESOP valuation in India, perquisite tax, and capital gains reporting.

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

Learn more about our Income Tax Filing Services for Traders & Investors covering ITR-3 filing, tax audit support under Section 44AB, F&O turnover calculation, and capital gains reconciliation with your broker’s statement.

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later

If you or someone you know has received a Section 148 income tax reassessment notice, do not panic but do act quickly and smartly. The law is on your side, provided you know where to look.

📞 Take Action Today

Need help evaluating whether your income tax reassessment notice is valid?

Connect with the experts at itradvisor.in for a detailed assessment of your notice, legal objection drafting, and end-to-end reply support. Visit: www.itradvisor.in | Powered by Adwani & Co LLP