Section 44AD & Balance Sheet

A creditor asked a small business client for a Balance Sheet. The client was filing under Section 44AD of the Income Tax Act. Legally, the client was compliant presumptive taxation scheme 44AD does not mandate maintaining traditional books of account for most small businesses. But commercially, the creditor still needed financial clarity before extending credit. This single situation reveals a gap that thousands of small business owners across India face: compliance relief under Section 44AD is not the same as financial awareness.

What Is Section 44AD and Who Qualifies for Presumptive Taxation in 2026?

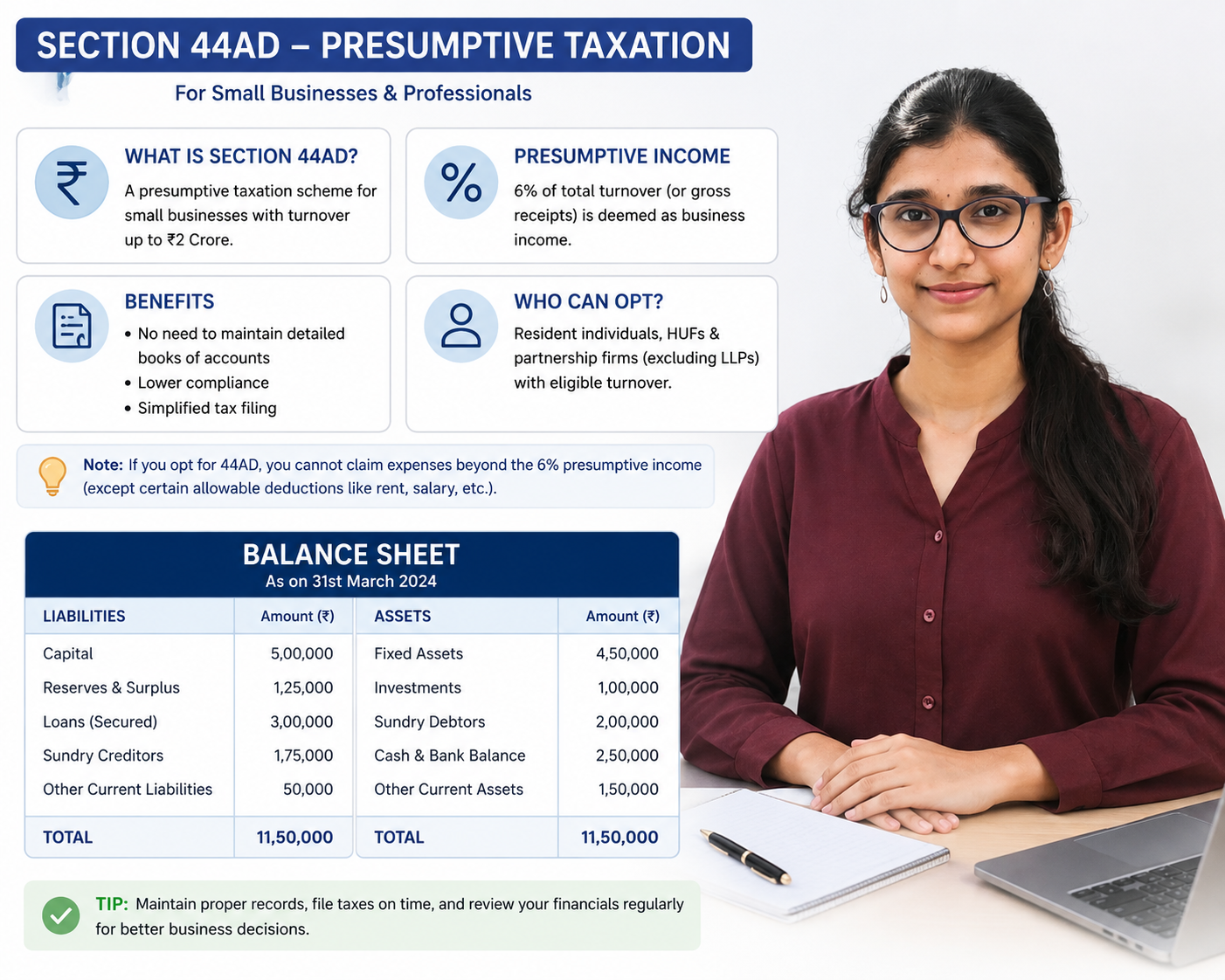

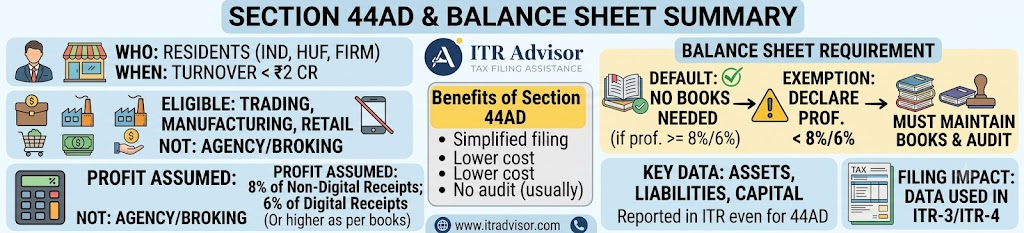

Section 44AD of the Income Tax Act, 1961 provides a presumptive taxation scheme for eligible small businesses with turnover up to ₹3 crore (subject to conditions on digital receipts). Under this scheme, a fixed percentage of gross receipts typically 8% (or 6% for digital transactions) is deemed as net profit, eliminating the need for detailed books and audit under Section 44AB.

Businesses opting for presumptive taxation 44AD in 2026 file their returns using ITR-4, making compliance significantly lighter compared to regular taxation. According to guidelines available on the Income Tax Department’s portal (incometax.gov.in), taxpayers under 44AD are exempt from the requirement to maintain books of account as prescribed under Section 44AA, provided they declare income at or above the presumptive rate.

Section 44AD and Balance Sheet: What the Law Says vs. What Reality Demands

Here is where business owners often misread the law. Section 44AD balance sheet requirement in India is not mandated by the Income Tax Act for compliant taxpayers under the presumptive scheme. However, that legal exemption does not mean a business can afford to operate without financial visibility.

The law can relax what you are required to maintain.

It cannot replace what you need to know.

Tax compliance keeps you on the right side of the law. Financial management helps you build something that lasts.

Creditors, banks, NBFCs, and even government tender processes routinely ask for a Balance Sheet to assess a business’s financial position regardless of which tax scheme the business uses. A Balance Sheet is, ultimately, a financial mirror of the business.

How to Address a Creditor’s Request When Filing Under Section 44AD

When a creditor or lender asks for a Balance Sheet from a Section 44AD taxpayer, there is a practical path forward even without formal accounts. The following documents together paint a coherent financial picture:

- ITR-4 Acknowledgement: Shows declared income, turnover, and tax paid a credible starting point.

- Computation of Income: Demonstrates the presumptive income calculation and net profit declared.

- Bank Statements & Reconciliation: Establishes actual cash flows, receipts, and business activity.

- GST Returns (GSTR-1 / GSTR-3B): Corroborates turnover independently through the GST portal (gst.gov.in).

- Outstanding Debtors / Creditors List: Provides a snapshot of working capital position.

Together, these documents substitute for a traditional Balance Sheet and satisfy most creditor due diligence requirements for small businesses under presumptive taxation 44AD 2026.

Why Financial Awareness Still Matters Under Section 44AD

As Dr. Haresh Adwani, PhD in Commerce and legal expert, often emphasizes in his advisory practice: a business owner may not be legally required to maintain books under 44AD, but the absence of records does not eliminate financial risk. Every business regardless of its tax scheme should have clarity on:

- Total assets and liabilities at any point in time

- Outstanding loans, dues, and repayment obligations

- Borrowing capacity and working capital health

- Cash flow patterns across quarters

- Whether the business can sustain itself through a lean period

These are not audit questions. They are survival questions. Businesses that track these numbers even informally are far better positioned to negotiate credit, handle disputes, and scale sustainably.

Key Takeaways: Section 44AD, Balance Sheet & Financial Management

1. Section 44AD exempts eligible small businesses from maintaining books of account under Section 44AA.

2. This exemption applies to Income Tax compliance not to commercial or credit requirements.

3. Creditors, banks, and NBFCs may still require a Balance Sheet or equivalent financial documentation.

4. ITR-4, bank statements, GST returns, and income computation can together address creditor queries.

5. Financial awareness knowing your assets, liabilities, and cash flows is essential regardless of tax scheme. 6. Presumptive taxation 44AD in 2026 is a compliance simplification, not a substitute for sound financial management.

Read our detailed guide on Presumptive Taxation Scheme: Section 44AD & 44ADA Explained Also read: 10 Common ITR Filing Errors That Can Trigger Income Tax Notices in 2026

Frequently Asked Questions

Q1. Is a Balance Sheet mandatory for businesses filing under Section 44AD?

No, the Income Tax Act does not mandate a formal Balance Sheet for taxpayers complying under Section 44AD. However, creditors, banks, and other third parties may still require financial statements independently of your tax compliance.

Q2. Can a Section 44AD taxpayer get a bank loan without a Balance Sheet?

Yes, in many cases. Bank reconciliations, ITR-4, GST returns, and computation of income together can satisfy lender requirements. Some banks have specific assessment frameworks for presumptive taxation filers.

Q3. What is the turnover limit under Section 44AD in 2026?

The turnover limit under Section 44AD is ₹3 crore for AY 2026-27, provided at least 95% of receipts and payments are through digital modes. For cash-heavy businesses, the limit is ₹2 crore.

Q4. What happens if a Section 44AD taxpayer does not declare the presumptive income correctly?

If declared income falls below the presumptive rate, the taxpayer must maintain books of account and get them audited under Section 44AB. Additionally, they may be barred from re-opting for 44AD for the next five assessment years.

Q5. Does opting for presumptive taxation 44AD affect a business’s credit eligibility?

It can, indirectly. Since formal Balance Sheets are not required, lenders may request alternative documents. A well-maintained record of bank statements and GST returns significantly improves credit assessment outcomes for 44AD businesses.

Conclusion

Section 44AD is one of the most taxpayer-friendly provisions in Indian tax law and rightly so. It dramatically reduces the compliance burden for small businesses and makes ITR-4 filing accessible to millions who might otherwise struggle with detailed accounts.

But here is what every small business owner must internalise: compliance is the floor, not the ceiling. Filing under presumptive taxation 44AD in 2026 keeps you legally protected. Understanding your Balance Sheet your assets, your liabilities, your financial position keeps your business commercially strong. The two must coexist.

About the Author : Shreya Kavitke

Shreya Kavitke is a CA Finalist and an Article Assistant at Adwani & Co. LLP, where she works across diverse areas of taxation, accounting, and regulatory compliance. With a strong academic foundation in commerce and practical exposure to advisory and compliance engagements, she contributes to research and analysis on evolving tax and business regulations.

Her areas of interest include direct taxation, Goods and Services Tax (GST), corporate compliance, and financial reporting.

At ITRadvisor, Shreya contributes articles that combine technical accuracy with practical applicability, helping readers stay informed about key tax developments, compliance obligations, and emerging regulatory trends. She believes that clear, reliable, and timely guidance is essential to navigating today’s dynamic tax environment.

This version reflects the polished, research oriented tone commonly found in publications by leading professional services firms while remaining authentic to Shreya’s current role and experience.

Want clarity on Section 44AD, ITR-4 filing, or how to present your financials to creditors? Visit ITRAdvisor.in for expert-reviewed tax guidance, practical tools, and authoritative content designed for small business owners across India. Stay compliant. Stay financially aware.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

A prominent “File Your ITR Now” button near the top and again at the end of the article

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.

Leave a Reply