AI ITR Filing 2026

Everyone is asking whether AI can prepare income tax returns. Barely anyone is asking the more important question: who will defend the tax position behind them?

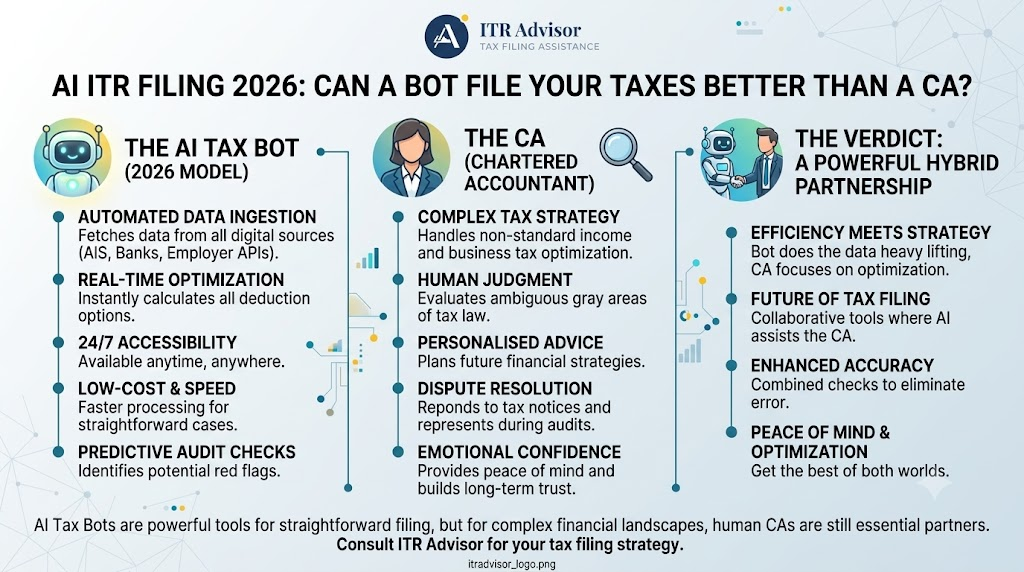

AI ITR filing tools in 2026 are genuinely impressive. They extract data from Form 16 and AIS, pre-populate schedules, flag mismatches with Form 26AS, and generate a draft return faster than any manual process. But here is what they cannot do: determine whether your tax position will hold up if the Income Tax Department sends a notice.

That gap between a technically filed return and a defensible one is exactly what taxpayers need to understand before trusting AI completely with their compliance.

What AI ITR Filing Tools Actually Do Well in 2026

To be fair, AI-assisted tax filing has made meaningful improvements to routine compliance. For straightforward salaried taxpayers with a single employer, Form 16, and standard deductions, AI tools deliver speed and accuracy that was difficult to match manually.

What AI handles reliably in ITR filing 2026:

- Auto-fetching pre-filled data from the Income Tax Department’s AIS and Form 26AS

- Matching TDS credits with Form 26AS entries to reduce demand notices on mismatch

- Suggesting the correct ITR form based on income type — ITR-1, ITR-2, or ITR-4

- Computing tax liability under both old and new tax regime and flagging which is lower

- Identifying obvious gaps such as a missing TDS entry or an unreported interest income item

These are real productivity gains. For a quick overview of which ITR form applies to your income profile, read our ITR-1 vs ITR-2 vs ITR-4 guide for AY 2026-27.

Where AI ITR Filing Fails: The Reasoning Problem

Tax risk in India rarely comes from a data extraction error. It comes from reasoning and reasoning is exactly where AI-generated tax returns have a structural gap.

Consider a taxpayer who claims a tax benefit. The numbers are correct. Every document is available. The return passes all system validation checks on the Income Tax Department’s e-filing portal. Yet the questions that matter most remain unanswered:

Questions AI Cannot Answer for Your ITR

→ Is the taxpayer actually eligible for this exemption or deduction?

→ Does a restriction, limitation, or anti-avoidance provision apply?

→ Is there a more advantageous tax position that has not been explored?

→ If the Income Tax Department issues a notice under Section 143(2) or 148, can the position be defended?

These are not rare edge cases. They arise in everyday situations F&O loss set-off against business income, HRA claims without proper rent documentation, deductions under Section 80C with incomplete evidence, or capital gains on equity funds where the holding period is borderline.

The Income Tax Department’s faceless assessment scheme and AI-driven scrutiny systems are specifically designed to catch reasoning inconsistencies not just arithmetic ones. Returns are risk-scored using cross-database matching of ITR data, AIS, GST turnover, MCA filings, and banking transactions. A return that is numerically clean but logically inconsistent across these sources remains a scrutiny risk.

A Real Example: When AI Filed Correctly but Wrongly

Practical Scenario

A freelancer with annual professional receipts of ₹18 lakh used an AI ITR filing tool for AY 2026-27.

The AI correctly:

• Selected ITR-4 (presumptive taxation under Section 44ADA)

• Applied the 50% deemed profit rate declaring ₹9 lakh as income

• Computed tax liability accurately under the new tax regime

What the AI did not evaluate:

• Whether the freelancer had claimed actual expenses exceeding the 50% deemed amount in a prior year, which triggers an obligation to maintain books of account

• Whether certain receipts were from a source that does not qualify under Section 44ADA

Result: The return was filed. But when a scrutiny notice arrived under Section 143(2) querying the presumptive scheme eligibility, there was no documentation trail to support the position. A professional review before filing would have flagged both risks in minutes.

AI ITR Filing 2026 and the Income Tax Notice Risk

As per guidance available through the Income Tax Department’s portal (incometax.gov.in) and CBDT’s risk management framework, cases are increasingly selected for scrutiny based on risk indicators not just mismatches. These indicators include unusual deduction patterns, turnover inconsistencies between ITR and GST returns, and high value transaction disclosures in AIS that do not align with reported income.

In that environment, AI ITR filing 2026 tools create a specific risk: they improve the presentation of a return without improving the underlying defensibility of its positions. A well-formatted, AI-generated return is not automatically a safe return.

This is the reasoning-versus-calculation distinction that tax professionals have been discussing since AI tools entered mainstream compliance and it is the most practically important thing a taxpayer in 2026 needs to understand.

For a detailed breakdown of what triggers income tax notices and how to respond,

read our Explore the Old vs New Tax Regime Comparison 2026

Key Takeaways

What Every Taxpayer Should Remember About AI ITR Filing in 2026

✔ AI ITR filing tools handle data extraction, form selection, and computation well especially for straightforward salaried returns.

✔ The gap is in reasoning: eligibility assessment, deduction defensibility, and position validation.

✔ The Income Tax Department’s faceless assessment and AI-driven risk-scoring evaluate logical consistency not just arithmetic.

✔ Treating an AI-generated ITR as a first draft subject to professional review is the smart approach.

✔ For any non-standard income F&O losses, capital gains, presumptive scheme, foreign income professional review before filing is essential.

Frequently Asked Questions

1. Can AI tools file income tax returns accurately in 2026?

For simple salary-based returns, yes AI tools perform well. For returns involving business income, capital gains, foreign assets, or multiple deduction claims, professional review is strongly recommended before filing.

2. What is the risk of relying only on AI for ITR filing?

The main risk is a reasoning gap AI applies rules mechanically without evaluating whether a specific position is eligible, defensible, or optimal for your situation. This can lead to income tax notices that are difficult to respond to without prior documentation.

3. Does AI ITR filing increase the chance of getting an income tax notice?

Not directly but an AI-filed return that contains an indefensible position is a scrutiny risk regardless of how cleanly it was prepared. The Income Tax Department’s risk-scoring evaluates logical consistency across AIS, GST, and MCA data, not just the arithmetic of the return.

4. Which ITR form should I use for AY 2026-27?

It depends on your income type. ITR-1 is for salaried taxpayers with income up to ₹50 lakh. ITR-2 covers capital gains and multiple properties. ITR-4 applies to presumptive income under Sections 44AD and 44ADA. Read our detailed ITR form selection guide for AY 2026-27 on ITRAdvisor.in.

5. What will be the most valuable tax skill in an AI-driven compliance world?

According to tax professionals including those at Adwani & Co LLP, the highest-value skill will be validating conclusions not just preparing returns. The ability to evaluate whether an AI-generated tax position is legally defensible, commercially reasonable, and consistent with regulatory expectations is what separates a capable tax advisor from a filing service.

Conclusion: AI Is a Tool. Judgment Is the Profession.

AI ITR filing in 2026 is fast, efficient, and accurate on the mechanical layer of compliance. It reduces data entry errors, speeds up return preparation, and makes basic tax filing accessible to a broader audience.

But the most expensive mistakes in taxation are rarely calculation errors. They are reasoning errors wrong eligibility assessments, indefensible deduction claims, and positions that cannot withstand scrutiny. That is where a qualified tax professional still makes the difference that cannot be automated.

The smart approach is not to choose between AI and professional review. It is to use AI for what it does well and ensure a professional reviews what it cannot.

Author

CA. Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services.

Whether you have already received a credit card income tax notice or want to ensure you never do Adwani and Company is your trusted partner. Led by Dr. Haresh Adwani and a seasoned team of Chartered Accountants, Adwani and Company provides end-to-end income tax compliance, notice response, and financial planning services.

Get Expert Tax Guidance

If you want to file your ITR accurately and defend it confidently visit ITRAdvisor.in today.

From ITR form selection and tax regime comparison to notice response and professional review, ITRAdvisor.in gives you the tax knowledge you need to stay compliant and avoid costly mistakes

Visit: ITRAdvisor.in

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform.

The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

© 2026 ITRAdvisor.in. All rights reserved.