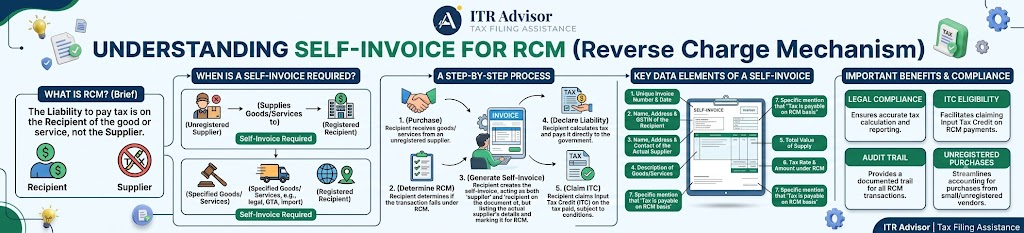

You paid GST under Reverse Charge Mechanism (RCM) on time. Good. But did you also issue a self-invoice for that RCM transaction? If not, your ITC claim and your audit file may already be at risk.

Many businesses treat RCM as a payment obligation and stop there. In reality, a self-invoice for RCM is a separate, mandatory document and skipping it is one of the most common GST compliance gaps we see at ITRAdvisor.in.

What Is a Self-Invoice for RCM?

Under Section 31(3)(f) of the CGST Act, when a registered person receives taxable goods or services from an unregistered supplier and is liable to pay GST under RCM, the recipient not the supplier must issue the invoice. This is the self-invoice for RCM. It exists because an unregistered supplier cannot legally issue a GST-compliant tax invoice, so the law shifts that responsibility to you.

Why the Self-Invoice for RCM Actually Matters

It supports the GST you paid in cash under RCM.

Without it, you cannot claim ITC on that RCM payment under Rule 36(1)(b).

It strengthens your documentation trail during GST audits and scrutiny.

It closes a gap officers routinely check, since RCM leaves no supplier-side trail.

The 30-Day Deadline Most Businesses Miss

Since Rule 47A took effect on 1st November 2024, a self-invoice for RCM must be issued within 30 days of receiving the goods or services not at month-end, and not whenever convenient. Miss this window and you risk interest on delayed tax and penalty exposure under Section 122, on top of ITC disputes.

The self-invoice must also be reported in Table 13 of GSTR-1, paired with a payment voucher under Section 31(3)(g) when payment is actually made to the unregistered supplier.

Common Self-Invoicing Mistakes Under RCM

Paying RCM tax correctly but never generating the self-invoice.

Issuing it weeks late, well outside the 30-day window.

Not labelling it clearly as a self-billed invoice.

Forgetting the accompanying payment voucher.

Key Takeaways

A self-invoice for RCM is mandatory under Section 31(3)(f) whenever you buy from an unregistered supplier under reverse charge.

You must issue it within 30 days of receipt, under Rule 47A.

No self-invoice generally means no valid ITC claim on that RCM payment.

Frequently Asked Questions on Self-Invoice for RCM

1. Is a self-invoice for RCM always required?

Yes, whenever you’re liable to pay GST under RCM on a supply from an unregistered supplier.

2. What happens if I don’t issue a self-invoice for RCM?

You may lose your ITC claim on that RCM payment and face questions during a GST audit.

3. What is the deadline to issue a self-invoice under RCM?

Within 30 days of receipt, as mandated by Rule 47A effective 1st November 2024.

4. Is a payment voucher the same as a self-invoice?

No. The self-invoice records the supply; the payment voucher separately records the payment.

Conclusion: Don’t Let Paperwork Undo Correct Tax Payment

Paying GST under RCM is only half the compliance story. Issuing a proper, timely self-invoice for RCM is what protects your ITC, your audit trail, and your peace of mind. As Dr. Haresh Adwani, founding expert at Adwani & Co LLP, often points out, GST compliance is not just about depositing tax it is about proving that tax was correctly deposited, with the right document, at the right time.

Learn more about our GST Compliance Checklist 2026, or read our detailed guide on GST Input Tax Credit Rules 2026.

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

Opened your inbox to find an Income Tax Department email asking you to “explain a discrepancy” before you have even filed your return? It happens to thousands of salaried taxpayers every season, and it almost always traces back to one document: the Annual Information Statement, or AIS. If the numbers in your AIS do not match what you are about to declare in your ITR, you are not just risking a delayed refund you are inviting a AIS notice. This guide walks you through exactly how AIS notices ITR filing AY 2026-27 cases arise, and the precise steps salaried taxpayers should take to avoid one before they even click submit.

What Is the AIS and Why It Decides Whether You Get a Notice

The Annual Information Statement is a consolidated financial profile that the Income Tax Department builds for every PAN, pulling data directly from your employer, banks, mutual fund houses, stock brokers, and registrars. It covers salary, interest income, dividends, securities transactions, and high-value spends essentially everything the department already knows about you before you file a single form.

Many taxpayers assume AIS is the same as Form 26AS. It is not. Form 26AS captures only TDS and TCS entries, while AIS is far broader and includes the underlying transaction data itself. Understanding the Form 26AS vs AIS difference 2026 is the first step toward a clean filing, because the department’s automated systems cross-check your ITR against both.

How an AIS Mismatch Turns Into an Income Tax Notice

When the income you declare in your ITR does not align with what AIS already shows, the system does not wait for a human officer to notice. Risk-based automated matching flags the gap almost instantly, and the most common outcome is a notice under the e-Verification Scheme or a query under Section 143(1)(a), asking you to reconcile the difference or file a revised return.

For salaried employees, the usual triggers are surprisingly routine: a mid-year salary revision your employer reported differently, interest income from a savings account or fixed deposit you forgot to add, dividend income that slipped through, or capital gains on mutual funds that were not separately declared. None of these are deliberate evasion but to an automated matching engine, unexplained is indistinguishable from undisclosed.

Step-by-Step: How to Avoid an AIS Notice Before You File

1. Download and Reconcile, Don’t Skip

Log in to the income tax e-filing portal, open the AIS module, and download both the AIS and the Taxpayer Information Summary (TIS). Compare every line item against your Form 16, salary slips, bank interest certificates, and capital gains statements before you touch the ITR form.

2. Submit Feedback on Every Incorrect Entry

If an entry in AIS is wrong, duplicated, or simply does not belong to you, use the “Add Feedback” option against that specific transaction. This creates a documented trail showing you proactively flagged the discrepancy a detail that matters enormously if a notice does arrive later.

3. File With the Correct Figures, Not Just the Pre-Filled Ones

Submitting AIS feedback alone does not change your ITR. You still need to file your return using the figures you believe are accurate, supported by your own documentation, even while the feedback is under review.

4. Re-Check Closer to the Deadline

AIS data is dynamic and keeps updating as employers and banks file revised TDS returns. A statement downloaded in April can look materially different by late May or June, so re-verify shortly before you actually file.

Expert InsightAccording to Dr. Haresh Adwani, tax advisory expert and a key voice behind Adwani & Co LLP’s compliance practice, the single biggest reason salaried taxpayers receive AIS-driven notices is not concealment it is simply filing too early, before banks and employers have finished updating their reported data for the year.

What Happens If You Already Filed and Then Spot a Mismatch

If you have already submitted your return and later notice an AIS discrepancy, a belated or revised return is usually the cleanest fix, provided it is filed within the applicable timelines specified by the Income Tax Department. Acting before a formal notice lands is always preferable to responding after one does.

Key Takeaways

AIS is broader than Form 26AS and drives most automated notices. Always reconcile AIS and TIS against your own documents before filing. Submit feedback on incorrect entries and file with verified figures. Re-check AIS closer to your filing date since data updates continuously.

Frequently Asked Questions

Q1. What triggers an AIS mismatch notice for salaried employees?

Unreported interest, dividend, or capital gains income, or salary figures that differ from employer-reported data, are the most common triggers. The system flags any unexplained gap automatically.

Q2. Is Form 26AS the same as AIS?

No. Form 26AS shows only TDS/TCS data, while AIS covers a much wider range of income and transaction details reported by third parties.

Q3. Can I correct a wrong entry in my AIS before filing?

Yes, you can submit feedback against any incorrect or duplicate entry directly on the AIS portal, which creates a record of your objection.

Q4. Does submitting AIS feedback automatically update my ITR?

No. Feedback only flags the entry for review; you must still file your return using the figures you believe are correct.

Q5. What should I do if I get a notice despite reconciling AIS?

Respond within the stated timeline with supporting documents such as Form 16, bank certificates, and your AIS feedback trail, or seek professional guidance promptly.

Conclusion:

An AIS notice rarely means you did something wrong it usually means a data point somewhere was never reconciled. With AY 2026-27 filings now in motion, the safest strategy for any salaried taxpayer is simple: download your AIS, match it line by line against your real records, fix what is wrong, and only then file. That single habit prevents the vast majority of notices before they are ever issued.

If you want expert guidance on reconciling your AIS or responding to an AIS notice, connect with itradvisor.in today and file your AY 2026-27 return with complete confidence.

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

If You Think Filing a Salary ITR Is Still Simple, This Will Change Your Mind

Picture this: You are a salaried professional. You earn well. Your company’s payroll team handles your TDS every month. You get your Form 16 in June, hand it to a local accountant or plug it into an online portal, file your return in twenty minutes, and go on with your life.

Two months later, you receive an Income Tax Department notice asking why your ITR does not match your Annual Information Statement.

You had no idea your FD interest was being reported. You forgot about the mutual funds you redeemed last October. You did not realise your credit card spend pattern was flagged for inconsistency with your declared income.

This scenario is playing out across India for AY 2026-27 and it is happening to careful, responsible, tax-compliant salaried professionals who simply did not know how much the system had changed.

ITR filing for salaried employees today is a sophisticated exercise. At ITR Advisor, our tax professionals work with employees across every sector IT, banking, healthcare, manufacturing, government to ensure their income tax returns are filed with the accuracy, completeness, and professional review that modern compliance demands.

This guide breaks down everything you need to know the risks, the right process, the expert advantage, and how to make sure AY 2026-27 is the year you file without a single worry.

How Income Tax Return Filing for SmartestSalaried Employees Has Changed in AY 2026-27

The Income Tax Department, through guidelines and compliance frameworks published on its official portal www.incometax.gov.in, has steadily built one of the most comprehensive taxpayer surveillance systems in Asia. Today, the department receives financial data from:

All scheduled banks (interest, cash deposits, high-value transfers)

SEBI-registered stock brokers and depositories (equity trades, LTCG, STCG)

Mutual fund registrars (SIP redemptions, fund switches, dividend payouts)

Post offices and NBFCs (recurring deposits, interest income)

Property registrars (real estate purchases and sales)

Every piece of this data is compiled into your Annual Information Statement (AIS) a financial fingerprint of your entire year. The Income Tax Department’s processing systems then compare your AIS against your filed ITR. Any gap between the two is a mismatch and mismatches generate notices.

This is the environment in which ITR filing for salaried employees in AY 2026-27 is happening. The era of filing using only Form 16 is over.

The 8 Costliest Mistakes SmartestSalaried Employees Make in ITR Filing And How to Avoid Them

Understanding the common failure points is the first step toward getting your return right.

1. Treating Form 16 as the Complete Picture

Form 16 is your salary TDS certificate nothing more. It captures what your employer paid you and the tax deducted at source. It does not capture:

Interest income from savings accounts, FDs, or RDs

Dividend received from shares or mutual funds

Capital gains from equity sales or MF redemptions

Rental income

Freelance or consulting income

Foreign salary or perquisites

If these are in your AIS but absent from your ITR, a notice will follow.

2. Filing the Wrong ITR Form

This is more common than most taxpayers realise. Every year, thousands of Smartest salaried employees file ITR-1 when they should have filed ITR-2 simply because they did not account for their capital gains, foreign assets, or multiple income sources.

ITR-1: Salary income below ₹50 lakh, one house property, no capital gains, no foreign assets

ITR-2: Capital gains from any source, two or more house properties, foreign assets or income, NRI status

ITR-3: Business or professional income alongside salary

Filing the wrong form triggers a Section 139(9) defective return notice and requires you to refile. This also delays any pending refund.

3.Skipping the Old vs New Tax Regime Comparision

The tax regime decision is one of the highest-impact choices in your entire return. Yet most salaried employees either stay with what their employer assumed or choose based on incomplete information.

Real Example:

Anil, a 38-year-old banker in Pune earning ₹22 lakh annually, had his employer default him to the new tax regime. His total tax liability under the new regime: ₹2,92,500. When his tax consultant ran the old regime calculation factoring in ₹1.5 lakh under Section 80C, ₹50,000 NPS contribution under 80CCD(1B), ₹25,000 health insurance under 80D, and ₹3.6 lakh HRA exemption his liability dropped to ₹2,24,200. He was unknowingly overpaying ₹68,300 every year. A single professional review corrected this permanently.

4. Not Reporting Capital Gains from SIPs and Stock Trading

India’s investor base has exploded. Millions of salaried employees now have active portfolios on platforms like Zerodha, Groww, Angel One, and Kite many of whom do not realise that every redemption, switch, or sale is a taxable event.

Short-term capital gains (STCG) from equity mutual funds are taxed at 20%. Long-term capital gains (LTCG) above ₹1.25 lakh are taxed at 12.5%. Both must be reported along with your cost of acquisition, date of purchase, and date of sale.

Your AMC or broker provides a capital gains statement. If you are filing without one, your return is almost certainly incomplete.

5.Missing Interest Income from All Bank Accounts

Most salaried professionals have more bank accounts than they actively manage a salary account, a savings account from a previous employer, an old joint account with a parent, an RD opened years ago. Each of these reports interest to the Income Tax Department. Each of these appears in your AIS.

Missing any one of them creates a mismatch.

Pro tip: Before filing, download your AIS from the income tax portal and create a checklist of every interest entry. Cross-check against your actual bank records. If an entry is incorrect, raise feedback on the portal before filing.

6. Incorrect or Undocumented HRA Claims

HRA (House Rent Allowance) is one of the most commonly claimed and most commonly scrutinised exemptions in salary ITR filing. Issues arise when:

Rent is paid to a parent but no proper rent agreement exists

Rent exceeds ₹1 lakh annually but the landlord’s PAN was not furnished to the employer

HRA is claimed in the ITR but the employer’s Form 16 does not reflect it (regime mismatch)

The Income Tax Department has the ability to cross-verify HRA claims through property registration data and landlord PAN records. Claims without documentation are a scrutiny risk.

7. Ignoring Crypto and Digital Asset Transactions

Virtual Digital Assets (VDAs), including cryptocurrency, are taxable at a flat 30% under Section 115BBH. Losses from crypto cannot be set off against any other income. TDS at 1% applies on certain transactions.

If you transacted in crypto during FY 2025-26, it must be disclosed in your ITR regardless of whether you made a profit. Ignoring it when your exchange has reported transactions in AIS is a serious compliance risk.

8 . Selecting the Wrong Bank Account for Refund Credit

A surprisingly common issue: taxpayers enter an old or inactive bank account for refund credit. The refund fails, and the taxpayer does not realise it for months. Always verify that your bank account is pre-validated on the income tax portal and linked to your PAN before submitting your return.

Who Absolutely Must File an Income Tax Return in AY 2026-27

While most salaried employees with income above the basic exemption limit are required to file, the Income Tax Act also mandates ITR filing based on certain activities regardless of taxable income. As per the department’s provisions, you must file even if your income is below the exemption limit if:

You have deposited more than ₹1 crore in bank accounts during the year

You have spent more than ₹2 lakh on foreign travel

You have paid more than ₹1 lakh in electricity bills

You hold foreign assets or have signing authority over foreign accounts

You have received income from property located abroad

Your aggregate TDS and TCS deductions exceed ₹25,000

Additionally, filing ITR even when not strictly required creates a verified income record that is essential for home loans, personal loans, visa applications, and financial planning.

Expert ITR Filing for Special Categories of Salaried Employees

ITR Filing for Government Employees and PSU Staff

Government employees and public sector staff often have additional income sources such as arrears (with relief under Section 89), pension, gratuity, leave encashment, and LTC. Each of these has specific treatment under the Income Tax Act. Incorrect handling of arrear relief, in particular, frequently results in excess tax payment that could have been avoided.

ITR Filing for Doctors, Engineers, and Consultants with Dual Income

Many salaried professionals doctors, architects, engineers also earn consulting or professional fees alongside their primary salary. This dual income profile requires careful handling: the consulting income may need to be reported under “Profits and Gains from Business or Profession,” and the correct ITR form (usually ITR-3) must be selected.

At ITR Advisor, our experts handle combined salary-plus-profession returns with full accuracy and proper schedule completion.

NRI Income Tax Return Filing for Indians Working Abroad

For Non-Resident Indians earning from Indian sources rental income, NRO account interest, Indian equity investments, or salary credited to Indian accounts NRI income tax return filing is mandatory when income exceeds the basic exemption limit.

The residential status determination (NRI vs RNOR vs Resident) is critical and must be based on days of physical presence in India. DTAA benefits, if applicable, must be claimed correctly using Form 67 where foreign taxes have been paid.

The Real Value of Filing Your ITR on Time : Beyond Just Compliance

Timely income tax return filing for salaried employees delivers benefits that go well beyond avoiding penalties:

Financial Documentation: ITR is the most widely accepted income proof for home loans, vehicle loans, and personal finance applications. Most banks require the last 2–3 years’ ITRs for loan processing.

Visa Applications: Several countries including the US, UK, Canada, and Schengen zone nations require ITR documents as part of visa income proof requirements.

Carry Forward of Losses: Capital losses (from equity, MFs, or property) can only be carried forward to offset future gains if the return is filed on time. A belated return forfeits this benefit.

Faster Refund Processing: Returns filed early in the season are typically processed sooner. Late filers often experience longer refund wait times as system loads increase.

Avoiding Compounding Interest: Late filing on a return with tax payable results in interest under Sections 234A, 234B, and 234C which compounds monthly and can add significantly to your total tax cost.

Why ITR Advisor Is the Right Choice for Smartest Salaried Employees Your Income Tax Return Filing in AY 2026-27

At ITR Advisor, we do not just enter numbers into a form. We bring professional tax expertise to every return we handle.

Here is what sets our expert ITR filing service apart:

Complete AIS and Form 26AS Reconciliation : We review every entry in your AIS before filing and ensure your return reflects a fully reconciled picture.

Regime Optimisation : We run a proper old vs new tax regime comparison for your specific income and deduction profile, ensuring you pay the least tax legally possible.

Capital Gains Accuracy : We calculate STCG and LTCG across equity, mutual funds, ESOPs, and property using your actual transaction statements.

Notice Risk Assessment : We proactively identify entries in your AIS that could trigger scrutiny and ensure proper disclosure and documentation before submission.

Post-Filing Support : If a notice or intimation arrives after filing, our team handles the response, revision, and compliance follow-through.Pan-India Digital Service We serve clients across Pune, Mumbai, Delhi, Bengaluru, Hyderabad, Chennai, and every corner of India through a fully secure digital filing process

Frequently Asked Questions

Q1. What is the last date to file salary ITR for AY 2026-27?

The standard due date for salaried employees is 31st July 2026. Belated returns can be filed up to 31st December 2026 with a late fee. Filing before the due date is always advisable to preserve all tax benefits, carry-forward rights, and timely refund processing.

Q2. Can I file ITR for salaried income without a CA?

Yes, but the risk of errors increases significantly when your income involves capital gains, foreign assets, RSUs, crypto, or multiple employers. Expert-assisted filing ensures accuracy, AIS reconciliation, and proper regime selection — reducing notice risk substantially.

Q3. How long does expert ITR filing take with ITR Advisor?

Simple salary returns are typically processed within 1–2 business days of receiving all required documents. Returns with capital gains, RSUs, or foreign income may take 2–4 business days depending on the complexity.

Q4. What if I received two Form 16s from different employers in the same year?

Both employers’ salary and TDS details must be consolidated in a single ITR. Failing to do so results in incomplete disclosure and a likely mismatch notice. This is a common situation for employees who switched jobs and requires careful aggregation of income and TDS credits.

Q5. Is capital gains from selling ancestral property taxable for salaried employees?

Yes. Capital gains from property sale — including inherited or ancestral property — are taxable. The cost of acquisition for inherited property is determined by its fair market value as of April 1, 2001. LTCG from property is taxed at 12.5% without indexation benefit (post-July 2024 amendments). Professional calculation is strongly recommended.

Q6. Do I need to show my PPF maturity amount in ITR?

PPF maturity proceeds are fully exempt from income tax. However, if the amount appears in your AIS, it is good practice to show it in the exempt income schedule of your ITR to prevent any potential mismatch query.

Q7. What is the penalty for filing an incorrect ITR?

Under Section 270A, under-reporting of income can attract a penalty of 50% of the tax on under-reported income. Misreporting (with intent) can result in a penalty of 200% of such tax. Accurate and complete filing is always the safer and smarter path.

Conclusion

Tax compliance in India has entered a new era. The gap between “filing a return” and “filing a correct and complete return” has never been wider and the consequences of that gap have never been more serious.

For Smartest Salaried Employees across India, ITR filing for AY 2026-27 demands a professional, systematic approach: reviewing AIS, comparing tax regimes, reporting every income source, documenting every deduction, and ensuring that what you submit aligns with what the Income Tax Department already knows.

The cost of getting it right the first time in time, money, and professional fees is a fraction of the cost of responding to a notice, revising a return, or managing a tax demand.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

A prominent “File Your ITR Now” button near the top and again at the end of the article

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.

ITR Advisor is here to make sure you get it right. Connect with our tax experts today for complete, accurate, and worry-free salary ITR filing for AY 2026-27.

A return takes fifteen minutes to file. Fixing one of the wrong ITR filing mistakes hiding inside it can take fifteen months. That gap between speed and consequence is exactly why taxpayers who file “on time” still end up facing an income tax notice they never saw coming.

Why ITR Filing Mistakes Go Unnoticed at First

Filing successfully and filing correctly aren’t the same thing. The portal checks the format of your submission not whether every figure matches what the department already knows. That is why ITR filing mistakes often surface weeks later, not on the day you submit.

A Quick Case: One Missed Entry, Months of Follow-Up

In a case reviewed recently, a taxpayer assumed the return was accurate simply because it had been accepted. The issue was small: income from one source wasn’t reported correctly. A notice followed, interest kept climbing, and the refund was held back while explanations went back and forth for months. In high-value cases, this kind of gap can turn into a tax demand running into lakhs or even crores.

The Five Checks That Prevent Most ITR Filing Mistakes

Before you click “Submit,” run through these checks — they catch the majority of ITR filing mistakes before they become an income tax notice:

Is every source of income reported, not just the obvious ones?

Have you picked the correct ITR form for your income type?

Are your deductions backed by documents you can actually produce?

Does your return match your AIS and Form 26AS, line by line?

Have you disclosed capital gains, foreign assets, or other reportable income, where applicable?

Form 26AS vs AIS: Why This Match Matters Most

Most income tax notices in 2026 trace back to one root cause: a mismatch between your filed return and your Form 26AS vs AIS data already on record. The Income Tax Department’s e-filing portal makes both statements available before filing, so reconciling them isn’t optional it’s the single highest-leverage check you can make.

How Quickly Can an ITR Filing Mistake Become a Notice?

Faster than most taxpayers expect. Once a mismatch is flagged, a notice can follow within the prescribed income tax notice time limit, and interest typically accrues from the point the shortfall existed not from the date the notice was issued.

Key Takeaway

ITR filing mistakes are rarely about dishonesty they’re almost always about a missed reconciliation step. Matching your return against your AIS and Form 26AS before submission remains the single most effective way to avoid an income tax notice altogether.

Getting Expert Eyes on Your Return

As Dr. Haresh Adwani, a Commerce Ph.D. holder and law graduate who frequently reviews such cases, notes most income tax notices are preventable with a thirty-minute reconciliation, not a thirty-day reply after the fact.

Read our detailed guide Salary vs AIS Mismatch in Your ITR : Dangerous, Common & Completely Fixable

Frequently Asked Questions

What is the most common ITR filing mistake?

Unreported income that already appears in your AIS or Form 26AS is the single most common trigger for a notice.

How long does the department have to send an income tax notice?

It depends on the type of notice and assessment year, but reassessment notices can be issued well within the prescribed income tax notice time limit — don’t assume an old return is automatically safe.

Can I fix an ITR filing mistake after submission?

Yes, a revised return is usually possible before the applicable deadline; after a notice is issued, a documented reply becomes necessary instead.

Does choosing the wrong ITR form count as a mistake?

Yes — filing under the wrong form is treated as a defective return and can independently trigger departmental queries.

Conclusion: Review Before You Submit, Not After You’re Notified

Filing fast feels productive, but ITR filing mistakes don’t announce themselves at the time of submission they surface later, as an income tax notice, a frozen refund, or months of correspondence. A few extra minutes of reconciliation today is consistently cheaper than the months it takes to undo a mismatch tomorrow.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

Not Sure If Your Return Is Clean? If you’re unsure whether your return has been reported correctly, a quick review today can help avoid a much bigger problem later. If you want expert guidance, connect with itradvisor.in today.

Here Is Your Definitive 2026 Survival Guide: Know Your Rights, Protect Your Wealth

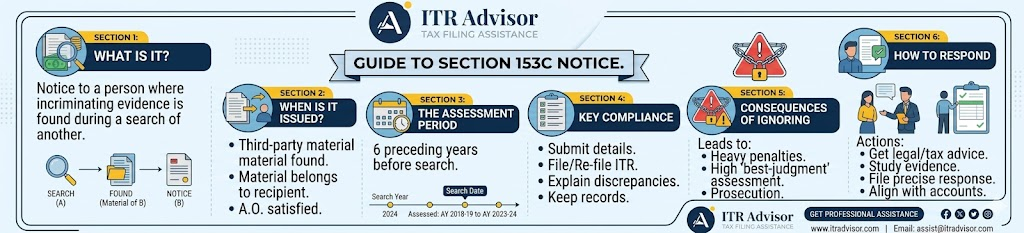

Imagine this: The Income Tax Department raids a business associate, a vendor, or even a distant acquaintance and days later, a notice lands on your doorstep under Section 153C of the Income Tax Act. You were never searched. No officer stepped into your office. Yet suddenly, you are under the scanner for six years of your income and assets. This is not a hypothetical situation. Across India in 2025 and 2026, thousands of taxpayers salaried professionals, business owners, real estate investors, and even silent partners have received notices under Section 153C without any warning whatsoever.

If you have received such a notice or if you want to protect yourself before one arrives this guide by Dr. Haresh Adwani, of Adwani and Company, is exactly what you need. Read every section carefully, because what you learn here could save you from penalties reaching up to 200% of your tax liability.

What Is Section 153C of the Income Tax Act?

Section 153C of the Income Tax Act, 1961, is a powerful provision that empowers the Assessing Officer (AO) to issue a tax notice and initiate assessment proceedings against a person who was NOT the original subject of an income tax search or seizure. In simpler terms, if the Income Tax Department raids someone else and finds documents, books of account, digital data, jewellery, or any other asset that belongs to or pertains to you you can be assessed under Section 153C, even though your premises were never raided.

This section sits within the broader framework of search and seizure assessments under Indian tax law, alongside its companion provision, Section 153A which governs assessments of the person who was actually searched. The Income Tax Department uses Section 153C to extend its reach beyond the person searched, ensuring that any connected third party with undisclosed income does not escape scrutiny.

As Dr. Haresh Adwaniof Adwani and Company always advises clients: “Section 153C is not a minor notice. It is a full-scale tax assessment that can reopen six years of your financial history. Treating it lightly is the most expensive mistake a taxpayer can make.”

Learn more about our Income Tax Assessment Services at Adwani and Company, where our team of expert CAs handles Section 153C notices with precision and strategy.

Section 153C vs Section 153A: Understanding the Critical Difference

Many taxpayers confuse Section 153A with Section 153C, and that confusion can lead to wrong responses and serious legal consequences. Here is the clearest distinction:

Section 153A : Notice to the Person Searched

When the Income Tax Department conducts a search under Section 132 or a requisition under Section 132A, the person who was searched receives a notice under Section 153A. This notice requires filing of income tax returns for the six assessment years immediately preceding the year of search, plus the current year.

Section 153C : Notice to a Third Party (You)

When documents, assets, digital records, or books of account found during a search on someone else are determined to belong to or pertain to you, the AO of the searched person hands over those materials to your Assessing Officer. Your AO then issues you a Section 153C notice and initiates the same assessment procedure as under Section 153A.

The critical phrase here is “belongs to or pertains to.” Indian courts including the Delhi High Court in the landmark Kabul Chawla case (2015) have clarified that the material found must genuinely belong to you or contain information directly relating to your income. Without this clear ownership link, the Section 153C notice can be legally challenged and quashed.

How Is a Section 153C Income Tax Notice Triggered? Step-by-Step Process

Understanding the procedural chain that leads to a Section 153C notice helps you evaluate whether the notice issued to you is legally valid a key part of your defence strategy.

The Income Tax Department conducts a search under Section 132 or a requisition under Section 132A at the premises of a person (let us call them Person A).

During the search on Person A’s premises, the investigating officers discover documents, books of account, hard drives, cash, jewellery, or other assets that appear to belong to or relate to you (Person B).

The AO in charge of Person A’s case reviews the seized material and records a Satisfaction Note a written document explaining in detail why he is satisfied that the material belongs to or pertains to Person B (you).

The seized material is formally handed over to the AO having jurisdiction over Person B (you).

Your AO reviews the material and issues a notice under Section 153C, requiring you to file income tax returns for the six assessment years preceding the year of search.

Assessment or reassessment of your income for those six years begins in accordance with the provisions of Section 153A.

According to the Income Tax Department’s guidelines and confirmed by multiple High Court rulings, the Satisfaction Note at Step 3 is non-negotiable. If it is absent, vague, or not recorded in writing before the notice is issued, the entire Section 153C proceeding is legally invalid.

Real-World Example: How a Section 153C Notice Can Arrive at Your Door

Practical Example: The Income Tax Department conducts a search in FY 2023-24 at the premises of a real estate developer in Pune. During the search, investigators discover a set of financial documents referencing a private investor who had made an unrecorded cash payment of ₹45 lakhs for a commercial property. The investor was never searched. However, the documents clearly link the payment to the investor’s PAN.

The AO records a Satisfaction Note and hands over the documents to the investor’s AO. A Section 153C notice is then issued to the investor for Assessment Years 2018-19 to 2023-24 six full years. The investor now faces potential tax demand on ₹45 lakhs, plus interest under Sections 234A, 234B, and 234C, plus a penalty that can reach up to 200% of the tax evaded under Section 270A.

This example is not extraordinary. It plays out in hundreds of cases every year, and this is precisely why proactive tax planning and clean documentation matter as much as filing returns on time.

Critical Time Limits Under Section 153C That Every Taxpayer Must Know

The Income Tax Act imposes strict time limits on assessments under Section 153C, and missing these deadlines can itself invalidate a notice. Here is what the law says:

Assessment Years Covered

Normally, a Section 153C notice covers the six assessment years immediately preceding the year in which the search was conducted. After amendments introduced in 2021, the timeline has been aligned with Section 132 and Section 132A provisions, providing greater clarity on which years can be reopened.

Extended Period of 10 Years

As amended by the Finance Act 2017, if the AO has credible evidence that undisclosed income exceeding ₹50 lakh has escaped assessment, the assessment window under Section 153C can be extended to cover up to ten years preceding the year of search. This extended period is not automatic it requires specific evidence and cannot be used as a blanket tool.

Time Limit for Completing Assessment

The Assessing Officer must complete the assessment within 12 months from the end of the financial year in which the evidence was handed over. This is a hard deadline under Section 153B, and failure to complete the assessment within this window renders the order invalid.

Dr. Haresh Adwani emphasises that checking these time limits carefully is the first defence a taxpayer should mount: “I have seen cases where the AO issued a Section 153C notice for years that were clearly outside the permissible window. A well-informed taxpayer, guided by the right CA, can get such proceedings quashed entirely based on this ground alone.”

The Satisfaction Note: Your Most Powerful Legal Shield Against a Section 153C Notice

The Satisfaction Note is arguably the most important procedural requirement in a Section 153C proceeding. Without it, the entire assessment collapses. Here is what you must know about it:

What Is the Satisfaction Note?

The Satisfaction Note is a written document prepared by the Assessing Officer of the searched person (Person A), in which he records his reasons for believing that the seized material belongs to or pertains to a third party (you, Person B). The Supreme Court and multiple High Courts have repeatedly held that this note must be prepared before the notice is issued not after.

What Happens If the Satisfaction Note Is Missing or Defective?

Indian courts have consistently quashed Section 153C assessments where the Satisfaction Note was absent, vague, or prepared mechanically. In the RRJ Securities Ltd. vs. CIT case decided by the Delhi High Court, the court held that for invoking Section 153C, the evidence must actually belong to the other person not merely refer to or relate to them. A defective Satisfaction Note is one of the strongest grounds for legally challenging a Section 153C notice.

At Adwani and Company, one of the first steps Dr. Haresh Adwani takes when reviewing a Section 153C notice is to request and examine the Satisfaction Note. A carefully prepared legal challenge based on procedural deficiencies has resulted in numerous assessments being set aside before they even begin.

Documents You Must Prepare When You Receive a Section 153C Income Tax Notice

Receiving a Section 153C notice is stressful, but a methodical, document-driven response is your most effective defence. Based on the guidelines issued by the Income Tax Department and practical experience, here is the complete list of documents you should gather immediately:

Income Tax Returns (ITR) for all 6 relevant assessment years

Books of account, ledgers, and financial statements for those years

Bank statements for all accounts (savings, current, FD, OD)

Details of all assets and liabilities during the relevant period

Complete source of funds documentation for all major transactions

Property purchase and sale documents (sale deeds, agreements)

Loan agreements and repayment records

Gift deeds or documentation for any assets received as gifts

TDS certificates and Form 26AS for all relevant years

PAN card, Aadhaar, and identity proof

Any correspondence with the searched person (Person A)

Investment records (shares, mutual funds, capital gains statements)

The Income Tax Department’s TRACES portal and the AIS (Annual Information Statement) available on the income tax e-filing portal (incometax.gov.in) provide a comprehensive picture of all transactions linked to your PAN. Reviewing your AIS before responding to any notice is a non-negotiable step recommended by Adwani and Company.

How to Respond to a Section 153C Tax Notice: A 6-Step Action Plan

Every Section 153C notice carries a response deadline. Missing that deadline can escalate the situation dramatically. Here is the structured action plan recommended by Dr. Haresh Adwani:

Do not panic, but act immediately. Every day that passes without action reduces your options.

Consult a qualified Chartered Accountant with proven experience in search and seizure assessments. This is not the time for general tax advice.

Request the Satisfaction Note and review it carefully with your CA to determine if it is procedurally valid.

Gather all the documents listed above and prepare a detailed reconciliation of your income, assets, and major transactions for the relevant years.

File the required income tax returns for past years if they were not previously filed, and ensure all disclosures are complete and accurate.

Respond to the notice within the stipulated deadline with a professionally prepared, legally sound reply that addresses each point raised by the AO.

If the Satisfaction Note is defective or the notice is issued for years beyond the permissible period, your CA may advise filing a writ petition before the appropriate High Court to get the proceedings stayed or quashed.

The team at Adwani and Company led by Dr. Haresh Adwani has successfully represented hundreds of clients before Assessing Officers, CIT(Appeals), and the Income Tax Appellate Tribunal (ITAT) in cases arising from Section 153C notices. A professionally drafted response, backed by clean documentation and sound legal arguments, resolves the majority of these cases at the earliest stage.

Consequences of Ignoring or Mishandling a Section 153C Income Tax Notice

The Income Tax Act provides for serious consequences when a taxpayer ignores a Section 153C notice or fails to respond adequately. Understanding these consequences reinforces why expert guidance is non-negotiable:

Tax demands on undisclosed income discovered during assessment

Interest under Section 234A (delay in filing), Section 234B (advance tax shortfall), and Section 234C (installment default)

Penalty under Section 270A of up to 200% of the tax amount in cases of misreporting or under-reporting of income

Best judgment assessment under Section 144 if the taxpayer fails to comply with notices or produce required documents

Potential prosecution proceedings in cases involving deliberate concealment of income

None of these consequences are inevitable if you respond correctly and promptly. The Income Tax Department’s own circulars emphasise that taxpayers who cooperate fully and disclose income honestly are treated more favourably during assessment proceedings.

Official Government References and Authority Signals

The legal basis for Section 153C proceedings is firmly established in the Income Tax Act, 1961, as administered by the Central Board of Direct Taxes (CBDT). The CBDT has issued multiple circulars and instructions clarifying procedural requirements for Assessing Officers conducting assessments under Sections 153A and 153C. Taxpayers who receive Section 153C notices have the right to access these circulars and rely on them in their defence.

The Ministry of Finance, through the Income Tax Department, has also introduced the Faceless Assessment Scheme to reduce physical interaction and improve transparency in assessment proceedings. While Section 153C cases may have specific exemptions from full faceless assessment, the principles of natural justice including the right to be heard and the right to challenge procedural deficiencies remain fully applicable.

For the most current information on income tax assessments, the official Income Tax Department website at incometax.gov.in and the CBDT’s circulars available on the website of the Ministry of Finance are the authoritative sources.

Frequently Asked Questions

Q1. Can I receive a Section 153C notice even if the Income Tax Department never searched my premises?

Yes. Section 153C specifically applies to persons who were NOT the subject of the original search. If documents or assets belonging to you are found during a search at someone else’s premises, you can receive a Section 153C notice.

Q2. How many years of income can be reassessed under Section 153C?

Normally, the six assessment years immediately preceding the year of search. In cases where undisclosed income exceeding ₹50 lakh is discovered, the assessment window can be extended to ten years. The exact years depend on when the search was conducted and when the material was handed over to your AO.

Q3. What is the Satisfaction Note in Section 153C, and why does it matter?

The Satisfaction Note is a mandatory written document prepared by the AO of the searched person, recording the reasons why seized material belongs to or pertains to a third party. Without this note, a Section 153C notice is legally invalid and can be challenged in court.

Q4. What documents should I keep ready when I receive a Section 153C notice?

You should immediately gather income tax returns for the past six years, bank statements, books of account, asset and liability details, property documents, loan agreements, Form 26AS, and source of funds documentation for all major transactions. Consulting an experienced CA

Q5. Can a Section 153C notice be challenged or quashed?

Yes. If the Satisfaction Note is absent or defective, if the notice covers years beyond the permissible period, or if the seized material does not genuinely belong to the taxpayer, the Section 153C notice can be legally challenged before the High Court through a writ petition or before the CIT(Appeals) or ITAT in appeal proceedings.

Q6. How can Adwani and Company help me respond to a Section 153C tax notice?

Dr. Haresh Adwani and the expert team at Adwani and Company provide end-to-end assistance: reviewing the Satisfaction Note, identifying legal deficiencies, gathering and organising documents, preparing professionally drafted responses, representing clients before the AO, CIT(Appeals), and ITAT, and if necessary, pursuing High Court relief. Connect with Adwani and Company today at www.adwaniandco.com.

Conclusion:

A Section 153C income tax notice is not the end of the road. It is a beginning a beginning of a legal process that, with the right expertise and preparation, can be navigated successfully. The law provides clear procedural safeguards including the mandatory Satisfaction Note requirement, strict time limits for assessment, and the right to appeal and these safeguards exist precisely to protect taxpayers from arbitrary or unlawful proceedings.

The two most important actions you can take right now are: first, understand the provisions of Section 153C thoroughly so that you know your rights; and second, engage a qualified and experienced Chartered Accountant who has handled income tax search assessment cases before. Do not attempt to respond to a Section 153C notice without professional guidance. The stakes are too high.

Dr. Haresh Adwani has built Adwani and Company on the principle that every taxpayer deserves expert, transparent, and accessible professional guidance especially in high-stakes situations like a Section 153C notice. With a team of experienced CAs, tax lawyers, and assessment specialists, Adwani and Company has successfully resolved Section 153C and Section 153A cases across India.

Read our detailed guide on Income Tax Appeals and Assessment Proceedings to understand your complete rights as a taxpayer under Indian tax law.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

A prominent “File Your ITR Now” button near the top and again at the end of the article.

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.

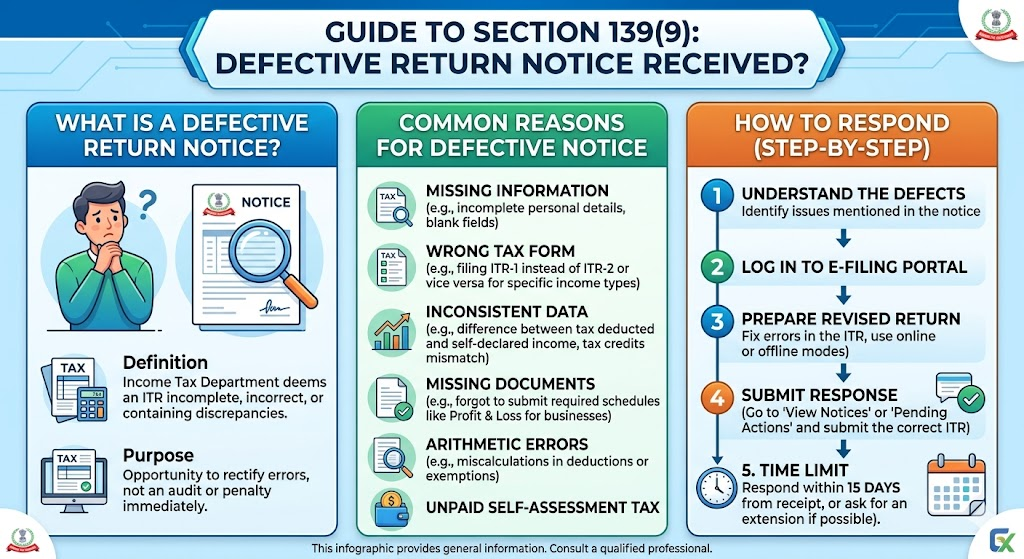

Have you received an email or SMS from the Income Tax Department stating that your Income Tax Return (ITR) is “Defective” under Section 139(9) of the Income Tax Act?

Don’t panic.

A Section 139(9) Notice does not automatically mean that you have concealed income or committed tax evasion. However, it is a notice that requires immediate attention because failure to respond within the prescribed time may result in your Income Tax Return being treated as invalid.

In simple terms, it may be as if you never filed your return at all.

In this article, we explain what a Section 139(9) Defective Return Notice means, why it is issued, common reasons, real-life examples, and how to respond correctly.

What is a Section 139(9) Defective Return Notice?

A Section 139(9) Notice is issued when the Income Tax Department finds defects, inconsistencies, omissions, or incomplete information in the Income Tax Return filed by a taxpayer.

The department provides an opportunity to correct the defect within the prescribed period.

Once the defect is corrected and submitted, the return continues to be treated as a valid return.

However, if the defect is not corrected, the return may become invalid.

Why is a Section 139(9) Defective Return Notice Issued?

The Income Tax Department processes millions of returns every year using automated systems.

If certain information is missing or inconsistent, a defective return notice may be generated.

Common Reasons for Section 139(9) Notice

Wrong ITR Form Selected

This is one of the most common mistakes.

Example:

A taxpayer sold mutual funds and earned capital gains but filed ITR-1 instead of the appropriate ITR form.

The department may issue a defective return notice.

Business Income Not Properly Reported

Taxpayers declaring business or professional income may fail to provide mandatory financial details.

Example:

A consultant reports professional income but does not provide the required Profit & Loss Account information.

Mismatch Between Income and TDS

Income reported in the return may not match TDS information available in Form 26AS.

Missing Balance Sheet Details

In some cases, taxpayers are required to disclose balance sheet information but fail to do so.

Incomplete Capital Gains Reporting

Sale transactions may be reported without proper capital gains computation.

Incorrect Claim of Losses

Business losses or capital losses may be claimed without furnishing required details.

Incomplete Foreign Asset Reporting

Taxpayers required to disclose foreign assets may fail to provide complete information.

Mr. Rahul, a software engineer from Pune, filed his Income Tax Return using ITR-1 because he believed he only had salary income.

However, during the financial year he had redeemed mutual funds worth ₹8 lakh.

Although the actual capital gain was small, the transaction itself required reporting under the appropriate ITR form.

A few weeks after filing, he received a Section 139(9) Defective Return Notice stating that the return was defective due to the use of an incorrect ITR form.

After reviewing the notice, the return was corrected and re-submitted using the correct form within the prescribed time.

The matter was resolved without penalty.

What Happens if You Ignore a Section 139(9) Notice?

Ignoring a defective return notice can create serious consequences.

The Income Tax Department may treat the return as invalid.

This can lead to:

Loss of refund claims

Late filing consequences

Interest liability

Loss of carry-forward of losses

Additional compliance issues

In simple words, it may be treated as if no valid return was filed

How to Respond to a Section 139(9) Notice?

Step 1: Read the Notice Carefully

Identify the exact defect mentioned by the department.

Step 2: Download the Notice

Review all instructions and defect codes.

Step 3: Gather Required Information

Depending on the defect, you may need:

Form 16

AIS

Form 26AS

Capital gains statements

Business records

Foreign asset information

Step 4: Correct the Defect

Update the return and provide the information requested by the department.

Step 5: Submit Response Within Time

Always ensure that the response is submitted within the specified timeline.

Most Common Defective Return Mistakes in 2026

Based on practical experience, the following mistakes are increasingly common:

✔️ Filing ITR-1 despite having capital gains

✔️ Ignoring AIS information

✔️ Not reporting FD interest

✔️ Not reporting dividend income

✔️ Incorrect business income disclosures

✔️ Missing foreign asset information

✔️ Wrong selection of ITR form

✔️ Incomplete capital gains schedules

Can a Defective Return Notice Be Resolved?

Yes.

Most Section 139(9) notices can be resolved successfully if the defect is identified and corrected promptly.

The key is understanding the issue and taking timely action.

Frequently Asked Questions

Is a Section 139(9) Notice serious?

It should not be ignored. While it is generally a compliance-related notice, failure to respond can invalidate the return.

Does a defective return notice mean scrutiny assessment?

No. A Section 139(9) Notice is different from a scrutiny notice under Section 143(2).

Can I get a refund if my return is defective?

The defect usually needs to be resolved before processing can continue.

Can I handle the notice myself?

Simple defects may be corrected independently. However, where capital gains, business income, foreign assets, or multiple issues are involved, professional guidance can be beneficial.

Why Taxpayers Should Seek Professional Help

Many taxpayers attempt to resolve defective return notices without understanding the underlying issue.

A wrong response can result in:

Invalid return status

Delayed refunds

Additional notices

Loss of tax benefits

Professional review can help identify the actual defect and ensure that the return is corrected properly.

Final Thoughts

A Section 139(9) Notice is one of the most common notices issued by the Income Tax Department. In most cases, it is not an allegation of tax evasion but an opportunity to correct errors in the return.

The sooner the defect is identified and corrected, the smoother the resolution process will be.

If you are unsure about the notice, seeking expert advice can help protect your refund, maintain compliance, and avoid unnecessary complications.

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

Received a Section 139(9) Notice? Consult ITRAdvisor.in

If you have received a Section 139(9) Defective Return Notice, do not ignore it.

At ITRAdvisor.in, we regularly assist taxpayers with:

✔️ Defective Return Notices

✔️ AIS Mismatch Issues

✔️ Capital Gains Reporting

✔️ Wrong ITR Form Selection

✔️ Revised Returns

✔️ NRI Taxation

✔️ Income Tax Notices

✔️ Return Rectification and Compliance

Whether your notice relates to capital gains, business income, foreign assets, AIS mismatches, or an incorrect ITR form, our team can help you understand the issue and prepare an appropriate response.

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

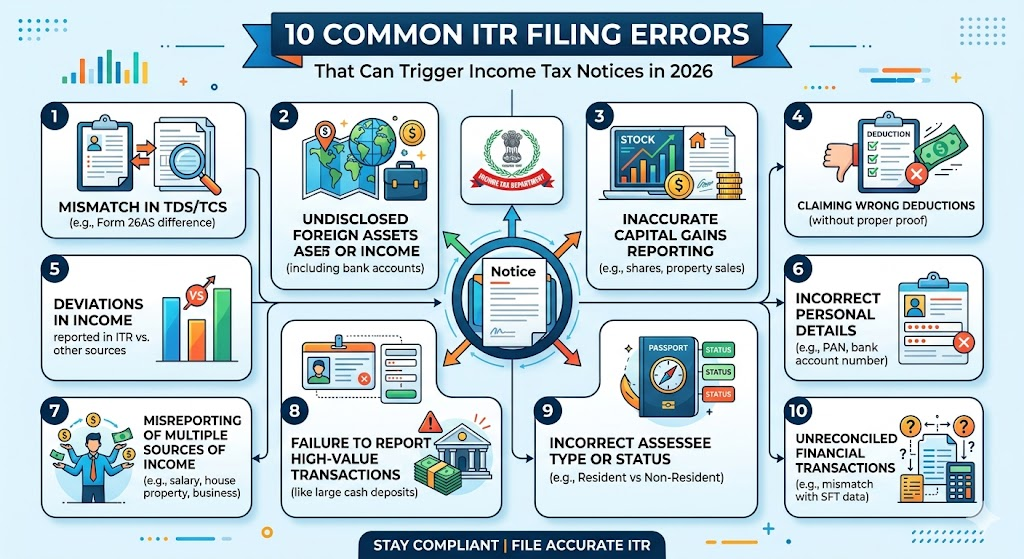

Filing your Income Tax Return (ITR) may appear simple, especially with pre-filled data available on the Income Tax Portal. However, thousands of taxpayers receive notices every year due to avoidable mistakes while filing their returns.

Many taxpayers believe that if tax has been deducted or Form 16 has been issued, there is no possibility of receiving a notice. Unfortunately, this is not always true.

The Income Tax Department now uses data from:

Annual Information Statement (AIS)

Form 26AS

Banks

Mutual Funds

Stock Brokers

Property Registrars

Credit Card Companies

As a result, even small filing errors can result in tax demands, refund delays, scrutiny, or notices.

Let’s look at the most common ITR filing mistakes and how to avoid them.

Not Checking AIS Before Filing

This is currently one of the biggest mistakes taxpayers make.

Many individuals file their returns using only Form 16 without reviewing the Annual Information Statement (AIS).

AIS may contain:

FD interest

Dividend income

Share transactions

Mutual fund redemptions

Property transactions

Foreign remittances

If income reflected in AIS is not reported in the ITR, the department may issue a notice.

Example

A salaried employee reported salary income based on Form 16 but forgot to include ₹38,000 FD interest reflected in AIS.

The mismatch was later identified during return processing.

Many taxpayers assume that because TDS has been deducted, interest income need not be reported.

This is incorrect.

Commonly missed income includes:

Savings account interest

Fixed Deposit interest

Recurring Deposit interest

The income must generally be disclosed in the return.

Ignoring Dividend Income

Dividend income received from shares and mutual funds is often forgotten during filing.

Since this information is generally available to the department, non-reporting can create mismatches.

Incorrect Capital Gains Reporting

This is one of the most frequent reasons for notices.

Taxpayers often:

Forget to report share transactions

Ignore mutual fund redemptions

Miscalculate capital gains

Fail to report property sales

Example

A taxpayer sold mutual funds worth ₹12 lakh and assumed there was no taxable gain because the amount was reinvested.

The transaction appeared in AIS but was omitted from the ITR.

A notice was later received seeking clarification.

Claiming Deductions Without Proper Documentation

Many taxpayers claim deductions under:

Section 80C

Section 80D

Section 80G

without maintaining supporting records.

If questioned by the department, documentary evidence may be required.

Not Reporting Foreign Assets

This mistake is particularly common among NRIs returning to India.

Foreign bank accounts, investments, and other reportable assets may require disclosure depending on residential status and applicable provisions.

Failure to disclose can have serious consequences.

Not Reconciling Form 26AS

Before filing, taxpayers should compare:

Form 16

Form 26AS

AIS

Bank records

Differences should be investigated before submission.

Incorrect Bank Account Details

A simple mistake in bank account information can result in:

Refund failure

Delayed processing

Additional compliance issues

Always verify account details carefully.

Filing in a Hurry Before the Deadline

Many taxpayers wait until the last few days before the due date.

As a result, important items are overlooked, including:

AIS mismatches

Capital gains

Interest income

Foreign assets

TDS discrepancies

Rushed filing often leads to mistakes that could have been avoided.

Real-Life Example: Notice Due to AIS Mismatch

Mr. Sharma filed his Income Tax Return based solely on Form 16 provided by his employer.

A few months later, he received a communication from the Income Tax Department.

Upon review, it was found that:

FD interest of ₹62,000 reflected in AIS was not reported.

Dividend income of ₹14,000 was omitted.

Mutual fund redemption transactions were not disclosed.

Although the omissions were unintentional, additional compliance was required to resolve the matter.

This situation is becoming increasingly common as the department relies heavily on AIS data.

Can I Correct an ITR Filing Mistake?

In many situations, taxpayers may be able to rectify mistakes by filing a revised return within the applicable timelines.

However, early identification of errors is important.

The longer a mistake remains uncorrected, the greater the risk of notices, demands, or penalties.

How to Avoid ITR Filing Errors:

Before filing your return:

✔️ Verify Form 16

✔️ Check AIS thoroughly

✔️ Review Form 26AS

✔️ Reconcile bank interest

✔️ Verify dividend income

✔️ Check capital gains statements

✔️ Confirm bank account details

✔️ Select the correct ITR form

✔️ Review foreign asset disclosures

✔️ Seek professional advice for complex transactions

Frequently Asked Questions

1.Can a small mistake in ITR trigger a notice?

Yes. Even small mismatches between the ITR and AIS can result in communications from the Income Tax Department.

2.Can I revise my ITR after filing?

In many cases, taxpayers can file a revised return within the prescribed timelines.

3.Is AIS more important than Form 16?

Both are important. However, AIS often contains additional information that may not appear in Form 16.

What is the most common ITR filing mistake

Currently, failure to reconcile AIS before filing is among the most common errors.

Final Thoughts

Most Income Tax notices are not issued because taxpayers intentionally hide income. They are often the result of simple mistakes, omissions, or mismatches.

A careful review of AIS, Form 26AS, interest income, capital gains, and deductions before filing can significantly reduce the risk of future notices and tax disputes.

Taking a few extra minutes before filing can save months of stress later.

Many taxpayers file their returns themselves and later discover mistakes that result in notices, refund delays, or additional tax demands.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

Various institutions are required to report certain transactions to the Income Tax Department.

These reports help the department verify whether financial activities align with declared income.

SFT reporting has significantly increased transparency and reduced the possibility of undisclosed transactions remaining unnoticed.

The Biggest Mistake Taxpayers Make

The most common mistake is filing an ITR based only on:

Form 16

Salary details

TDS certificates

Without checking:

AIS

Form 26AS

Capital gains reports

Mutual fund statements

Bank interest income

This often leads to avoidable notices.

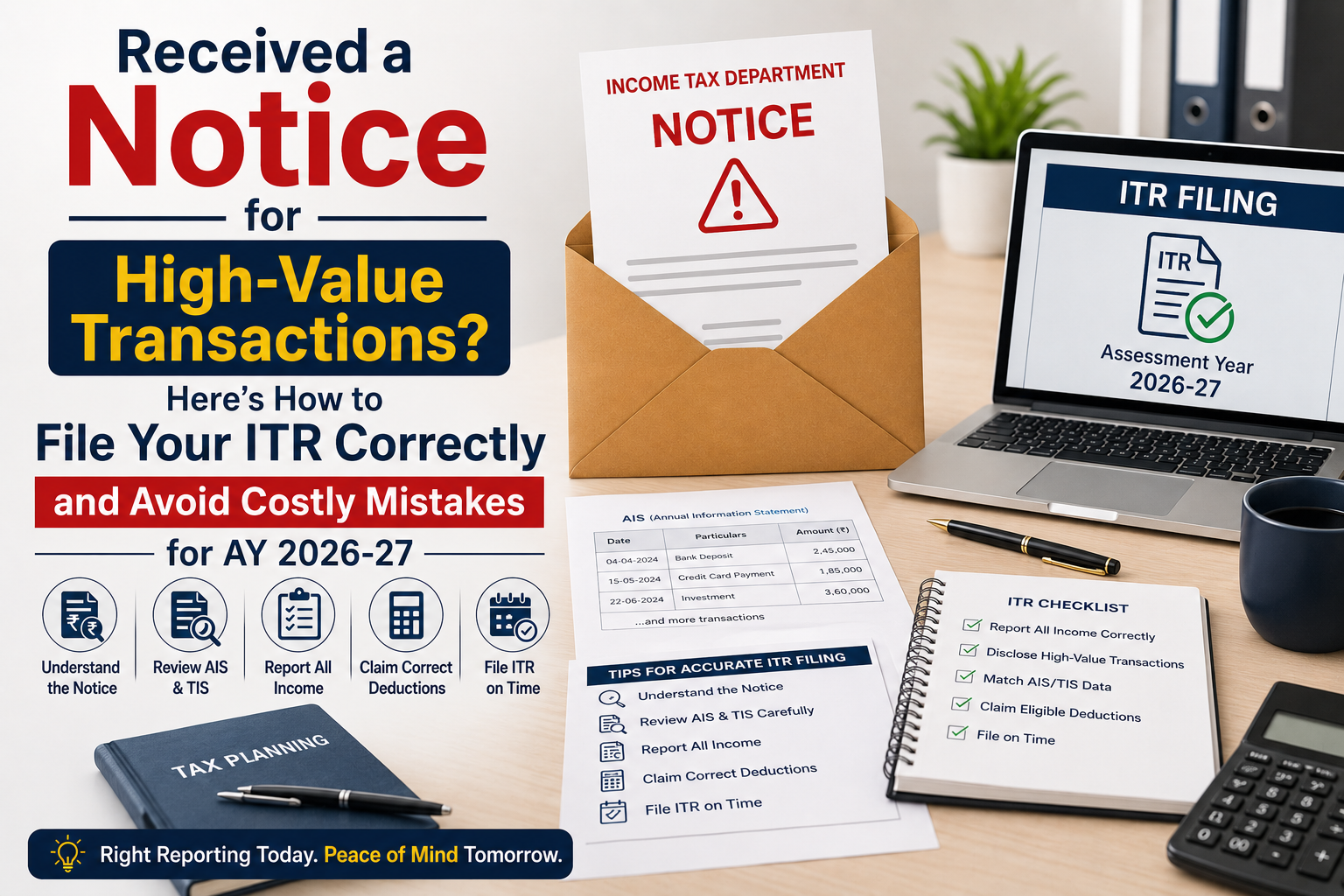

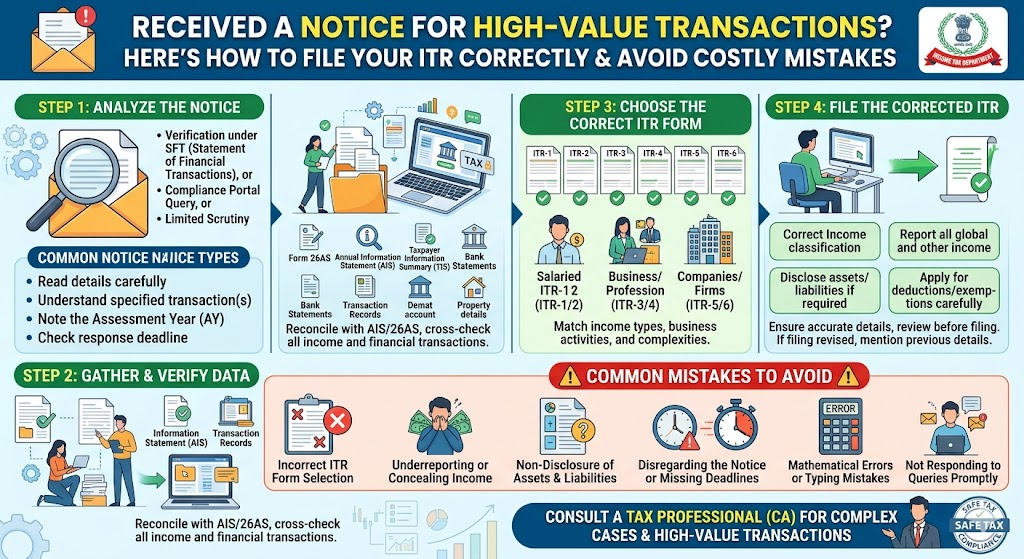

How to File Your ITR Correctly If You Have High-Value Transactions

Step 1: Download and Review AIS

Before filing:

✔️ Review all transactions appearing in AIS

✔️ Verify accuracy

✔️ Check whether any transaction appears unfamiliar

Step 2: Reconcile Income Sources

Match:

Salary income

Interest income

Dividend income

Capital gains

Rental income

Business income

with AIS and Form 26AS.

Step 3: Report Capital Gains Properly

Many taxpayers report only profits and ignore losses.

This is a mistake.

All relevant transactions should be reported appropriately.

Step 4: Maintain Documentation

Keep records of:

Property purchases

Loan statements

Mutual fund investments

Bank transactions

Gift deeds

Sale agreements

Proper documentation helps support explanations if required.

Step 5: Choose the Correct ITR Form

Selecting the wrong ITR form can create compliance issues.

A professional review is particularly important where multiple income sources exist.

Real-Life Example

A salaried employee earning ₹16 lakh annually filed his own return.

He reported:

✔️ Salary income

But forgot to report:

❌ Mutual fund redemption

❌ Dividend income

❌ Fixed deposit interest

All these transactions appeared in AIS.

A compliance notice was subsequently issued seeking clarification.

The matter was resolved, but only after additional effort, documentation, and correspondence.

Most importantly, the notice could have been avoided through proper review before filing.

Frequently Asked Questions

1.Does a high-value transaction always lead to a notice?

No. However, transactions that are inconsistent with reported income may attract scrutiny.

2.What should I do if a transaction in AIS is incorrect?

The discrepancy should be reviewed carefully and appropriate action should be taken before filing the return.

3.Can cash deposits trigger an income tax notice?

Yes. Large cash deposits are among the most common reasons for notices

4.Are mutual fund transactions reported to the Income Tax Department?

Yes. Certain investment and redemption transactions may appear in AIS and related reporting systems.

5. Should I file my return based only on Form 16?

No. AIS, Form 26AS, capital gains statements, and other relevant information should also be reviewed.

Warning Signs You Should Not Ignore

Consider professional assistance if:

⚠️ Your AIS contains unfamiliar entries

⚠️ You purchased property during the year

⚠️ You redeemed mutual funds

⚠️ You traded in shares

⚠️ You made substantial cash deposits

⚠️ Your credit card expenditure is significantly high

⚠️ You received an income tax notice

⚠️ You have multiple income sources

Need Help Understanding Your AIS or High-Value Transactions?

Every year, thousands of taxpayers receive notices because they file returns without understanding what the Income Tax Department already knows through AIS and SFT reporting.

At Adwani & Co. | ITR Advisor, we help taxpayers:

✅ Review AIS and TIS

✅ Analyze high-value transactions

✅ Report capital gains correctly

✅ File accurate ITRs

✅ Respond to notices

✅ Reduce the risk of future scrutiny

✅ Reconcile AIS with income disclosures

Book an AIS & ITR Review Before Filing

If your AIS shows transactions you don’t understand, don’t guess.

A single reporting mistake can lead to notices, delays, additional tax demands, and unnecessary stress.

Our experts can review your AIS, explain the transactions, identify potential issues, and help you file your return correctly.

📞 Contact Adwani & Co. today for a professional AIS review and error-free ITR filing