June 2026• Nidhi Adwani

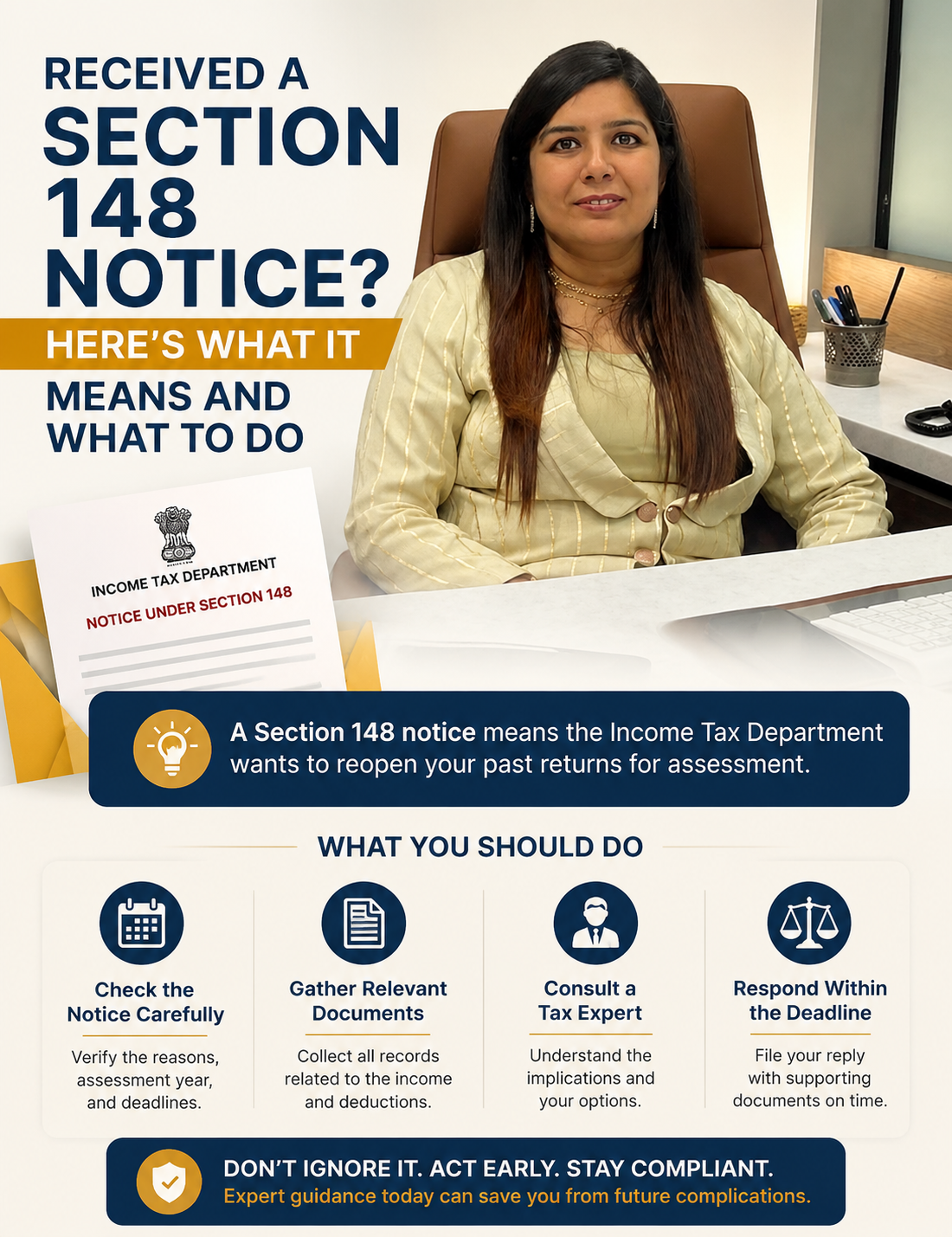

A Section 148 Notice is one of the most serious notices that a taxpayer can receive from the Income Tax Department.

Many taxpayers panic when they receive such a notice because it relates to income that the department believes may have escaped assessment in an earlier year.

However, receiving a Section 148 Notice does not automatically mean that you have committed tax evasion or concealed income. In many cases, notices are issued due to information mismatches, non reporting of transactions, or incomplete disclosures in the Income Tax Return (ITR).

Understanding the reason for the notice and responding correctly is critical.

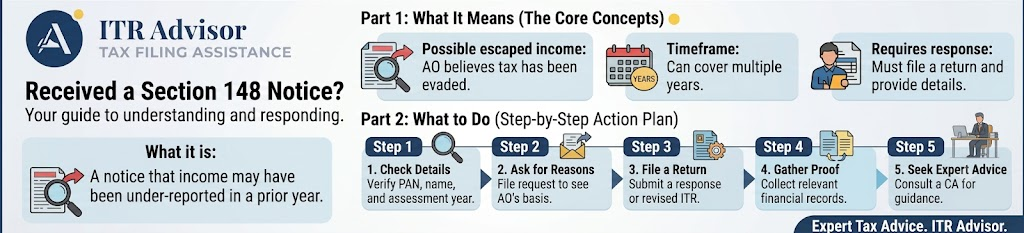

What is a Section 148 Notice?

A Section 148 Notice is issued when the Income Tax Department has information suggesting that taxable income may have escaped assessment.

In simple words, the department believes that:

- Certain income was not disclosed in the ITR, or

- Certain transactions were not properly reported, or

- Additional tax may be payable.

The notice gives the taxpayer an opportunity to explain the transaction before reassessment proceedings are completed.

Why is a Section 148 Notice Issued?

Today, the Income Tax Department receives information from multiple sources, including:

- Banks

- Property Registration Offices

- Stock Brokers

- Mutual Fund Companies

- Credit Card Companies

- GST Authorities

- Foreign Tax Authorities

- Annual Information Statement (AIS)

If the information available with the department does not match the details disclosed in the ITR, a Section 148 Notice may be issued.

Common Reasons for Receiving a Section 148 Notice

- Property Sale Not Reported

The taxpayer sold a property but failed to report capital gains in the return.

- High-Value Credit Card Spending

Large spending patterns not matching declared income.

- Share Market Transactions Not Disclosed

Capital gains or trading profits omitted from the ITR.

- Foreign Income Not Reported

Income earned outside India not disclosed where required.

- Cash Deposits in Bank Accounts

Large cash deposits that do not match reported income.

- Business Receipts Under-Reported

Turnover reflected in GST records differs from income declared in the ITR.

Real-Life Example: Section 148 Notice for Property Sale

Mr. Rajesh, a salaried employee from Pune, sold a residential plot in 2022 for ₹72 lakh.

Since tax was deducted by the buyer and the sale proceeds were credited to his bank account, Mr. Rajesh assumed that no further reporting was required.

While filing his Income Tax Return, he disclosed his salary income but failed to report the capital gains arising from the property sale.

The property transaction was reported to the Income Tax Department through the registrar’s office and reflected in its database.

Two years later, Mr. Rajesh received a Section 148 Notice stating that income chargeable to tax appeared to have escaped assessment.

After consulting a tax professional, he:

- Obtained the purchase documents.

- Calculated the indexed cost of acquisition.

- Computed long-term capital gains.

- Submitted proof of investment made in another residential property.

- Claimed exemption under the applicable provisions.

After reviewing the documents, the Income Tax Department accepted the explanation and completed the reassessment proceedings.

This is one of the most common reasons for Section 148 Notices in India.

Real-Life Example: Section 148 Notice for Credit Card Spending

A taxpayer declared annual income of ₹9 lakh in his Income Tax Return.

However, information available with the Income Tax Department showed credit card spending exceeding ₹24 lakh during the same financial year.

The department sought an explanation regarding the source of funds used for such expenditure.

Upon examination, it was found that a significant portion of the spending was incurred for family members and reimbursed by relatives.

Supporting documents were submitted and the matter was explained during reassessment proceedings.

This example highlights how high-value transactions can attract scrutiny even when there is no tax evasion.

Read our detailed guide on:Got an Income Tax Notice for High Credit Card Spending?

What Should You Do After Receiving a Section 148 Notice?

Step 1: Do Not Ignore the Notice

Ignoring the notice can result in reassessment being completed based on available information.

Step 2: Understand the Issue

Identify:

- Assessment Year involved

- Transaction questioned by the department

- Deadline for response

Step 3: Gather Documents

Depending on the issue involved, collect:

- Bank statements

- Property documents

- Capital gains calculations

- Loan documents

- Investment records

- Business books of accounts

Step 4: Verify the Facts

Many notices arise because the department’s information is incomplete or because a transaction has been misunderstood.

Step 5: Submit a Proper Response

A well-documented response supported by evidence can significantly improve the outcome of reassessment proceedings.

Is Section 148 Notice Serious?

Yes.

A Section 148 Notice should always be taken seriously because it involves reopening an earlier assessment.

However, seriousness does not mean guilt.

Many genuine taxpayers successfully resolve reassessment proceedings by providing proper explanations and supporting documents.

What Happens if You Ignore a Section 148 Notice?

Failure to respond may result in:

- Reassessment based on available records

- Additional tax demand

- Interest liability

- Penalty proceedings in certain cases

Therefore, timely action is essential.

Frequently Asked Questions (FAQs)

1.Does a Section 148 Notice mean I have concealed income?

No. The notice only indicates that the department believes income may have escaped assessment and seeks an explanation.

2.Can salaried employees receive a Section 148 Notice?

Yes. Property transactions, share trading, foreign assets, and high-value transactions can trigger notices even for salaried taxpayers.

3.Can a Section 148 Notice be issued years after filing the return?

Yes. Subject to statutory conditions and timelines prescribed under the Income Tax Act.

4.Should I seek professional assistance?

Where the notice involves property transactions, capital gains, business income, foreign assets, or substantial tax demands, professional guidance is strongly advisable.

About the Author Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co., where she plays a key role in people management, team development, organizational culture, and business communications. With a background in Law and MBA (Human Resources), she combines legal understanding with modern HR practices to support a productive and growth-oriented workplace.

Beyond HR management, Nidhi actively oversees staff engagement initiatives, recruitment, employee development, and internal operations. She also manages the firm’s social media presence and contributes to content strategy, helping communicate valuable insights to clients and professionals through informative articles and digital engagement.

As a regular contributor to the blogs of ITRAdvisor and Adwani & Co., she writes on topics related to human resources, workplace culture, leadership, employee engagement, professional development, and organizational effectiveness. Her articles aim to simplify practical HR concepts, share industry perspectives, and encourage continuous learning among professionals and business owners.

Through her writing, Nidhi seeks to bridge the gap between people, processes, and professional growth, helping organizations build stronger teams and healthier work environments.

Need Help with a Section 148 Notice?

Receiving a reassessment notice can be stressful, but the right response at the right time can make a significant difference.

If you have received a Section 148 Notice and need assistance in understanding the notice, preparing a response, calculating capital gains, explaining high-value transactions, or representing your case before the Income Tax Department, professional support can help protect your interests.

For assistance and consultation, contact ITRAdvisor.in. Our team helps taxpayers across India with ncome Tax Notices, Reassessment Proceedings, AIS Mismatches, Capital Gains Issues, NRI Taxation, and ITR Compliance matters.

Early action can often prevent unnecessary tax disputes and penalties.

Leave a Reply