Form 26A and TDS Default

You deducted TDS. Or at least, you thought you did. Then comes the notice Section 201(1) of the Income Tax Act, 1961 declares you a ‘defaulter.’ The Income Tax Department now wants the tax you missed deducting, plus interest under Section 201(1A), and potentially a penalty. It’s a situation that thousands of Indian businesses, employers, and contractors face every year. But there’s a lesser-known relief mechanism that can shield a deductor from the tax demand Form 26A for TDS default under Section 201. The catch? It has real limits. Understanding both the relief and its boundaries is critical before you assume you’re protected.

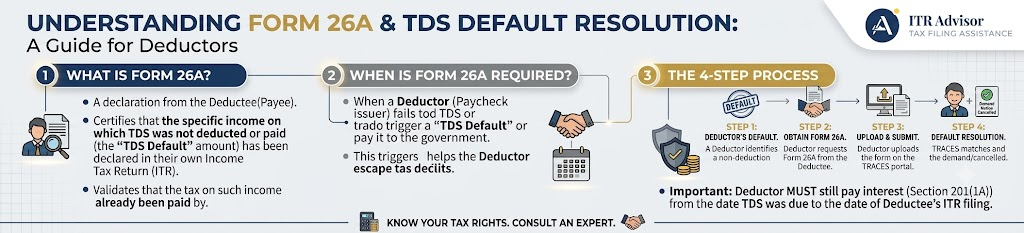

What Is a TDS Default Under Section 201?

Under the Income Tax Act, any person responsible for deducting tax at source (TDS) and failing to do so or deducting but not depositing it with the government is treated as an assessee-in-default under Section 201(1). This triggers a dual liability:

- Payment of the tax that was not deducted or short-deducted

- Interest under Section 201(1A) at 1% per month (or part of month) for non-deduction, and 1.5% per month for non-deposit

In practice, this means even a minor lapse in TDS compliance say, missing TDS on a contractor payment under Section 194C, or on rent under Section 194I can result in a substantial demand from the Income Tax Department, often years later during scrutiny or survey.

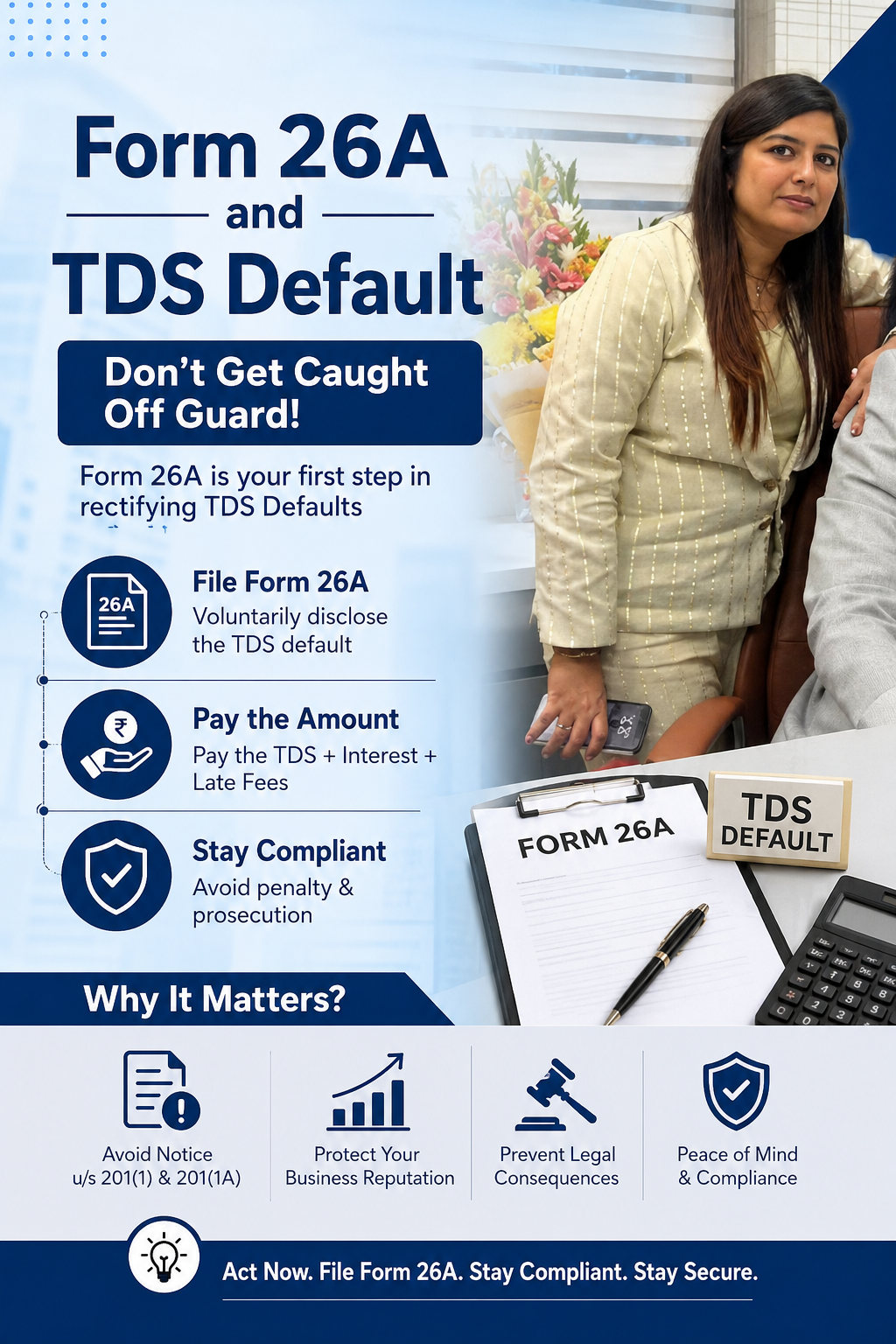

Form 26A: The TDS Default Relief Certificate That Can Save You

This is where Form 26A for TDS default relief becomes pivotal. Introduced to provide genuine relief to deductors who missed TDS but the payee still paid the tax on the income received, Form 26A is a certificate furnished by the payee’s chartered accountant confirming that:

- The payee has disclosed the income in their return

- Tax on that income has been duly paid by the payee

- No double demand should be raised on the deductor for the same income

Once Form 26A is accepted by the Income Tax Department through the TRACES portal (traces.gov.in), the deductor cannot be treated as an assessee-in-default under Section 201(1) for the tax demand portion. This is a critical and often misunderstood protection.

Important Note

- Form 26A must be filed on the TRACES portal by a Chartered Accountant on behalf of the payee.

- It is only available for non-salary payments it cannot be used for TDS defaults on salary (Section 192).

The Acknowledgement Number from Form 26A filing must be submitted during proceedings.

The Critical Limits of Section 201 Relief: What It Does NOT Protect You From

This is where many deductors make a costly mistake: they assume Form 26A wipes the slate clean. It does not.

1. Interest Under Section 201(1A) Is NOT Waived

Even if Form 26A is accepted and the deductor is relieved from the principal tax demand under Section 201(1), the interest liability under Section 201(1A) remains fully payable. This interest runs from the date of payment to the payee until the date the payee actually pays the tax — and it is charged at 1% per month for the period of non-deduction. The Supreme Court and multiple High Courts have consistently upheld this position.

2. Section 271C Penalty for Non-Deduction Remains Possible

The Assessing Officer retains discretion to levy penalty under Section 271C equal to the amount of TDS not deducted. Form 26A provides no automatic shield against this penalty. Whether penalty is levied depends on facts, intention, and the AO’s assessment.

3. Time Limit for Proceedings Under Section 201

The Income Tax Department can initiate TDS default proceedings within 7 years from the end of the financial year in which the payment was made, as per Section 201(3). If you receive a notice after several years, Form 26A still needs to be arranged a practical challenge if the payee is no longer traceable.

Key Risk Alert

Even with Form 26A in hand, your exposure to interest under Section 201(1A) is real. For a Rs. 50 lakh payment where TDS was not deducted for 3 years, the interest alone can exceed Rs. 1.8 lakh. Do not treat Form 26A as a ‘full escape’ it is a partial relief

Illustrative Example

Scenario: ABC Pvt. Ltd. paid Rs. 20,00,000 to a contractor in April 2022 without deducting TDS under Section 194C (applicable rate: 2%). The contractor paid the full income tax in their AY 2023-24 ITR. ABC obtains Form 26A in June 2024.

TDS that should have been deducted: Rs. 40,000

Period of default: April 2022 to June 2024 (approx. 26 months)

Interest under Section 201(1A): Rs. 40,000 x 1% x 26 = Rs. 10,400

Tax demand under Section 201(1): NIL (waived by Form 26A)Conclusion: Form 26A removes the Rs. 40,000 demand — but Rs. 10,400 interest is still payable. The earlier you file Form 26A, the lower the interest exposure

How to File Form 26A for TDS Default Relief: Step-by-Step

The process for obtaining Form 26A is managed through the TRACES portal of the Income Tax Department:

- Step 1: The payee (recipient of income) engages their Chartered Accountant to certify the income disclosure and tax payment.

- Step 2: The CA logs into the TRACES portal and files Form 26A with details of the payee’s income, TAN of the deductor, and confirmation of tax payment.

- Step 3: An acknowledgement number is generated, which the deductor must quote in any Section 201 proceedings.

- Step 4: The Assessing Officer verifies the certificate and, if satisfied, drops the principal demand under Section 201(1).

According to the Income Tax Department’s guidelines on TRACES, Form 26A is a valid defence mechanism available to deductors but the certificate must be genuine, and the underlying tax payment by the payee must be verified through the payee’s AIS (Annual Information Statement) and Form 26AS.

Key Takeaways: Form 26A & Section 201 TDS Default

- Section 201(1) makes a deductor liable for TDS not deducted or not deposited, plus interest.

- Form 26A, filed through TRACES by the payee’s CA, can remove the principal tax demand under Section 201(1).

- Interest under Section 201(1A) is NOT waived even with Form 26A this is the most common misconception.

- Penalty under Section 271C may still apply at the Assessing Officer’s discretion.

- Section 201 proceedings have a 7-year limitation window early resolution saves more interest.

Read our detailed guide on AIS Shows Higher Income Than Your ITR? Complete Guide to Avoid Income Tax Notice in AY 2026-27

Form 26A is not available for salary TDS defaults under Section 192

Frequently Asked Questions: Form 26A, TDS Default & Section 201 Relief

Q1. Can Form 26A completely save me from a TDS default notice?

Form 26A can eliminate the principal tax demand under Section 201(1). However, interest under Section 201(1A) remains payable and is not waived under any provision.

Q2. What is the time limit to receive a TDS default notice under Section 201?

Under Section 201(3), the Assessing Officer can issue a TDS default order within 7 years from the end of the financial year in which the payment was made to the payee.

Q3. Is Form 26A applicable for salary TDS defaults?

No. Form 26A is not available for non-deduction of TDS on salary payments under Section 192. It applies only to non-salary payments to resident payees.

Q4. Who files Form 26A the deductor or the payee?

Form 26A is filed by the payee’s Chartered Accountant on the TRACES portal. The deductor must coordinate with the payee and their CA to initiate the process.

Q5. Can TDS default under Section 201 attract criminal prosecution?

In extreme cases, willful non-deduction or non-deposit of TDS can attract prosecution under Section 276B of the Income Tax Act. Form 26A does not protect against criminal proceedings only against the civil tax demand.

Conclusion: Know the Full Picture Before Relying on Section 201 Relief

Form 26A is a genuinely useful and powerful relief mechanism for TDS defaulters but it is not a magic eraser. The Section 201 TDS default relief through Form 26A removes the principal tax demand when the payee has paid the tax, but the deductor continues to face interest under Section 201(1A) and the risk of penalty under Section 271C. Understanding this distinction is the difference between smart compliance and a costly assumption.

If you have received a Section 201 notice, are unsure about your TDS compliance position, or need help coordinating Form 26A through the TRACES portal, visit itradvisor.in for expert guidance and step-by-step resources designed for Indian taxpayers and businesses.

About the Author – Nidhi Adwani

Nidhi Adwani is the Human Resources Manager at Adwani & Co. She is a Law Graduate and holds an MBA in Human Resources. She manages recruitment, employee engagement, team development, workplace culture, and the firm’s social media and content activities. Passionate about people and organizational growth, she also contributes articles for ITRAdvisor and Adwani & Co. Her writing focuses on HR practices, leadership, workplace engagement, and professional development, offering practical insights for professionals and businesses.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

Visit ITRAdvisor.in today for professional guidance and consultation.

Early action can often prevent bigger tax problems later.

Disclaimer ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.