Section 80GGC Deduction Disallowance

Imagine claiming a perfectly legal tax deduction one that the Income Tax Act explicitly allows and having it disallowed by your Assessing Officer simply because he found it suspicious. No evidence. No proof of wrongdoing. Just suspicion. This is precisely the situation that the Income Tax Appellate Tribunal (ITAT) recently pushed back against in a landmark ruling on Section 80GGC deductions, and it has important implications for every Indian taxpayer who has donated to a registered political party.

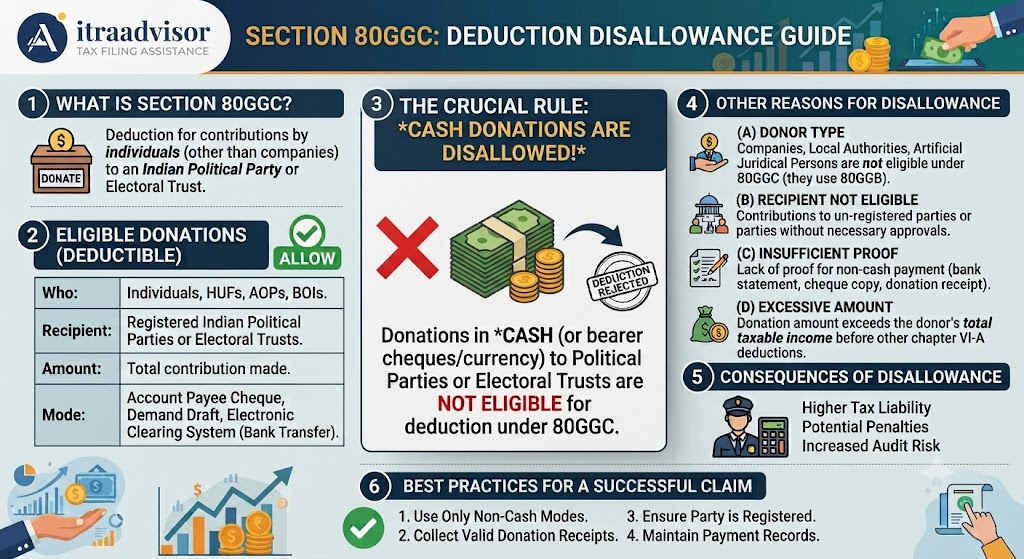

What Is Section 80GGC? Understanding the Deduction for Political Contributions

Section 80GGC of the Income Tax Act provides a full 100% deduction on contributions made by any person (other than a company or local authority) to a registered political party or an electoral trust. This is one of the few deductions in the Indian tax code that allows complete relief there is no upper ceiling on the deduction amount, subject to the conditions below.

To claim the Section 80GGC deduction, the contribution must satisfy all of the following conditions:

- The donor must be an individual, HUF, firm, AOP, or BOI not a company or a local authority.

- The contribution must be made to a political party registered under Section 29A of the Representation of the People Act, 1951, or to an electoral trust.

- The payment must be made through any mode other than cash. Contributions made in cash are explicitly excluded from the Section 80GGC deduction benefit.

- The taxpayer must obtain a receipt from the political party or electoral trust acknowledging the donation.

When these conditions are satisfied, the Section 80GGC deduction is a legitimate and fully supported claim under the Income Tax Act. Disallowing it requires evidence — not conjecture.

The ITAT Ruling: Why Suspicion Alone Cannot Disallow a Section 80GGC Deduction

In a significant ruling that reinforces taxpayer rights, the Income Tax Appellate Tribunal held that mere suspicion on the part of the Assessing Officer (AO) without any concrete, tangible evidence of fraud, bogus payment, or non-compliance with Section 80GGC conditions is legally insufficient to disallow a Section 80GGC deduction claim.

The facts in the case were straightforward: the taxpayer had made a documented, non-cash contribution to a registered political party, claimed the Section 80GGC deduction in the ITR, and produced the relevant receipt. The AO, however, raised doubts about the genuineness of the transaction and disallowed the deduction without examining the political party’s records, without issuing a summons, and without pointing to any specific defect in the documentation.

The ITAT found this approach fundamentally flawed. The tribunal emphasised a principle that runs through Indian tax jurisprudence: the burden of proof lies on the tax department to establish that a claimed deduction is fraudulent or ineligible not on the taxpayer to disprove a suspicion. If the AO had genuine doubts, the correct course was to investigate the political party, verify the receipt independently, or conduct enquiries under Sections 131 or 133(6) of the Income Tax Act. None of that happened. Disallowance of the Section 80GGC deduction was accordingly set aside.

Worked Example: What a Valid Section 80GGC Deduction Looks Like

| Parameter | Detail |

| Taxpayer | Salaried individual, AY 2026-27 |

| Gross Total Income | ₹18,00,000 |

| Donation Made To | Registered political party (Sec. 29A, RPA 1951) |

| Amount Donated | ₹2,00,000 (via NEFT) |

| Receipt | Obtained from the political party |

| 80GGC Deduction | ₹2,00,000 (100% of donation, no ceiling) |

| Net Taxable Income | ₹16,00,000 after 80GGC deduction |

| Outcome If AO Disallows Without Evidence | Appealable at CIT(A) and ITAT — taxpayer likely to succeed per this ruling |

What Indian Taxpayers Must Do to Protect Their Section 80GGC Deduction Claim

The ITAT ruling is a relief, but it does not mean taxpayers can afford to be careless with documentation. If your Section 80GGC deduction is questioned, your first line of defence is the quality of your paperwork. Here is what you must have:

Documentation Checklist for Section 80GGC Deduction

- Receipt from the registered political party or electoral trust specifically acknowledging the donation amount, date, and your PAN.

- Bank statement or payment proof showing the NEFT/cheque/digital transfer cash donations are entirely ineligible under Section 80GGC.

- Confirmation that the party is registered under Section 29A of the Representation of the People Act, 1951 you can verify this through the Election Commission of India’s published list.

- Copy of your ITR showing the Section 80GGC deduction has been correctly entered in Schedule VI-A.

If your Section 80GGC deduction is disallowed despite clean documentation, you have a strong appellate case, as this ITAT ruling demonstrates.

Key Takeaways: Section 80GGC Deduction and the ITAT Ruling

• Section 80GGC allows a 100% tax deduction on contributions to registered political parties or electoral trusts with no upper limit.

• Cash donations are completely ineligible. All 80GGC contributions must be made through banking channels.

• The ITAT has ruled that an AO cannot disallow a Section 80GGC deduction based on suspicion alone concrete evidence of non-compliance is required.

• The burden of proving that a deduction is bogus lies with the tax department, not the taxpayer.

• Maintain a receipt from the political party, bank transfer proof, and ITR Schedule VI-A entry to defend any 80GGC disallowance. • If your Section 80GGC deduction is wrongly disallowed, you can appeal to CIT(A) and then ITAT, where this ruling significantly strengthens your case.

Expert Perspective: Proving Legitimacy Is About Documentation, Not Debate

Dr. Haresh Adwani, a PhD in Commerce and tax practitioner associated with ITRAdvisor.in, puts it plainly: ‘The Section 80GGC deduction is one of the most straightforward claims in the Indian tax code 100% of a non-cash donation to a registered party, fully deductible. The problem arises not from the law but from poor record-keeping. Taxpayers who maintain a clear paper trail receipt, bank proof, PAN linkage rarely face sustained disallowance. The ITAT has now confirmed what we have always advised: suspicion is not a substitute for evidence, and taxpayers need not accept a disallowance that lacks legal foundation.’

What to Do If Your Assessing Officer Disallows Your Section 80GGC Deduction

If you receive a draft assessment order or a final order disallowing your Section 80GGC deduction without adequate grounds, your escalation path is clear:

- File your objections with the Dispute Resolution Panel (DRP) if applicable, or file an appeal before the Commissioner of Income Tax (Appeals) [CIT(A)] within 30 days of receiving the demand order.

- Cite this ITAT ruling in your appeal submissions to demonstrate that suspicion alone is legally insufficient for Section 80GGC disallowance.

- Attach all documentation receipt, bank statement, ITR schedule as annexures to your appeal memorandum.

- If the CIT(A) also rules against you, escalate to the ITAT, where the position on evidence-based disallowance is now well-established.

Do not simply pay a demand arising from an unjustified Section 80GGC disallowance. The appellate system exists precisely for these situations, and taxpayers who engage it with proper documentation generally prevail.

Read our detailed guide on ITR 1 vs ITR 2 vs ITR 3 vs ITR 4: The Definitive Guide to Picking the Right Income Tax Return Form for AY 2026-27

Frequently Asked Questions: Section 80GGC Deduction

Q1. Who is eligible to claim a Section 80GGC deduction?

Any individual, HUF, firm, AOP, or BOI can claim the Section 80GGC deduction. Companies and local authorities are explicitly excluded from this provision.

Q2. Is there a maximum limit on the Section 80GGC deduction?

No. Section 80GGC allows a 100% deduction with no upper ceiling on the amount contributed to a registered political party or electoral trust, provided the payment is non-cash.

Q3. Can my Assessing Officer disallow the Section 80GGC deduction without evidence?

As per the ITAT ruling discussed in this article, a disallowance based purely on suspicion without evidence is not legally tenable. The AO must establish specific non-compliance to disallow the deduction.

Q4. Where do I enter the Section 80GGC deduction in my ITR?

The Section 80GGC deduction is entered in Schedule VI-A of ITR-1, ITR-2, ITR-3, or ITR-4 (as applicable), under the heading ‘Deductions under Chapter VI-A’.

Q5. What happens if I made a cash donation to a political party? Can I still claim Section 80GGC?

No. Section 80GGC explicitly bars deductions for cash donations. Only contributions made through banking channels (NEFT, cheque, UPI, demand draft) qualify for the deduction.

Conclusion: Know Your Rights Under Section 80GGC and Claim Them Confidently

The ITAT’s ruling on Section 80GGC deduction disallowance is a powerful reaffirmation of a fundamental principle: in India’s tax system, as in law more broadly, suspicion is not proof. If you have made a legitimate, documented, non-cash contribution to a registered political party and your Assessing Officer disallows the Section 80GGC deduction on vague grounds, you have both the right and the legal precedent to fight back.

What protects you is not complicated it is a receipt, a bank statement, and a correctly filed ITR. If you have those, your Section 80GGC deduction stands on solid ground. If it is still challenged, the appellate route is well-established and, as this ITAT ruling shows, increasingly taxpayer-friendly where documentation is clean.

Claimed a Section 80GGC deduction and received a disallowance notice?

ITRAdvisor.in provides clear, authoritative guidance on all income tax deductions, ITAT rulings, and notice responses. Whether you need to understand your Section 80GGC eligibility, respond to a scrutiny notice, or appeal an unjust disallowance, our resources will walk you through every step.Visit ITRAdvisor.in today — because a legally correct claim deserves a legally correct outcome.

About the Author:

Mukesh Chavan is a dedicated indirect taxation and compliance professional associated with Adwani & Co LLP, specializing in GST advisory, GST audits, GST assessments, and RERA compliance services. With extensive experience in handling complex regulatory matters, he assists businesses in ensuring compliance with evolving GST laws and real estate regulations while minimizing risks and enhancing operational efficiency.

Mukesh has successfully guided clients through GST registrations, return compliance, departmental assessments, audits, litigation support, and tax planning strategies. He also possesses significant expertise in RERA compliance, helping real estate developers, promoters, and stakeholders navigate regulatory requirements and maintain seamless project compliance.

Through his articles and professional insights, Mukesh aims to simplify complex GST and RERA provisions, offering practical guidance that empowers businesses to remain compliant, avoid disputes, and make informed decisions in an increasingly dynamic regulatory environment. His approach combines technical expertise with practical business understanding, enabling clients to focus on growth while meeting their statutory obligations with confidence.

| Not Sure If Your Return Is Clean? If you’re unsure whether your return has been reported correctly, a quick review today can help avoid a much bigger problem later. If you want expert guidance, connect with itradvisor.in today. |

| Need Help Before You File? If you’re a salaried professional, business owner, freelancer, or NRI and want to ensure your ITR matches your AIS and Form 26AS before submission — ITRAdvisor.in is where to start. Visit itradvisor.in for expert tax guidance, AIS reconciliation checklists, and professional support backed by Adwani & Co LLP. |

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.