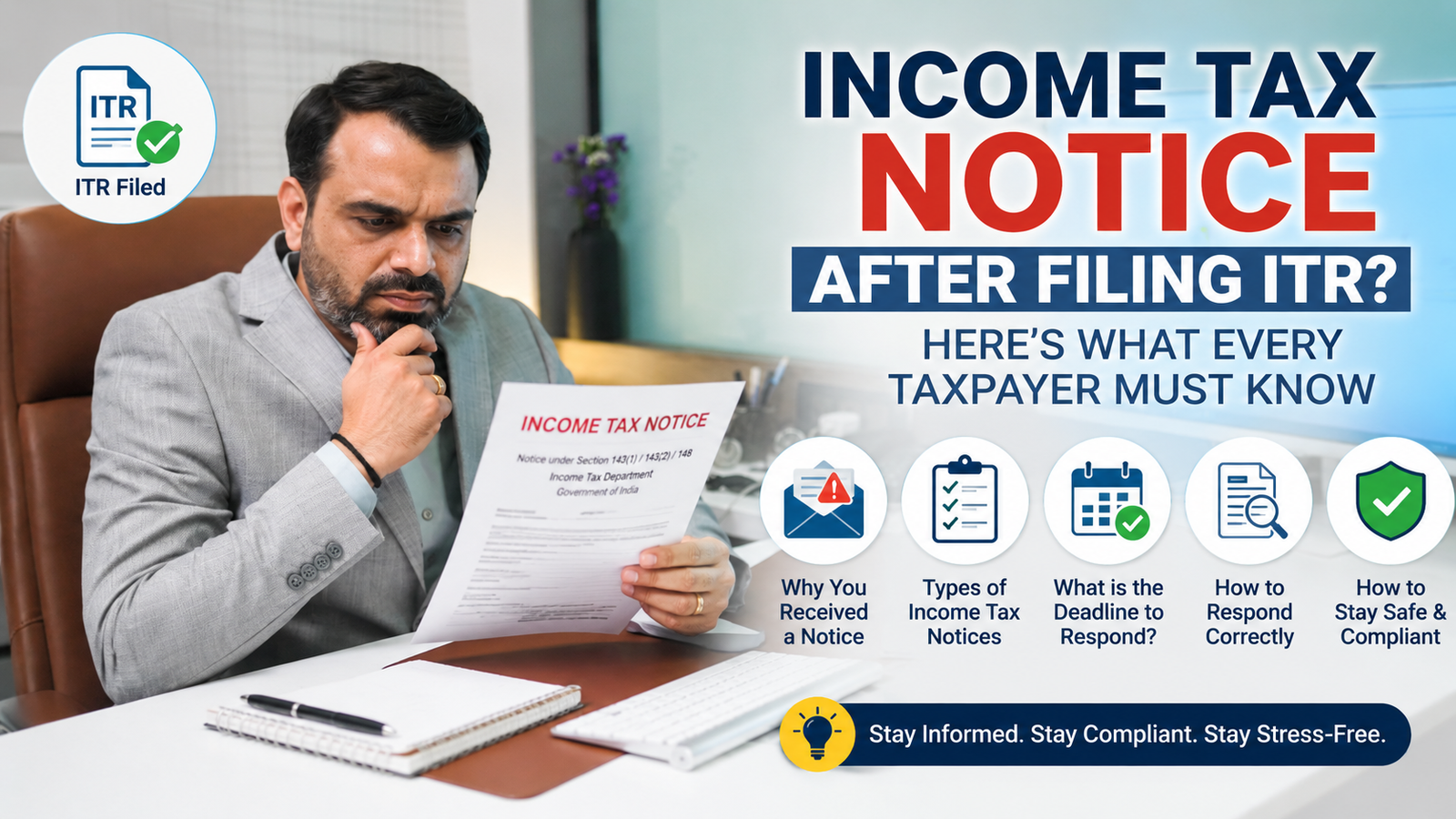

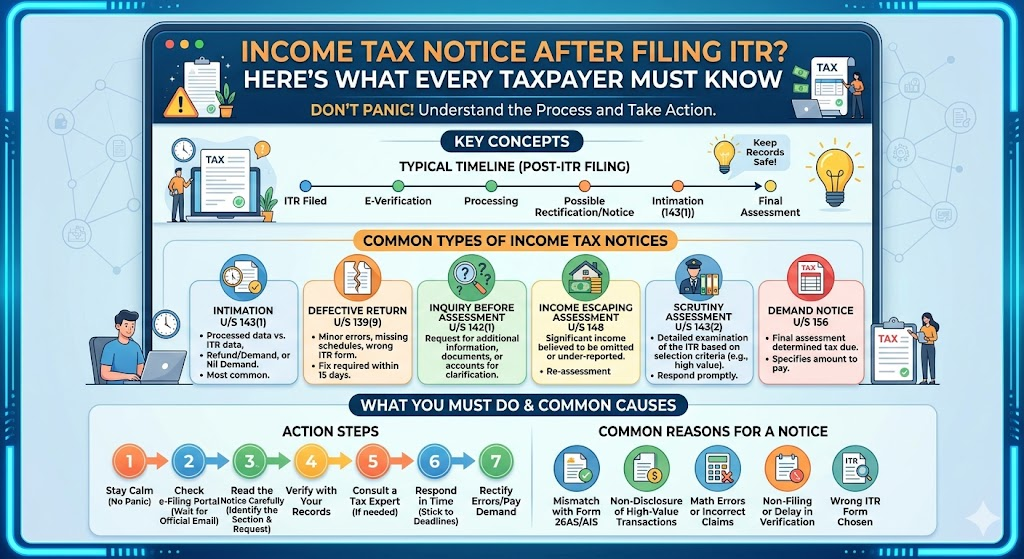

One of the most common questions taxpayers ask after filing their Income Tax Return (ITR) is

“I have already filed my return. Why did I receive an Income Tax Notice?”

Receiving a notice from the Income Tax Department can be stressful. However, a notice does not automatically mean you have done something wrong. In many cases, the notice is simply a request for clarification, additional information, or correction of a mismatch.

Understanding the reason behind the notice and responding appropriately can help avoid unnecessary penalties, interest, and prolonged scrutiny.

In this guide, we explain the most common reasons for receiving an income tax notice after filing your ITR and the steps you should take.

Can You Receive an Income Tax Notice Even After Filing Your Return?

Yes.

Filing your return does not guarantee that the Income Tax Department will not seek further clarification.

The department now uses advanced data analytics, AIS (Annual Information Statement), TIS (Taxpayer Information Summary), SFT reporting, bank transaction data, and employer reporting to verify the accuracy of returns.

Any mismatch or omission can trigger a notice.

Top 7 Reasons Why Taxpayers Receive Income Tax Notices

1. Income Reported in AIS Is Missing in ITR

One of the most common reasons for notices is a mismatch between income reported in AIS and income declared in your return.

Examples:

* Interest income from savings accounts

* Fixed deposit interest

* Dividend income

* Capital gains from shares or mutual funds

* Foreign remittances

Even small omissions can trigger automated compliance checks.

2. High-Value Transactions Reported to the Department

Banks, mutual funds, registrars, and other institutions report specified financial transactions to the Income Tax Department.

Examples include:

* Large cash deposits

* Property purchases

* Significant mutual fund investments

* High credit card spending

* Foreign travel expenses

If your declared income does not support these transactions, the department may seek clarification.

3. Claiming Excess Deductions

Incorrect deduction claims frequently lead to notices.

Common areas include:

* Section 80C

* Section 80D

* Home loan interest

* HRA exemption

* Donations under Section 80G

Taxpayers should retain documentary evidence supporting every deduction claimed.

should be reviewed by a qualified tax professional.

How to Avoid Income Tax Notices in Future

Before filing your return:

✅ Review AIS thoroughly

✅ Match Form 26AS with Form 16

✅ Report all bank interest

✅ Disclose capital gains

✅ Verify deductions

✅ Report foreign assets where applicable

✅ Maintain proper documentation

A careful review before filing can significantly reduce the risk of future notices.

Real-Life Example

A salaried employee earning ₹18 lakh annually filed his return independently.

He reported salary income correctly but forgot to disclose:

* Savings account interest

* Fixed deposit interest

* Dividend income

These entries appeared in AIS but not in the return.

The department later issued a compliance notice seeking clarification.

The issue was resolved through revised reporting, but the taxpayer experienced avoidable stress and delays.

Frequently Asked Questions (FAQs)

1.Is an income tax notice always bad news?

No. Many notices are routine communications seeking clarification or correction.

2.Can I ignore an income tax notice?

No. Every notice should be reviewed and responded to appropriately.

3.How long do I have to respond?

The deadline depends on the specific notice. Always check the notice carefully.

4.Can I revise my return after receiving a notice?

In many situations, corrective action or revised filing may be possible, subject to applicable provisions.

5.Can a CA help me respond to a notice?

Yes. Professional guidance can help ensure accurate and timely compliance.

About Author

Dr. Haresh Adwani holds a PhD in Commerce and brings over 20 years of expertise in GST compliance, income tax advisory, FEMA, and corporate law. Services include GST audit, ITR filing, GST appeal representation, notice response, NRI taxation, and FEMA compliance.

Need Help With an Income Tax Notice?

Received an Income Tax Notice after filing your ITR?

Our team at Adwani & Co. / ITR Advisor assists taxpayers across India with:

* Income Tax Notice Replies

* AIS & TIS Mismatch Review

* Defective Return Notices

* Scrutiny Assessments

* Capital Gains Reporting

* NRI Taxation Issues

* Revised Return Filing

Get your notice reviewed by our experts before responding.

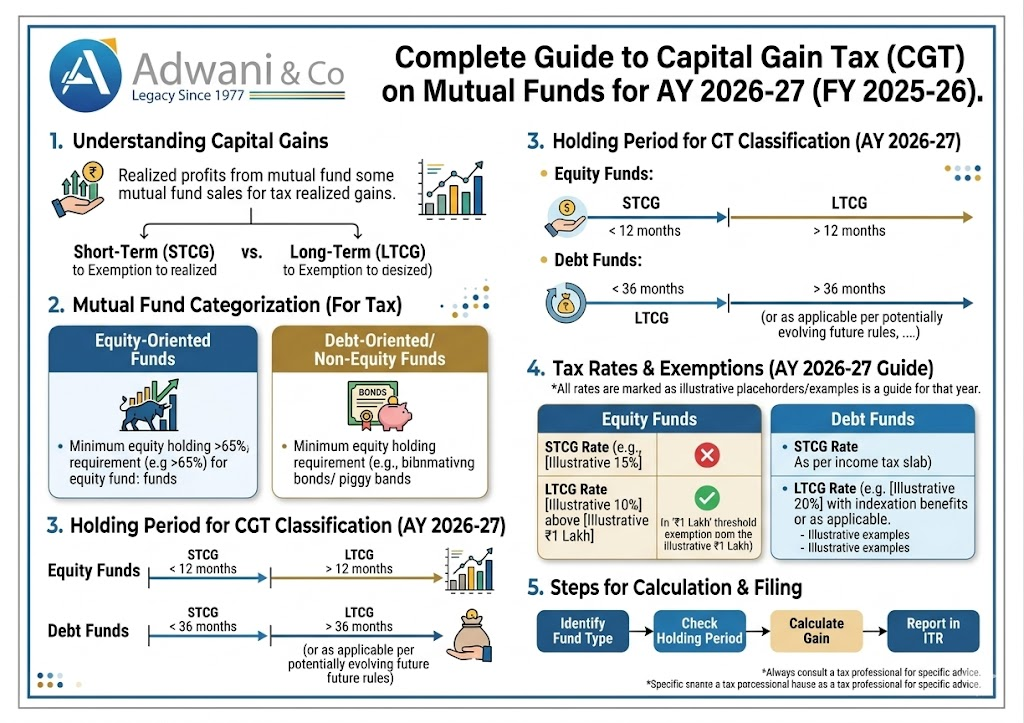

If you have invested in mutual funds and redeemed or switched units during FY 2025-26, capital gains taxation is something you cannot afford to ignore at ITR filing time.

The rules around mutual fund capital gains tax in India have changed significantly over the last two years. The Finance Act 2023 removed the indexation benefit for debt mutual funds. The Finance Act 2024 revised LTCG and STCG rates for equity funds. For AY 2026-27, understanding these updated rules is critical to accurate filing and avoiding income tax notices.

This guide explains the complete taxation framework for mutual fund capital gains covering equity funds, debt funds, hybrid funds, international funds, tax harvesting strategies, ITR reporting, and AIS compliance in plain, practical terms.

What Are Capital Gains on Mutual Funds?

When you redeem, switch, or sell mutual fund units, any profit you earn over your purchase cost (cost of acquisition) is called a capital gain. This gain is taxable under the head ‘Capital Gains’ as per the Income Tax Act, 1961.

Capital gains from mutual funds are classified based on two factors:

Type of fund : equity-oriented or non-equity (debt, international, hybrid)

Holding period : duration from purchase date to redemption date

Importantly, switching between schemes even within the same fund house is treated as a redemption and triggers capital gains. Similarly, receiving units via dividend reinvestment can have cost and holding period implications.

Common misconception: Many investors believe that switching from a growth plan to a direct plan, or from regular to direct, is not taxable. It is. Any switch or transfer of units is a redemption in the eyes of the Income Tax Department and generates capital gains or losses.

Short-Term vs Long-Term Capital Gains: Holding Period Rules

The boundary between short-term capital gains (STCG) and long-term capital gains (LTCG) depends on the type of mutual fund.

Fund Type

Short-Term Holding Period

Long-Term Holding Period

Equity Mutual Funds (equity exposure ≥65%)

12 months or less

More than 12 months

Debt Mutual Funds (equity exposure <35%)

36 months or less (old rule) All periods post Apr 2023

More than 36 months (old rule) No LTCG benefit post Apr 2023

24 months or less (old rule) All periods post Apr 2023

More than 24 months (old rule) No LTCG benefit post Apr 2023

Fund of Funds (domestic equity)

12 months or less

More than 12 months

Gold ETFs / Gold Funds

24 months or less

More than 24 months

Note: Post Finance Act 2023: For debt mutual funds and overseas funds purchased on or after 1 April 2023, there is no distinction between STCG and LTCG all gains are taxed at income tax slab rates regardless of holding period.

Capital Gain Tax Rates on Mutual Funds for AY 2026-27

The Finance Act 2024 revised the capital gains tax rates applicable from 23 July 2024 onwards. These revised rates apply fully to FY 2025-26 returns filed as AY 2026-27.

Equity Mutual Funds (Equity Exposure ≥ 65%)

Gain Type

Holding Period

Tax Rate (AY 2026-27)

Exemption Limit

Short-Term Capital Gain (STCG)

Up to 12 months

20% (flat) + surcharge + cess

Nil

Long-Term Capital Gain (LTCG)

More than 12 months

12.5% (flat) + surcharge + cess

Rs. 1.25 lakh per year (aggregate)

Budget 2024 Change: STCG rate on equity was raised from 15% to 20%. LTCG rate was raised from 10% to 12.5%. The exemption limit was raised from Rs. 1 lakh to Rs. 1.25 lakh. These changes apply to transactions on or after 23 July 2024.

Debt Mutual Funds (Post 1 April 2023 Purchases)

Purchase Date

Tax Treatment

Applicable Rate

Purchased before 1 April 2023 (held >36 months)

LTCG with indexation

20% with indexation benefit

Purchased before 1 April 2023 (held ≤36 months)

STCG

Income tax slab rate

Purchased on or after 1 April 2023 (any holding period)

Taxed as ordinary income

Income tax slab rate (no indexation, no LTCG benefit)

Note: The Finance Act 2023 removed the LTCG benefit and indexation for debt mutual funds purchased on or after 1 April 2023. This fundamentally changed debt fund tax efficiency versus fixed deposits.

Hybrid & Other Fund Categories

Fund Category

Equity Exposure

STCG Rate

LTCG Rate

Indexation

Aggressive Hybrid (≥65% equity)

≥65%

20%

12.5% above Rs. 1.25L

No

Conservative Hybrid / Debt-oriented Hybrid

<35% equity

Slab rate

Slab rate (post Apr 2023)

No (post Apr 2023)

Balanced Advantage Fund (35-65% equity)

35-65%

20% or slab

12.5% or slab

Depends on equity exposure

International / Overseas Funds

Foreign equity

Slab rate

Slab rate (post Apr 2023)

No (post Apr 2023)

Gold ETF / Gold Fund

No equity

Slab rate (≤24 months)

12.5% (>24 months, no indexation post 2024)

No (post 2024)

Fund of Funds – Domestic Equity

≥90% in equity MFs

20%

12.5% above Rs. 1.25L

No

What Is Indexation Benefit and Who Can Still Claim It?

Indexation allows you to inflate your purchase cost using the Cost Inflation Index (CII) notified by the Income Tax Department each year. This reduces your effective capital gain and therefore your tax liability.

Post the Finance Act 2024 amendments, indexation for most asset classes has been modified. For mutual funds specifically:

Equity mutual funds: Never had indexation benefit tax at flat rates

Debt mutual funds purchased before 1 April 2023 and held for more than 36 months: LTCG with indexation at 20% still applies grandfathered treatment

Debt mutual funds purchased on or after 1 April 2023: No indexation, taxed at slab rates regardless of holding

Gold funds and FoFs: Post Finance Act 2024, the 20% with indexation benefit for long-term gains has been replaced with 12.5% without indexation

Asset Class

Pre-1 April 2023 Purchases (Long-term)

Post-1 April 2023 Purchases

Debt Mutual Funds

20% with indexation (LTCG >36 months)

Slab rate, no indexation

International Funds

20% with indexation (LTCG >36 months)

Slab rate, no indexation

Gold ETF / Gold Funds

20% with indexation (LTCG >24 months)

12.5% without indexation (LTCG >24 months)

Equity Mutual Funds

12.5% without indexation (LTCG >12 months)

12.5% without indexation (LTCG >12 months)

Exemptions Available on Mutual Fund Capital Gains

Rs. 1.25 Lakh LTCG Exemption on Equity Funds

Under Section 112A of the Income Tax Act, 1961, long-term capital gains from equity-oriented mutual funds are exempt up to Rs. 1.25 lakh per financial year (aggregate across all equity assets including equity MFs, equity shares, equity ETFs, and units of business trusts).

Only gains exceeding Rs. 1.25 lakh are taxed at 12.5% (without indexation).

Example: If your total LTCG from equity mutual funds and direct equity shares combined is Rs. 2 lakh in FY 2025-26, your taxable LTCG is Rs. 75,000 (Rs. 2L minus Rs. 1.25L), taxed at 12.5% = Rs. 9,375.

Section 54F: Capital Gain Exemption on Reinvestment in Residential Property

If you redeem any long-term capital asset (including mutual fund units classified as long-term, other than a residential house) and reinvest the net consideration in purchasing or constructing a residential house property, you may claim exemption under Section 54F.

This is particularly useful for investors planning to deploy mutual fund redemption proceeds into real estate.

Section 54EE and 54EC: Bonds

Long-term capital gains from mutual funds may also qualify for exemption under Section 54EC by reinvesting up to Rs. 50 lakh in specified NHAI or REC bonds within 6 months of the sale.

Tax Loss Harvesting: A Practical Strategy for Mutual Fund Investors

Tax loss harvesting is a strategy where investors intentionally redeem loss-making mutual fund units before the financial year end (March 31) to book losses, which can then be set off against existing capital gains to reduce tax liability.

How Set-Off Rules Work Under the Income Tax Act

Type of Loss

Can Be Set Off Against

Carry Forward Period

Short-Term Capital Loss (STCL)

STCG or LTCG (any asset)

8 years

Long-Term Capital Loss (LTCL)

LTCG only (same or different asset)

8 years

Business Loss

Business income only (not capital gains)

8 years

Speculative Loss

Speculative income only

4 years

Key Insight: You can set off your short-term capital losses from poorly performing debt funds against long-term capital gains from equity funds. This cross-asset, cross-category set-off is allowed under the Income Tax Act and is a powerful planning tool.

Tax Harvesting in Practice: Example

Situation: Aditya has LTCG of Rs. 3 lakh from equity mutual funds in FY 2025-26. He also has STCL of Rs. 1.5 lakh from an international fund that has underperformed.

Taxable LTCG before set-off = Rs. 3 lakh

Less: LTCG exemption = Rs. 1.25 lakh

Taxable LTCG after exemption = Rs. 1.75 lakh

Less: STCL set-off = Rs. 1.5 lakh

Net taxable LTCG = Rs. 25,000

Tax at 12.5% = Rs. 3,125 (versus Rs. 21,875 without harvesting)

AIS, Form 26AS and Mutual Fund Capital Gains: Reporting Obligations

The Annual Information Statement (AIS) on the Income Tax portal now captures all mutual fund transactions reported by RTAs (Registrar and Transfer Agents) such as CAMS and KFintech. This includes purchases, redemptions, switches, SIP and SWP transactions, and dividend payouts.

Why AIS Mismatches in Mutual Funds Are a Common Notice Trigger

If your ITR does not reflect the capital gains shown in your AIS, the Income Tax Department’s automated system flags this discrepancy. This is one of the most common reasons salaried individuals who also have mutual fund investments receive notices under Section 143(1)(a) or Section 142(1).

Common causes of AIS mismatch for mutual fund investors:

Not reporting gains from old folio numbers or dormant accounts

Switching between direct and regular plans without reporting the resulting gain

Not accounting for reinvested dividends (growth option vs IDCW option confusion)

Not including gains from ELSS fund redemptions after 3-year lock-in

Joint holding gains reported under the first holder’s PAN in AIS

How to Download Your Capital Gain Statement

Log in to CAMS (camsonline.com) or KFintech (kfintech.com) with your PAN and email

Navigate to ‘Capital Gain Statement’ under the Reports section

Select the financial year FY 2025-26 (1 April 2025 to 31 March 2026)

Download the statement and verify it matches your AIS on incometax.gov.in

For SIPs, each SIP instalment has a different purchase date and cost ensure all are captured

Which ITR Form to Use for Mutual Fund Capital Gains in AY 2026-27?

Taxpayer Profile

Correct ITR Form

Salaried with only equity MF LTCG (no other capital assets, LTCG ≤Rs. 1.25L)

ITR-1 (Sahaj) — if total income ≤Rs. 50L

Salaried with any capital gains (STCG or LTCG exceeding basic limits)

ITR-2

Business income + capital gains from MFs

ITR-3

Presumptive taxation professionals (44ADA) + capital gains from MFs

ITR-3 (not ITR-4, since ITR-4 cannot report capital gains)

NRI with Indian mutual fund redemptions

ITR-2

Company or LLP

ITR-6 or ITR-5 as applicable

How to Report Mutual Fund Capital Gains in ITR-2

Go to Schedule CG (Capital Gains) in ITR-2

Equity MF LTCG report under ‘Section 112A’ in Schedule 112A (scrip-wise details required)

Equity MF STCG report under ‘Section 111A’

Debt MF / other MF gains report under ‘Short-Term Capital Gains taxable at applicable rate’ or LTCG under Section 112

Set-off and carry forward report in Schedule CYLA, BFLA, and CFL

Use the pre-filled data but always verify against your capital gain statement

TDS on Mutual Fund Redemptions and Dividends

TDS on Mutual Fund Dividends (IDCW)

Under Section 194K of the Income Tax Act, mutual fund houses deduct TDS at 10% on dividend (IDCW) income paid to resident individuals if the aggregate dividend in a financial year exceeds Rs. 5,000. This TDS is reflected in Form 26AS and AIS.

TDS on Redemptions by NRIs

For NRI investors, mutual fund redemptions attract TDS as follows:

Fund Type

STCG TDS Rate for NRI

LTCG TDS Rate for NRI

Equity Mutual Funds

20% (was 15% pre-Budget 2024)

12.5% (above Rs. 1.25L exemption)

Debt Mutual Funds (post Apr 2023)

Slab rate / 30% for NRIs

No separate LTCG — slab rate

Other Non-Equity Funds

Applicable slab rate / 30%

20% with indexation (pre-Apr 2023 purchases)

The Grandfathering Rule: Equity Mutual Funds Held Before 31 January 2018

When the government reintroduced LTCG tax on equity mutual funds through the Finance Act 2018, it provided a grandfathering benefit. Gains accrued in equity mutual funds up to 31 January 2018 were protected from taxation.

If you are still holding equity mutual fund units purchased before 31 January 2018, your cost of acquisition for tax purposes is the higher of:

Your actual purchase price

The NAV (Net Asset Value) of the fund on 31 January 2018

This effectively means that all gains up to 31 January 2018 are tax-free under LTCG. Only gains post that date are taxable at 12.5%.

If you have very old mutual fund folios with units purchased before 2018, your capital gain statement will reflect this grandfathering cost automatically. Ensure your ITR filing uses the correct grandfathered cost basis.

ELSS Mutual Funds: Tax Deduction + Capital Gains Taxation

Equity Linked Savings Schemes (ELSS) offer a dual tax benefit deduction under Section 80C (up to Rs. 1.5 lakh) on investment, and long-term capital gains treatment on redemption after the mandatory 3 year lock in.

Aspect

ELSS Details

Lock-in period

3 years from each SIP instalment date

Section 80C deduction

Up to Rs. 1.5 lakh per year (under old tax regime only)

LTCG tax rate on redemption

12.5% above Rs. 1.25 lakh (same as equity funds)

STCG possibility

No lock-in ensures minimum 3-year holding (>12 months = LTCG)

Reporting in ITR

Schedule 112A under Capital Gains scrip-wise detail needed

Applicable ITR form

ITR-2 or ITR-3 (not ITR-1 or ITR-4)

80C deduction new regime

Not available Section 80C deductions not applicable under new tax regime

Common Mistakes Mutual Fund Investors Make in ITR Filing

Filing ITR-1 or ITR-4 despite having capital gains from mutual funds leads to defective return notice

Not reporting ELSS redemptions treated as income not disclosed, can trigger scrutiny

Not matching AIS with capital gain statement before filing AIS mismatches trigger Section 143(1)(a) notices

Missing gains from SWP (Systematic Withdrawal Plans) each SWP withdrawal is a partial redemption taxable as capital gain

Ignoring dividend (IDCW) income taxable at slab rate, must be reported under ‘Income from Other Sources’

Not reporting losses losses eligible for carry forward are forfeited if not claimed in ITR

Treating all mutual fund gains as LTCG STCG from equity funds held under 12 months is taxed at 20%, not 12.5%

Not accounting for SIP-wise holding period each SIP instalment has its own purchase date; gains from instalments held <12 months are STCG

Practical Examples: Calculating Mutual Fund Capital Gains Tax for AY 2026-27

Example 1 : Salaried Investor with Equity MF Redemption

Ramesh is a salaried individual earning Rs. 10 lakh per year. In FY 2025-26, he redeemed equity mutual fund units with total LTCG of Rs. 2 lakh and STCG of Rs. 30,000.

Capital Gain Component

Amount

Tax Rate

Tax Payable

LTCG from equity MFs

Rs. 2,00,000

12.5% above Rs. 1.25L exemption

Rs. 9,375 on Rs. 75,000

STCG from equity MFs

Rs. 30,000

20%

Rs. 6,000

Total MF Capital Gain Tax

Rs. 15,375

Example 2 : Debt Fund Investor (Post April 2023 Purchase)

Sunaina purchased debt mutual fund units in June 2023 for Rs. 5 lakh. She redeemed them in December 2025 for Rs. 5.8 lakh (gain of Rs. 80,000). She falls in the 30% tax bracket.

No LTCG benefit purchased after 1 April 2023

No indexation benefit

Rs. 80,000 added to total income and taxed at 30% slab = Rs. 24,000

Had she purchased this before 1 April 2023 and held for >36 months LTCG with indexation at 20% could have been applicable

Example 3 : SIP with Mixed LTCG and STCG

Priya runs a monthly SIP of Rs. 10,000 in an aggressive hybrid fund (equity ≥65%) since April 2023. She redeemed all units in May 2025.

SIP instalments from April 2023 to April 2024 (13 months or more by May 2025): LTCG at 12.5%

SIP instalments from May 2024 to April 2025 (held <12 months by May 2025): STCG at 20%

Her capital gain statement from CAMS will split this automatically she should not manually aggregate

Debt mutual funds purchased after 1 April 2023: taxed at slab rates no LTCG, no indexation benefit

Debt funds purchased before 1 April 2023: LTCG with indexation at 20% still applicable if held >36 months

Switch, SWP, and plan change transactions are taxable redemption events often missed by investors

Tax loss harvesting before 31 March can significantly reduce net capital gains tax liability

Short-term losses from any capital asset can be set off against both STCG and LTCG

AIS on the Income Tax Portal captures all MF transactions mismatches trigger notices

File ITR-2 or ITR-3 for capital gains not ITR-1 or ITR-4

NRIs face TDS at source on MF redemptions and must file ITR to claim excess TDS refunds

For SIP investments, each instalment has its own holding period and cost use the capital gain statement from CAMS/KFintech

Frequently Asked Questions (FAQs)

Q1. What is the LTCG tax rate on equity mutual funds for AY 2026-27?

Long-term capital gains from equity mutual funds for AY 2026-27 are taxed at 12.5% (without indexation) on gains exceeding Rs. 1.25 lakh in a financial year. This rate was revised upward from 10% by the Finance Act 2024, effective from 23 July 2024. LTCG up to Rs. 1.25 lakh is fully exempt.

Q2. What is the STCG tax rate on equity mutual funds for AY 2026-27?

Short-term capital gains from equity mutual funds where units are held for 12 months or less are taxed at a flat rate of 20% under Section 111A of the Income Tax Act. The Finance Act 2024 revised this rate from 15% to 20%, applicable from 23 July 2024.

Q3. Is there any exemption on capital gains from equity mutual funds?

Yes. Under Section 112A, LTCG from equity-oriented mutual funds is exempt up to Rs. 1.25 lakh per financial year in aggregate (including gains from equity shares, equity mutual funds, and equity ETFs). Only the amount exceeding Rs. 1.25 lakh is taxed at 12.5%. There is no exemption for STCG from equity mutual funds.

Q4. Is dividend (IDCW) from mutual funds taxable?

Yes. Dividend income from mutual funds now called IDCW (Income Distribution cum Capital Withdrawal) is taxable in the hands of the investor at their applicable income tax slab rate under ‘Income from Other Sources’. Mutual fund houses deduct TDS at 10% under Section 194K if aggregate dividend in a financial year exceeds Rs. 5,000 for resident individuals. This TDS appears in Form 26AS.

Q5. How are NRI investments in Indian mutual funds taxed?

NRIs with investments in Indian mutual funds are subject to the same capital gains tax rates as resident investors, but TDS is deducted at source by the mutual fund house. For equity funds, TDS on STCG is 20% and on LTCG is 12.5%. For debt funds, TDS is at applicable rates. NRIs should file their Indian ITR to reconcile actual tax liability against TDS deducted and claim refunds if excess TDS has been deducted.

Conclusion:

Mutual fund capital gains taxation in India has gone through some of its most significant changes in recent memory the Finance Act 2023 and Finance Act 2024 together rewrote the rules for both equity and debt funds. For AY 2026-27, investors need to be particularly careful about the revised LTCG and STCG rates for equity funds, the slab-rate treatment of new debt fund investments, and the correct ITR form to use.

The good news is that with proper planning tax loss harvesting, use of the Rs. 1.25 lakh LTCG exemption, set-off of losses, and timely filing the overall tax outgo from mutual fund investments can be optimised legally.

The starting point is always the capital gain statement from your RTA (CAMS or KFintech), reconciled carefully against your AIS. Do this before your ITR filing, not after a notice arrives.

File on time, report accurately, and claim every benefit you are entitled to. If your portfolio has multiple fund types, SIPs, and switches, professional guidance ensures you don’t leave money on the table — or face unnecessary scrutiny.

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

bout the Author Dr. Haresh Adwani Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra.

Every year, lakhs of Indian taxpayers scramble to file their Income Tax Returns just before the deadline. Some miss it. And that’s when things get complicated.

Missing the ITR filing deadline for AY 2026-27 isn’t just an administrative lapse it has real financial consequences. From a late filing fee under Section 234F to interest under Section 234A, the cost of delay adds up quickly. There’s also the risk of income tax notices, loss of refunds, and the permanent loss of certain tax benefits.

Whether you’re a salaried employee, freelancer, business owner, or NRI, this guide covers everything you need to know about the late filing penalty for AY 2026-27.

What Is the ITR Filing Due Date for AY 2026-27?

The Assessment Year (AY) 2026-27 corresponds to income earned during the Financial Year (FY) 2025-26 from 1 April 2025 to 31 March 2026.

For most individual taxpayers including salaried employees, freelancers, and small businesses not subject to tax audit the standard due date for filing an ITR is 31 July of the assessment year.

So for AY 2026-27, the general due date is 31 July 2026.

Taxpayer Category

ITR Filing Due Date (AY 2026-27)

Salaried Individuals & HUFs (no audit)

31 July 2026

Businesses requiring tax audit (Section 44AB)

31 October 2026

Companies requiring audit

31 October 2026

Transfer pricing cases (Section 92E)

30 November 2026

Revised Return

31 December 2026

Belated / Late Return (Section 139(4))

31 December 2026

Important: Due dates are subject to CBDT notifications and extensions. Always verify the latest notification on the Income Tax India portal or ITRAdvisor.in before filing.

What Is Section 234F? Late Filing Fee Explained

Section 234F was inserted into the Income Tax Act, 1961, with effect from AY 2018-19. It introduced a mandatory late filing fee for taxpayers who miss the due date but still want to file a belated return.

Before Section 234F, there was no direct fee for late filing only interest. The section was introduced to encourage timely compliance.

Section 234F Late Filing Fee Structure for AY 2026-27

Filing Date

Total Income Above Rs. 5 Lakh

Total Income Up to Rs. 5 Lakh

On or before 31 July 2026 (due date)

NIL

NIL

After 31 July 2026 up to 31 Dec 2026

Rs. 5,000

Rs. 1,000

After 31 December 2026 (if extended)

Rs. 5,000

Rs. 1,000

Key Point: Even if your tax liability is zero or you are eligible for a full refund, the late filing fee under Section 234F still applies unless your total income is below the basic exemption limit (i.e., below Rs. 3 lakh under the new regime for FY 2025-26).

Who Is Exempt from Section 234F Late Filing Fee?

Individuals whose total income is below the basic exemption limit

Individuals not required to file ITR under the law (though voluntary filing is advisable)

Returns filed within the prescribed due date

Section 234A : Interest on Late Filing When Tax Is Due

Section 234F is a fee. But if you also have unpaid tax liability at the time of filing, you will additionally be charged interest under Section 234A of the Income Tax Act.

How Is Section 234A Interest Calculated?

Rate: 1% simple interest per month or part of a month

Calculated on the outstanding tax payable (i.e., tax due minus TDS, advance tax, and self-assessment tax paid)

Period: From the day after the due date till the date of actual filing or payment

Example: If you file your ITR on 30 September 2026 (due date 31 July 2026) with Rs. 50,000 outstanding tax, you will pay 2 months of 234A interest = Rs. 1,000. Plus Rs. 5,000 under Section 234F. Total additional outgo: Rs. 6,000.

Section 234B and 234C: Additional Interest Traps

If you are required to pay advance tax but haven’t paid it correctly, you may also face:

Section 234B –:Interest for default in payment of advance tax (if advance tax paid is less than 90% of the total tax liability)

Section 234C Interest for deferment of advance tax instalments

Section

Nature of Default

Interest Rate

Calculation Period

234A

Late ITR filing with outstanding tax

1% per month

Due date to actual filing date

234B

Advance tax less than 90% of tax due

1% per month

1 April to date of filing

234C

Underestimated advance tax instalments

1% per month

Per each instalment default

Beyond Penalty: Other Consequences of Late ITR Filing

1. Loss of Carry Forward of Losses

2. Delay in Income Tax Refund

3. Inability to Revise the Return

4. Difficulty in Loan Approvals and Visa Applications

5. Income Tax Notices for Non-Filing

What Is a Belated Return? Can You Still File After the Deadline?

Yes. If you miss the 31 July 2026 due date, you can still file a belated return under Section 139(4) of the Income Tax Act, 1961 up to 31 December 2026.

A belated return carries the Section 234F fee and applicable interest. However, it is far better to file a belated return than not to file at all.

What You Can and Cannot Do in a Belated Return

Feature

Original Return (by 31 Jul 2026)

Belated Return (by 31 Dec 2026)

Filing allowed

Yes

Yes

Late filing fee (Section 234F)

Nil

Rs. 1,000 or Rs. 5,000

Carry forward of capital/business losses

Allowed

NOT Allowed

Claim deductions u/s 80C, 80D, etc.

Allowed

Allowed

Revision of return u/s 139(5)

Allowed (up to 31 Dec 2026)

Allowed (up to 31 Dec 2026)

Refund claim

Allowed

Allowed (but may be delayed)

Practical Examples: How the Penalty Adds Up

Example 1 : Salaried Employee, No Outstanding Tax

Rajan is a salaried employee with total income of Rs. 8 lakh. His full tax has been deducted at source by his employer. He forgets to file his ITR and files it on 15 September 2026.

Section 234F fee: Rs. 5,000 (income above Rs. 5 lakh, filed after 31 July 2026)

Section 234A interest: Nil (no outstanding tax payable)

Total additional payment: Rs. 5,000

Example 2 : Freelancer with Outstanding Tax

Priya is a freelancer with total income of Rs. 12 lakh and advance tax of Rs. 40,000 paid. Total tax liability is Rs. 1,20,000. She files her return on 1 October 2026.

Outstanding tax = Rs. 80,000

Section 234F fee = Rs. 5,000

Section 234A interest = 2 months x 1% x Rs. 80,000 = Rs. 1,600

Total additional payment = Rs. 6,600

Plus: she cannot carry forward any capital losses (if applicable)

Example 3 – Low Income Taxpayer

Sunita is a retired individual with pension income of Rs. 4.5 lakh. She files her return on 20 August 2026.

How to Avoid Late Filing Penalties: A Practical Checklist

Collect all income documents : Form 16, Form 16A, rental agreements, freelance invoices

Download and reconcile your AIS (Annual Information Statement) from the Income Tax Portal

Verify TDS credit in Form 26AS matches your actual tax deductions

Calculate advance tax liability if you have income beyond salary (freelance, rent, capital gains)

Identify the correct ITR form for your income type

File on or before 31 July 2026 to avoid Section 234F fee

If you discover any errors post-filing, file a revised return by 31 December 2026

If you have capital losses or business losses, timely filing is non-negotiable

NRI Taxpayers: Special Note on Late Filing

Non-Resident Indians (NRIs) with income arising in India rent, capital gains from sale of property or securities, interest from NRO accounts are also required to file ITR if their Indian income exceeds the basic exemption limit.

For NRIs, the same Section 234F fee applies if the return is filed late. Additionally, NRIs dealing with property transactions often receive TDS at higher rates (such as 20%+ on LTCG). If they fail to file returns, excess TDS deducted cannot be claimed as refund.

If you are an NRI who sold property in India in FY 2025-26, filing your ITR on time is critical to reclaiming excess TDS. A late return not only delays the refund but also attracts Section 234F fee.

NRIs should also be aware of the 120day rule those who visit India for 120 days or more and whose Indian income exceeds Rs. 15 lakh may be classified as Resident but Not Ordinarily Resident (RNOR), which has separate filing obligations.

File your ITR for AY 2026-27 by 31 July 2026 to avoid late filing fee under Section 234F

Late filing fee is Rs. 5,000 for income above Rs. 5 lakh and Rs. 1,000 for income up to Rs. 5 lakh

Section 234A interest applies at 1% per month on unpaid taxes from the due date to the filing date

Capital losses and business losses cannot be carried forward if the return is filed late

Belated returns (up to 31 December 2026) are better than no return at all

NRIs must also file returns on time to avoid penalties and claim excess TDS refunds

Even nil-tax returns should be filed on time for compliance, refund claims, and loan documentation

Frequently Asked Questions (FAQs)

Q1. What is the last date to file ITR for AY 2026-27?

The last date for filing the original ITR for most individuals (salaried, freelancers, non-audit cases) is 31 July 2026. For belated returns, the deadline is 31 December 2026. Dates may be extended by CBDT via official notification.

Q2. Is Section 234F applicable if there is no tax liability?

Yes. Section 234F applies based on whether the return is filed after the due date it is not linked to tax liability. However, if your total income is below the basic exemption limit no fee applies.

Q3. Can I carry forward capital losses if I file the return late?

No. If you file your return after the due date, capital losses (both STCG and LTCG losses) and business losses cannot be carried forward to future years. This is one of the most significant financial consequences of late filing.

Q4. Is there any penalty for non-filing of ITR (not even a belated return)?

Yes. Under Section 276CC of the Income Tax Act, willful failure to file an ITR is a criminal offence result ing in imprisonment ranging from 3 months to 2 years, with possible extension to 7 years in cases of significant tax evasion. Additionally, the Assessing Officer can also impose a penalty, which can result in a higher tax demand.

Q5. Can I file an ITR after 31 December 2026?

After 31 December 2026, the window for filing a belated return for AY 2026-27 generally closes. However, in certain circumstances may be required or permitted to file a late return. For updating income post-assessment, you may use an Updated Return within two years from the end of the relevant assessment year.

Conclusion: File On Time — There Is No Good Reason to Delay

The late filing penalty for AY 2026-27 is not just about the Rs. 5,000 fee. It’s about losing carry-forward benefits that could save you thousands of rupees in future taxes. It’s about delayed refunds that you are rightfully entitled to. It’s about the risk of notices that create unnecessary stress and professional fees.

The income tax system in India is increasingly data-driven. With AIS capturing your bank transactions, mutual fund purchases, property deals, and more — there is very little that the Income Tax Department does not know. Filing your return accurately and on time is no longer just an option. It’s the only sensible financial decision.

If you are unsure about which ITR form to use, how to reconcile your AIS, or whether you have any outstanding tax liability — seek professional guidance well before 31 July 2026. The cost of advice is always less than the cost of a penalty.

The late filing penalty for AY 2026-27 is not just about the Rs. 5,000 fee. It’s about losing carry-forward benefits that could save you thousands of rupees in future taxes. It’s about delayed refunds that you are rightfully entitled to. It’s about the risk of notices that create unnecessary stress and professional fees.

The income tax system in India is increasingly data driven. With AIS capturing your bank transactions, mutual fund purchases, property deals, and more there is very little that the Income Tax Department does not know. Filing your return accurately and on time is no longer just an option. It’s the only sensible financial decision.

About the Author Dr. Haresh Adwani Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

Imagine filing your income tax return confidently only to receive a notice three months later saying your reported income does not match what the Income Tax Department already knows. This is exactly what happens when taxpayers skip reviewing their Annual Information Statement (AIS) before filing ITR.

The AIS is not just another document on the Income Tax e-filing portal. It is the government’s comprehensive financial dossier on you capturing every significant transaction linked to your PAN,

In this complete guide, the tax professionals at Adwani and Company led by Dr. Haresh Adwani, PhD in Commerce and a qualified law graduate walk you through exactly how to download AIS from the Income Tax portal, how to open the password protected AIS PDF, how to interpret it, and why reconciling AIS before filing your ITR for AY 2026-27 could save you from costly income tax notices.

What Is the Annual Information Statement (AIS) and Why Does It Matter for ITR Filing?

The Annual Information Statement, commonly referred to as AIS, was introduced by the Income Tax Department of India to give taxpayers a consolidated, transparent view of all financial information that the department has collected about them from various reporting entities banks, brokers, mutual fund houses, registrars, employers, GST authorities, and more.

Before the introduction of AIS, taxpayers relied primarily on Form 26AS for TDS-related data. AIS goes several steps further it is a far more expansive document that captures the full spectrum of your financial activity throughout the financial year.

What Information Does AIS Contain?

AIS captures the following key categories of information:

Salary income as reported by your employer

Interest income from savings accounts, fixed deposits, recurring deposits, and bonds

Dividend income from shares and mutual funds

Capital gains from sale of equity shares, mutual fund units, debt instruments, and real estate

Purchase and sale transactions of immovable property

Mutual fund purchase and redemption details

Foreign remittances sent or received under LRS (Liberalised Remittance Scheme)

GST turnover figures for registered businesses

High-value cash deposits or withdrawals

TDS and TCS data (which also appears in Form 26AS)

Rent paid or received above prescribed thresholds

Cryptocurrency and virtual digital asset (VDA) transactions

Expert Insight: “The AIS has transformed how the Income Tax Department tracks compliance. Every mismatch between your filed return and your AIS is a potential trigger for a Section 143(1)(a) intimation or a full scrutiny notice. Reviewing AIS before filing ITR is no longer optional — it is essential,” says Dr. Haresh Adwani, Founder of Adwani and Company.

AIS vs Form 26AS vs TIS Key Differences Every Taxpayer Must Know Before Downloading

Many taxpayers confuse AIS with Form 26AS or are unsure about the Tax Information Summary (TIS). Here is a clear breakdown:

Feature

Form 26AS

AIS (Annual Information Statement)

TIS (Tax Information Summary)

Scope

TDS, TCS, and advance tax only

Full financial transactions across all sources

Derived summary from AIS with taxpayer feedback

Introduced

2002

2021

2021

Capital Gains

❌ Not included

✅ Included

✅ Included

Crypto / VDA

❌ Not included

✅ Included

✅ Included

GST Turnover

❌ Not included

✅ Included

✅ Included

Who Should Use

Basic TDS verification

Complete pre-ITR reconciliation

Final verified income summary

In short: for AY 2026-27, always start with AIS, cross-check it against Form 26AS, review the TIS for any feedback you may have submitted, and only then proceed to file your income tax return.

How to Download AIS from the Income Tax Portal – Complete Step-by-Step Process

Downloading your Annual Information Statement from the Income Tax e-filing portal takes under five minutes if you know the right steps. Follow this exact process:

#

Action

What to Do / Where to Click

1

Visit the Portal

Open your browser and go to the official Income Tax e-filing portal: incometax.gov.in

2

Log In with PAN

Click ‘Login’ at the top right. Enter your PAN as your User ID, along with your password and the captcha code.

3

Navigate to Services

On the dashboard, click on the ‘Services’ tab in the top navigation menu.

4

Click on AIS

From the dropdown under Services, select ‘Annual Information Statement (AIS)’. You will be redirected to the AIS portal (compliance.insight.gov.in).

5

Select Financial Year

On the AIS portal, select the relevant Financial Year — FY 2025-26 for AY 2026-27 — from the dropdown menu.

6

Choose Your Format

You can download AIS in two formats: PDF (for easy reading) or JSON (for data processing). For individual review, select PDF.

7

Download and Open

Click Download. Once downloaded, open the PDF. It will prompt you for a password.

8

Enter the Password

The AIS PDF password is: [PAN in lowercase] + [Date of Birth in DDMMYYYY format]. Example: if PAN is ABCDE1234F and DOB is 15-August-1985, the password is abcde1234f15081985.

How to Download TIS (Tax Information Summary) from the AIS Portal

On the AIS portal, go to the ‘TIS’ tab (next to ‘AIS’).

Select the Financial Year.

Click Download → select PDF or JSON.

The TIS PDF uses the same password format as AIS: PAN (lowercase) + DOB (DDMMYYYY).

The TIS is particularly useful when the department processes your ITR and computes pre-filled data it uses TIS figures as the reference point for any automated intimations.

Why Reviewing AIS Is Critical Before Filing Your ITR for AY 2026-27

1. Catch Income the Department Already Knows About

Every bank, mutual fund house, stock broker, property registrar, and company that deducts TDS from your payments is required to report this information to the Income Tax Department. If they have reported income linked to your PAN and you do not include it in your ITR the department’s automated system will flag the mismatch immediately.

2. Identify Errors in Reported Data

AIS data is not always correct. Banks sometimes report interest income for the wrong PAN. Brokers may report capital gains figures that differ from your actual gains due to corporate actions. If you find incorrect entries in your AIS, you can submit feedback directly on the AIS portal, marking the entry as ‘Incorrect’ or ‘Not relating to me’. This feedback is reflected in your TIS.

3. Avoid Defective Return Notices and Scrutiny

The Income Tax Department’s automated processing system compares your filed ITR with your AIS/TIS data. Any significant discrepancy whether it is unreported mutual fund redemptions, omitted interest income, or missing property sale consideration — may result in an intimation under Section 143(1)(a) or even a scrutiny notice under Section 143(2), explains Dr. Haresh Adwani of Adwani and Company.

4. Claim Accurate TDS Credit

AIS also reflects TDS entries from multiple sources — salary TDS (Form 16), bank TDS on FD interest, TDS on professional fees, rent TDS, and more. Cross-checking AIS with your Form 26AS ensures you claim all available TDS credit and do not leave money on the table.

Learn more about our Income Tax Filing and TDS Compliance Services for salaried professionals and business owners.

Real-Life Example: How an AIS Mismatch Triggered an Income Tax Notice

Case Study: Ravi, IT Professional, Pune • Salary: ₹14 lakh per annum • SIP investments in 3 equity mutual funds since 2021 (redeemed in FY 2025-26) • Fixed deposit interest: ₹42,000 (bank deducted TDS at 10%) • Ravi filed ITR-1 reporting only salary income and FD interest omitting LTCG of ₹1.18 lakh from mutual fund redemptions What Happened: The mutual fund house had already reported Ravi’s redemption and LTCG to the Income Tax Department via AIS. The ITR-1 Ravi filed (which cannot accommodate capital gains) was also the wrong form. Result: Defective return notice under Section 139(9) + intimation under Section 143(1)(a) for unreported capital gains. He had to refile using ITR-2, pay additional tax, and clear the notice — all of which could have been avoided with a 10-minute AIS review.

Most Common AIS Mismatches That Trigger Income Tax Notices in AY 2026-27

Mutual fund redemptions reported in AIS but not declared in ITR especially SIP redemptions or systematic withdrawal plans

FD and savings account interest income under-reported or omitted entirely

Dividend income from shares or mutual funds not included (dividends are now taxable in the hands of the investor)

Property sale consideration shown in AIS at the registered value, while taxpayer reports lower consideration in ITR

Cryptocurrency or VDA transactions reported by exchanges but omitted from ITR

GST turnover in AIS not matching income declared in ITR (common for freelancers and small business owners)

Foreign remittances or LRS transactions in AIS not reflected in ITR

Employer reporting perquisites or ESOPs in AIS that the taxpayer was unaware of

Who Must Absolutely Review AIS Before Filing ITR for AY 2026-27?

While every taxpayer benefits from an AIS review, certain profiles face the highest risk from AIS mismatches:

Salaried professionals who invest in mutual funds, stocks, or have fixed deposits

Freelancers and consultants who receive professional fees and may have GST registration

Business owners whose GST turnover is captured in AIS and must match income tax declarations

Doctors, architects, lawyers, and other self-employed professionals with TDS on professional fees

NRIs with Indian income sources rental income, interest, dividends, or capital gains

Stock market investors and traders particularly those with F&O trading activity

Real estate investors who sold property during FY 2025-26

Crypto investors whose exchange transactions are now reported to the Income Tax Department

Critical ITR Filing Deadlines and AIS Review Timeline for AY 2026-27

Managing your AIS review within the right timeline is essential for penalty-free ITR filing:

Deadline / Action

Details

ITR Filing Due Date (Non-Audit)

July 31, 2026 — File before this date to avoid late filing fee under Section 234F

Audit Cases ITR Due Date

October 31, 2026

Belated Return Deadline

December 31, 2026 (with late fee of ₹1,000–₹5,000)

Ideal AIS Review Window

June 1 to July 15, 2026 — reconcile and file well before the deadline

AIS Feedback Submission

Submit corrections on the AIS portal before filing ITR to avoid mismatch notices

Frequently Asked Questions

Q1. What is the AIS password to open the downloaded PDF?

The AIS PDF password is your PAN number in lowercase letters followed by your date of birth in DDMMYYYY format with no spaces or special characters. For example, if your PAN is ABCPQ9876R and your date of birth is 22nd January 1988, the password is abcpq9876r22011988.

Q2. Can an AIS mismatch trigger an income tax notice?

Yes absolutely. The Income Tax Department’s automated systems compare your filed ITR data against your AIS and TIS figures. Even minor discrepancies in interest income, capital gains, dividend income, or GST turnover can result in an automated intimation under Section 143(1)(a) or a scrutiny notice under Section 143(2). This is why AIS reconciliation before ITR filing is non-negotiable.

Q4. What should I do if I find incorrect information in my AIS?

You can submit feedback directly on the AIS portal against any entry. Options include marking it as ‘Information is correct’, ‘Information is not fully correct’, ‘Information relates to other person / year’, ‘Information is duplicate / included in other information’, or ‘Information is denied’. This feedback updates your TIS, which is then used as a reference for ITR pre-fill and automated processing.

Q6. Is there a late filing penalty even if my tax payable is nil after TDS?

Yes. Under Section 234F of the Income Tax Act, a late filing fee of ₹1,000 applies if your total income exceeds ₹2.5 lakh but does not exceed ₹5 lakh, and ₹5,000 if your income exceeds ₹5 lakh regardless of whether your tax liability after TDS credit is nil. Filing before July 31, 2026 avoids this penalty entirely.

Q7. Can I download AIS for previous financial years?

Yes. The AIS portal at compliance.insight.gov.in allows taxpayers to access AIS data for multiple financial years. You can select FY 2024-25, FY 2023-24, or earlier years from the financial year dropdown. This is particularly useful when responding to income tax notices for past years or filing belated/revised returns.

Conclusion:

The Annual Information Statement is the Income Tax Department’s most powerful transparency tool and it should be your most important pre-filing checklist. Before you file a single digit in your ITR for AY 2026-27, download your AIS, open it with the correct password, reconcile every entry against your own records, and submit feedback for any incorrect data.

AsDr. Haresh Adwani of Adwani and Company emphasises: “Taxpayers who review their AIS carefully before filing rarely face income tax notices. Those who skip it often spend weeks dealing with the consequences. The ten minutes spent on AIS review today saves ten hours of notice management tomorrow.”

About the Author Dr. Haresh Adwani Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra. He has guided hundreds of SMEs, startups, and corporates through India’s evolving tax landscape. He is a recognised advisor on GST compliance, company formation, and Virtual CFO services, and regularly contributes to professional seminars and industry forums in Pune.

The Simple ITR Form That Is Not So Simple for Millions of Taxpayers

Every year, millions of Indians instinctively reach for ITR 1 also known as the Sahaj form because it feels familiar, it looks simple, and it has always been “the salaried person’s form.” And for a large segment of taxpayers, it absolutely is the right choice.

But here is the problem: a significant and growing number of salaried employees, professionals, and investors are filing ITR 1 when they are not eligible to do so. The result is a defective return notice under Section 139(9), a delayed refund, and in some cases, a demand for revised filing with penalties.

The Income Tax Department has made ITR form selection a critical compliance checkpoint. With the introduction of the Annual Information Statement (AIS) and real-time data reporting from banks, brokers, mutual funds, and registrars, the department’s processing systems automatically flag returns where the wrong form has been used. The verification is instant, the notice is automated, and the consequences are real.

At ITR Advisor, we help taxpayers across India understand which ITR form is correct for their specific income profile and we file their returns with the precision and expertise that modern tax compliance demands. This guide answers, once and for all, the question that thousands of taxpayers search for every season: who cannot file ITR-1 for AY 2026-27?

What Is ITR 1 (Sahaj) and Who Is It Actually Designed For?

ITR-1, officially called the Sahaj form, was designed for the simplest income profiles a single employer, straightforward salary, basic deductions, one house property, and limited financial activity. As per the guidelines published on the official Income Tax e-Filing Portal, ITR 1 is applicable only for resident individuals whose income profile satisfies all of the following conditions simultaneously:

Total income does not exceed ₹50 lakh during the financial year

Income comes only from salary or pension

Income from one house property (where there is no brought-forward loss)

Income from other sources such as savings interest and FD interest (excluding lottery, horse racing, or speculative income)

Agricultural income up to ₹5,000

If your income profile matches all five conditions cleanly ITR1 is your form. If even one condition is not met, you must move to a different form, most commonly ITR 2 or ITR 3.

The challenge is that most taxpayers do not realise how many common financial activities knock them out of ITR 1 eligibility. Let us go through each restriction in detail.

Complete List: Who Cannot File ITR-1 for AY 2026-27

1. Taxpayers Whose Total Income Exceeds ₹50 Lakh

This is the most straightforward restriction. If your gross total income from salary, interest, rental, capital gains, or any other source exceeds ₹50 lakh in FY 2025-26, you cannot use ITR 1.

Taxpayers crossing this threshold must use ITR 2 (if no business income) or ITR 3 (if business or professional income is also present).

It is important to note that “total income” for this purpose includes all income before deductions under Chapter VI A. So even if your net taxable income after 80C and 80D deductions is below ₹50 lakh, if your gross income exceeds the limit, ITR 1 is not applicable.

2. Taxpayers with Capital Gains from Any Source

This is the single most common reason salaried employees are disqualified from ITR 1 and the one they are least aware of.

If you have earned capital gains during the year from any of the following sources, you cannot file ITR 1:

Sale of equity shares (listed or unlisted)

Redemption or switching of mutual fund units (including SIPs)

Sale of ELSS fund units after the lock-in period

Sale of debt mutual funds

Encashment of bonds or debentures

Sale of residential property or commercial property

Sale of gold, gold ETFs, or sovereign gold bonds

Sale of any other capital asset

Important: Even if your LTCG from equity falls below the ₹1.25 lakh exemption threshold and no tax is payable, the transaction still disqualifies you from ITR 1. The exemption applies to tax liability not to the disclosure requirement or form eligibility.

The correct form for salaried employees with capital gains is ITR 2, which includes a dedicated Schedule CG for accurate reporting.

Real Example: Meera is a schoolteacher in Nagpur earning ₹9.8 lakh annually. In March 2026, she redeemed her ELSS mutual fund after the three year lock in period and received ₹1.1 lakh in LTCG entirely within the ₹1.25 lakh exemption. She assumed that since no tax was owed, she could still file ITR-1. Her return was marked defective. She had to refile using ITR 2, which delayed her ₹32,000 refund by nearly two months.

3. Individuals with Business Income, Freelance Income, or Professional Receipts

If you earn any income that qualifies as business or professional income under the Income Tax Act, ITR 1 is not applicable. This includes:

Freelance writing, design, photography, or consulting fees

Income from tuition or coaching classes

Commission income (insurance agents, real estate brokers)

Income from practice (doctors, lawyers, architects, CAs with private clients)

Income from any trade, commerce, or manufacturing activity

Income from gig economy platforms (Uber, Swiggy delivery, Upwork, Fiverr)

If you are salaried but also earn even a modest amount from freelance or consulting work say ₹30,000 from a project you cross into ITR-3 territory (or ITR-4 if you opt for presumptive taxation under Section 44ADA).

4. Individuals Holding Foreign Assets or Having Foreign Income

If you hold or have held at any point during FY 2025-26:

A foreign bank account (including NRE, NRO, or FCNR accounts held abroad)

Foreign equity shares or stocks (including RSUs from a foreign employer that have vested)

A foreign property or immovable asset

Beneficial ownership in a foreign trust or entity

Any other foreign asset required to be disclosed under the Black Money Act

…then you cannot file ITR 1. You must use ITR 2, which includes Schedule FA (Foreign Assets) for mandatory disclosure.

Similarly, if you received any income from foreign sources RSU income, overseas salary credits, foreign dividend, or international freelance payments ITR 2 is required.

The Income Tax Department has significantly stepped up enforcement of foreign asset disclosures in recent years. Non-disclosure of foreign assets can attract penalties under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 making accurate form selection critically important for anyone with overseas financial exposure.

5. Company Directors and Unlisted Equity Shareholders

If you serve as a director in any company private, public, or otherwise during the financial year, you are not eligible to use ITR-1, regardless of your salary level or other income.

Similarly, if you hold equity shares in an unlisted company at any point during the year, ITR-2 is mandatory. This is a particularly important restriction for employees of startups who receive ESOPs in unlisted companies, or for professionals who hold a nominal stake in a family-owned private limited company.

6. Taxpayers with More Than One House Property

ITR-1 allows income from only one house property. If you own more than one property whether both are self-occupied, one is let out, or one is deemed let-out you must file ITR-2.

This restriction catches many taxpayers by surprise. Common scenarios where this applies:

Inherited property alongside your own purchased flat

Joint ownership in parents’ house along with your own home

Two self-occupied properties (only one can be treated as self-occupied for tax purposes under current rules; the other is treated as deemed let-out)

7. Individuals with Crypto or Virtual Digital Asset (VDA) Income

Virtual Digital Assets, including cryptocurrency, NFTs, and other digital tokens, are taxable at a flat 30% under Section 115BBH. Since crypto income falls outside the “income from other sources” category permitted in ITR-1, taxpayers with any crypto transactions whether profit or loss must use ITR-2 or ITR-3.

The Income Tax Department receives transaction data from crypto exchanges registered in India. If your AIS shows crypto activity but your ITR 1 does not reflect it, an AIS mismatch notice is virtually certain.

8. NRIs and Non-Resident Taxpayers

ITR-1 is available only for resident individuals as defined under the Income Tax Act. If your residential status for FY 2025-26 is:

Non-Resident (NRI)

Resident but Not Ordinarily Resident (RNOR)

…you cannot use ITR-1. NRIs and RNORs must file using ITR-2, which provides for the correct residential status declaration and applicable income schedules.

If you returned to India during the year and are unsure of your residential status, a day-count calculation based on physical presence in India is required. This is an area where professional guidance from a tax expert is strongly recommended.

Learn more about our NRI Residential Status Determination and ITR Filing Services.

9. Taxpayers with Agricultural Income Exceeding ₹5,000

While agricultural income itself is exempt from tax, if your agricultural income exceeds ₹5,000 during the year, ITR 1 is not eligible. You must use ITR 2, which allows for the proper partial integration calculation applicable when agricultural income exceeds this threshold.

10. Individuals with Brought-Forward Losses from Previous Years

If you have carried forward capital losses from prior assessment years that you wish to set off against current year gains, ITR 1 cannot accommodate this. The Schedule CG in ITR 2 handles brought-forward loss set off and carry forward calculations.

Similarly, if you have house property losses from previous years (exceeding the ₹2 lakh cap) still being carried forward, ITR 2 is required.

Why Filing the Wrong ITR Form Is a Bigger Problem Than Most Taxpayers Realise

Filing ITR 1 when you are actually eligible for ITR 2 or ITR 3 triggers a Section 139(9) defective return notice from the Income Tax Department. This notice:

Declares your return invalid

Gives you a 15-day window (extendable) to file a corrected return in the right form

Holds your tax refund pending correction

In some cases, results in interest implications if the correction is delayed

Beyond the notice itself, an incorrect ITR can result in under-reporting of income (by omitting schedules the correct form would have captured), which carries penalty risk under Section 270A.

The good news is that this is entirely preventable with proper form selection before filing begins.

How to Correctly Identify Your ITR Form for AY 2026-27

Before selecting your form, ask yourself these five questions:

1. Is my gross total income below ₹50 lakh?

2. Have I sold any shares, mutual funds, property, or any capital asset this year?

3. Do I have any freelance, consulting, business, or professional income?

4. Do I hold foreign assets or have I received foreign income?

5. Am I a director in any company or do I hold unlisted shares?

If the answer to question 1 is YES and all others are NO ITR 1 is likely your correct form (subject to verifying the other conditions above).

If the answer to any of questions 2 through 5 is YES you need ITR-2 at minimum, possibly ITR-3.

When in doubt, reviewing your AIS on the Income Tax portal before making the decision is the most reliable approach. Your AIS will show every transaction reported against your PAN making it clear whether any of the disqualifying activities occurred during the year.

At ITR Advisor, Dr. Haresh Adwani a PhD holder in Commerce and a law graduate with deep expertise in income tax law leads a team of professionals who review each client’s complete income profile before selecting the appropriate ITR form. This expert first approach prevents defective return notices and ensures your filing is accurate from the start.

Q1. Which ITR form should salaried employees use for AY 2026-27?

Salaried employees with income below ₹50 lakh, no capital gains, no foreign assets, one house property, and no business income can use ITR 1. Employees with capital gains (even exempt LTCG), two properties, foreign assets, directorship, or unlisted shares must use ITR 2. Employees with additional business or professional income should file ITR 3.

Q2. Can AIS mismatch trigger an income tax notice even if I file ITR-1 correctly?

Yes. Even if you are technically eligible for ITR1, failing to report income visible in your AIS such as FD interest from multiple banks, dividend income, or savings account interest will create a mismatch between your ITR and AIS. The department’s automated processing system flags these mismatches and generates notices. Always review your AIS before filing.

Q3. I am a salaried employee but also a director in my spouse’s company with no active role. Do I need ITR-2?

Yes. Directorship in any company regardless of whether you are active, paid, or have any shareholding disqualifies you from ITR-1. You must file ITR 2 for AY 2026-27.

04.What happens if I file ITR-1 when I should have filed ITR-2?

The Income Tax Department’s processing system identifies the form mismatch and issues a Section 139(9) defective return notice. You will be required to refile using the correct form within the specified timeframe. This delays your refund and, if the correction deadline is missed, the original return may be treated as invalid.

05.Can ITR Advisor help me determine the right ITR form for my profile?

Absolutely. ITR Advisor’s tax experts review your complete income profile — salary, investments, AIS data, foreign exposure, directorship, and all other relevant factors — to identify the correct ITR form and ensure accurate, complete filing. Dr. Haresh Adwani and the ITR Advisor team bring professional-grade tax expertise to every return.

Conclusion:

ITR form selection is not a formality it is the foundation of a correct and compliant income tax return. Filing ITR 1 when you are not eligible is one of the most common and most avoidable reasons salaried taxpayers receive defective return notices, face refund delays, and invite unnecessary scrutiny.

The restrictions around who cannot file ITR-1 for AY 2026-27 are clear and well-defined: income above ₹50 lakh, capital gains of any kind, business or freelance income, foreign assets, directorship, unlisted shares, more than one property, crypto transactions, NRI status, and carried-forward losses any one of these requires a different form.

The smart approach is to check your AIS, review your full income profile, and confirm your form eligibility before filing. When the decision involves complexity multiple income sources, foreign exposure, capital gains, or ESOPs professional guidance is not just helpful, it is essential.

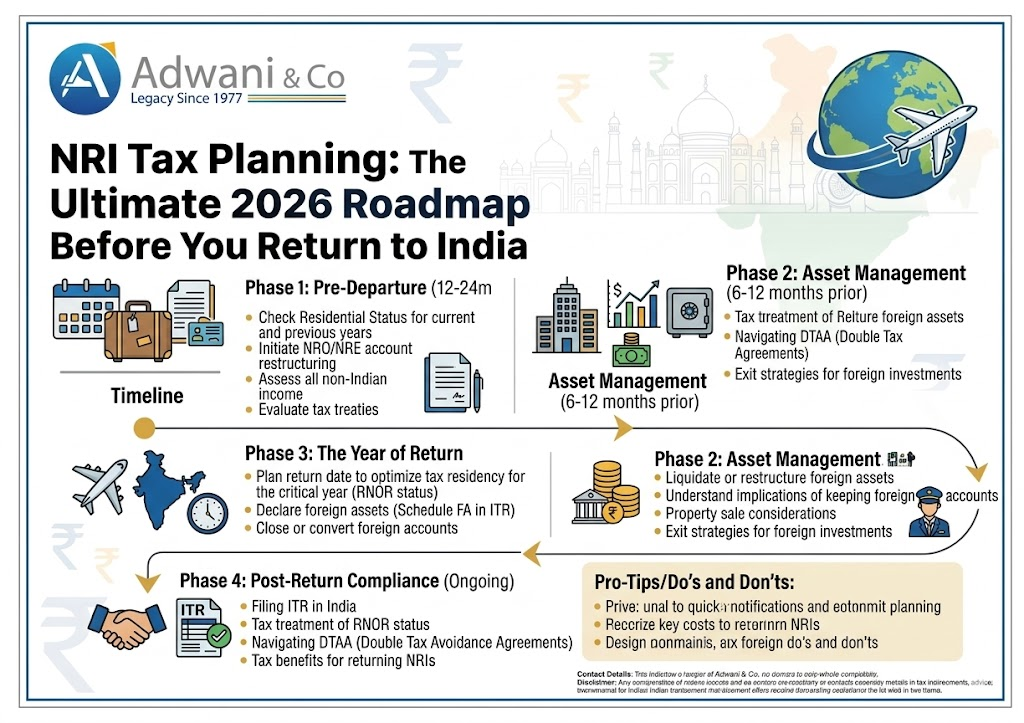

NRI Tax Rules India 2026: The Essential Roadmap Every Returning NRI Must Follow

The flight is booked. The resignation letter is written. After ten, fifteen, sometimes twenty years abroad, you are finally coming home. But somewhere between the excitement of reunion dinners and the relief of leaving behind bitter winters, one question sits quietly at the back of your mind what happens to my money?

It is the question most returning NRIs either ask too late or never ask at all until the Income Tax Department sends them a notice that arrives long after they have settled back in. The uncomfortable truth is this: the moment your residential status shifts from NRI to Resident Indian, India’s tax net expands dramatically. Your US brokerage account, your UK pension, your Dubai rental income, your Singapore investments all of it can suddenly fall within India’s taxing jurisdiction.

This is not a scare tactic. It is the straightforward application of NRI tax rules in India, as laid out by the Income Tax Department at incometax.gov.in. And the good news is that with proper planning ideally six to twelve months before you board that return flight you can navigate this transition intelligently, legally, and with far less tax outgo than you might fear.

This comprehensive guide, prepared with insights from Adwani and Company and its lead expert Dr. Haresh Adwani, covers every critical dimension of NRI tax planning for 2026: residential status transitions, RNOR benefits, NRI capital gains tax implications, FEMA compliance, DTAA relief, and ITR filing obligations. Consider this your complete pre-departure tax checklist.

Understanding NRI Tax Rules in India : It All Starts With Residential Status

Before any investment strategy, account restructuring, or tax planning can begin, one thing must be determined with precision: your exact residential status under Indian tax law for each financial year during and after your return.

The Income Tax Act, 1961 classifies individuals into three categories and each carries dramatically different NRI tax rules:

The Three Residential Status Categories

NRI : Non-Resident Indian An individual qualifies as an NRI if they stay in India for fewer than 182 days in a financial year (general rule). As an NRI, India taxes you only on income earned or received within India your foreign income is completely outside India’s reach.

RNOR : Resident but Not Ordinarily Resident This is the transitional status that returning NRIs enter before becoming full residents. It is the single most valuable planning window in NRI tax rules. During RNOR status, you are technically a resident, but foreign income that is not derived from a business controlled in India or a profession set up in India remains outside India’s tax net. This status typically lasts two to three financial years after returning, depending on how many years you spent as an NRI.

ROR : Resident and Ordinarily Resident This is full residency. Every rupee of global income salary, interest, dividends, capital gains, rental income is taxable in India, regardless of where it is earned or held. Once you become ROR, the NRI tax rules that protected your foreign income no longer apply.

The transition looks like this: NRI → RNOR (planning window) → ROR (full global taxation).

The RNOR window is your golden opportunity. Squander it, and you pay taxes you did not need to pay. Use it wisely, and you can restructure investments, liquidate foreign assets, and repatriate funds in a way that is both legal and dramatically more tax-efficient.

“Most NRIs think they have all the time in the world after they land. The reality is the clock starts the moment the financial year begins. We always recommend calculating the RNOR window at least a year in advance , it is the foundation of the entire planning exercise.”

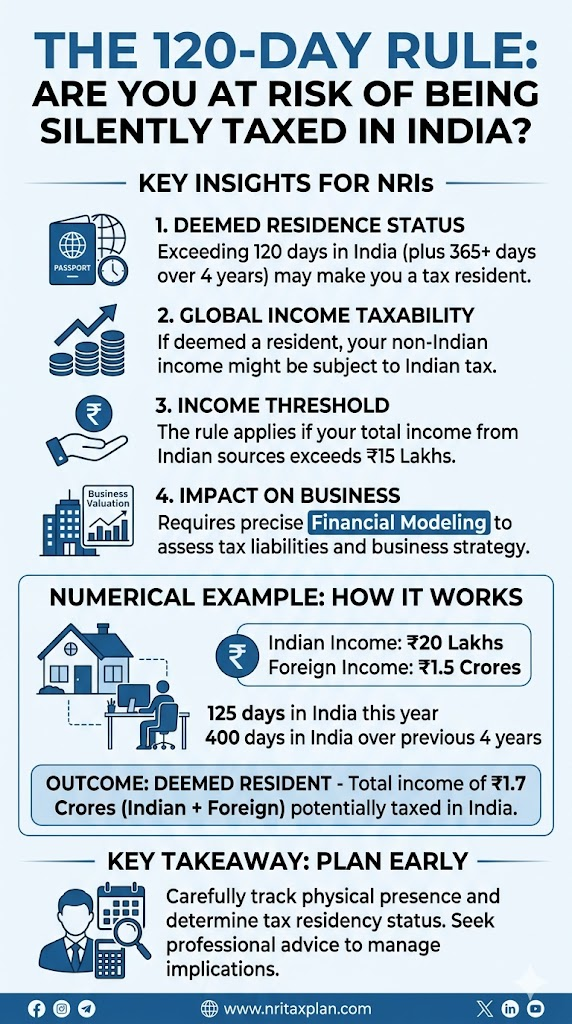

The 120-Day Trap — NRI Tax Rules That Catch People Off Guard

Here is a provision in India’s NRI income tax rules that most people including many financial advisors still underestimate. Introduced via the Finance Act 2020, it can reclassify an NRI as a tax resident even when they continue to physically live abroad.

When Does the 120-Day Rule Apply?

Three conditions must all be satisfied simultaneously:

Your Indian income exceeds ₹15 lakh in the financial year (this includes salary from Indian employers, rent from Indian property, dividends from Indian stocks, or interest from NRO accounts)

You stayed in India for 120 days or more in that financial year

Your cumulative India stays over the preceding four financial years total 365 days or more

If all three conditions apply, you are classified as a resident for that financial year and your global income becomes taxable in India.

The dangerous part is how easily 120 days accumulates without deliberate tracking. A summer visit for a family wedding (30 days), a Diwali trip (3 weeks), a medical emergency in March (2 weeks), and a business trip to Mumbai (10 days) that alone is 87 days. Add a few more trips and you have crossed the threshold without ever intending to.

The solution is simple but requires discipline: maintain a precise record of every India entry and exit date, verified against your passport stamps. If your Indian income from any source NRI capital gains tax on property, NRO interest, rental income exceeds ₹15 lakh, this is not optional. It is essential risk management.

NRI Capital Gains Tax in India 2026 — What Changes When You Return

One of the most financially significant areas within NRI tax rules concerns capital gains on investments both Indian and foreign. The rules shift substantially depending on your residential status at the time of the transaction.

Capital Gains on Indian Assets (Shares, Mutual Funds, Property)

For investments held in India listed shares, equity mutual funds, real estate NRI capital gains tax rules are broadly similar to those for resident Indians under the Income Tax Act, as updated for AY 2026-27

Asset Type

Holding Period

Tax Rate (NRI & Resident)

Listed equity shares / equity MFs

> 1 year (LTCG)

12.5% on gains above ₹1.25 lakh

Listed equity shares / equity MFs

≤ 1 year (STCG)

20% flat

Debt mutual funds

Any period

Taxable at slab rates

Real estate (property)

> 2 years (LTCG)

12.5% (indexation removed for post-July 2024 sales)

Real estate (property)

≤ 2 years (STCG)

Taxable at slab rates

As an NRI selling Indian property, TDS at 12.5% (LTCG) or 30% (STCG) is deducted at source by the buyer — even before you see the proceeds. Obtaining a lower TDS certificate from the Income Tax Department (Form 13) beforehand can reduce this deduction to the actual tax liability, significantly improving your cash flow.

:Capital Gains on Foreign Assets After Returning

This is where the RNOR window becomes enormously valuable. Consider the difference:

Sold while still NRI: India has no right to tax gains on foreign assets — taxed only in the country where the asset is held (subject to DTAA)

Sold during RNOR period: Foreign sourced capital gains are generally not taxable in India during RNOR status — a significant relief

Sold after becoming ROR: Full Indian capital gains tax applies on the global appreciation, with DTAA credit available only if foreign tax was actually paid

For a returning professional with, say, USD 200,000 in a US brokerage account (stocks bought at USD 80,000 cost — a gain of USD 120,000, approximately ₹1 crore), the difference between selling during the RNOR window versus after becoming ROR could easily amount to ₹12–15 lakh in Indian tax.

Real-World Example How Smart NRI Tax Planning Saved ₹18.5 Lakh

Case: Priya R., Senior Engineer Seattle to Hyderabad, Return Year FY 2025-26

Priya spent 12 years in the United States and decided to return to India permanently in November 2025. Her financial profile at the time of return:

Indian apartment generating ₹14.4 lakh annual rental income

NRE fixed deposits: ₹32 lakh

Without Planning : Estimated Tax Exposure

After becoming ROR (which would have happened in FY 2027-28 without planning), if Priya sold her US portfolio, the entire ₹97 lakh gain would be taxable in India as long-term capital gains at 12.5% — a tax liability of approximately ₹12.1 lakh, with no foreign tax offset since the US levies 0% LTCG on this income bracket for her filing status.

Additionally, her NRE accounts, not re-designated in time, would constitute a FEMA violation penalties of up to 3x the value of the violation apply under FEMA, 1999.

With Planning via Adwani and Company: