Dr. Haresh Adwani April 2026 8 min read

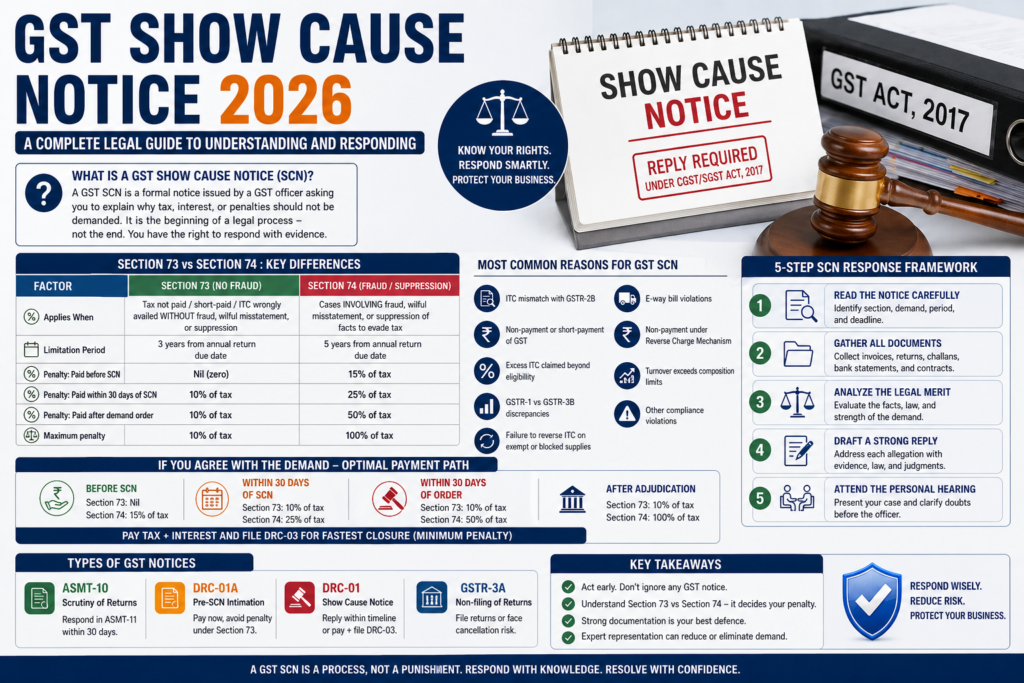

What Is a GST Show Cause Notice (SCN)?

A GST Show Cause Notice (SCN) is a formal legal communication issued by a GST officer under the CGST/SGST Act 2017. It requires the recipient to explain “show cause” why a specified action (typically a tax demand, interest levy, or penalty confirmation) should not proceed.

A GST Show Cause Notice is the beginning of a legal process, not its conclusion. You have every right to present your case with evidence. The danger is not the notice itself it is an uninformed, delayed, or undocumented response.

The Two Critical GST SCN Provisions: Section 73 vs Section 74

Every GST Show Cause Notice is issued under one of two provisions and this distinction is the most important piece of information in the notice. It determines your penalty exposure, response urgency, and the cost of resolution at every stage.

| Factor | Section 73 (No Fraud) | Section 74 (Fraud / Suppression) |

| Applies when | Tax not paid / short-paid / ITC wrongly availed WITHOUT fraud, wilful misstatement, or suppression | Cases INVOLVING fraud, wilful misstatement, or suppression of facts to evade tax |

| Penalty: Paid before SCN | Nil (zero) | 15% of tax |

| Penalty: Paid within 30 days of SCN | 10% of tax | 25% of tax |

| Penalty: Paid after demand order | 10% of tax | 50% of tax |

| Maximum penalty (contested and confirmed) | 10% of tax | 100% of tax |

| Limitation period for SCN | 3 years from annual return due date | 5 years from annual return due date |

Most Common Reasons for a GST Show Cause Notice in 2026

- ITC mismatch: ITC claimed in GSTR-3B does not reconcile with auto-populated GSTR 2B data.

- Non-payment or short payment of GST on taxable supplies.

- Excess ITC claimed beyond Section 16 eligibility conditions.

- Discrepancy between GSTR 1 outward supply data and GSTR-3B tax payment.

- Failure to reverse ITC on exempt supplies or blocked credits under Section 17(5).

- E-way bill violations goods transported without valid documentation.

- Non-payment of GST under Reverse Charge Mechanism on applicable services.

- Turnover exceeding composition scheme limits without transitioning to regular registration.

Types of GST Show Cause Notice Notices: A Complete Reference

ASMT-10: Scrutiny of Filed Returns

Issued under Section 61 when a GST officer identifies discrepancies in your filed returns (typically between GSTR-1, GSTR-3B, and GSTR-2B). Respond in Form ASMT-11 within 30 days with a documented reconciliation. A well-drafted ASMT-11 response prevents escalation to a formal SCN in most cases.

DRC-01A: Pre-SCN Intimation Your Zero-Penalty Opportunity

DRC-01A is a pre-notice intimation that gives you the opportunity to voluntarily accept the demand and pay the tax with interest before formal proceedings begin. Proactive payment at DRC-01A stage under Section 73 results in zero penalty. This is the most cost-effective resolution point for any GST dispute. Treat DRC-01A with the same urgency as a formal SCN.

DRC-01: The Formal Show Cause Notice

DRC-01 is the primary show cause notice under Section 73 or 74. Upon receipt, you must either pay the demand with interest and file DRC-03 (voluntary payment challan), or file a detailed written reply within the prescribed deadline typically 30 days. This is the most consequential notice to respond to correctly.

GSTR-3A: Notice for Non-Filing of Returns

Issued under Section 46 when returns have not been filed for two or more consecutive tax periods. Continued non-filing after GSTR-3A can result in GSTIN cancellation, creating severe business continuity risks.

Also Read:

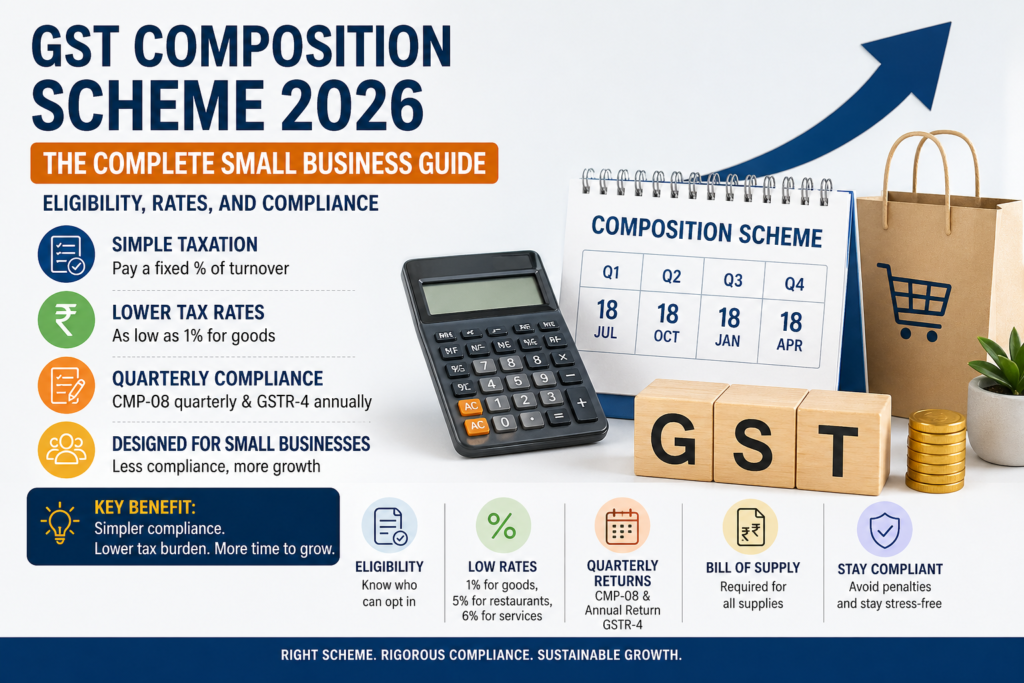

https://itradvisor.in/blog/gst-composition-scheme

The 5-Step GST Show Cause Notice Response Framework

Step 1: Read the Notice Carefully and Identify the Section

Identify: (1) Section 73 or 74, (2) the exact demand tax, interest, and proposed penalty, (3) the specific transactions or return periods in question, and (4) your response deadline. Section 73 vs 74 is the single most important data point.

Step 2: Gather Every Relevant Document

Assemble: tax invoices, e-way bills, filed GSTR-1 and GSTR-3B returns, purchase invoices, GSTR-2B statements, DRC-03 challans, bank statements, and supplier contracts. Strong, organised documentation is your most powerful defence.

Step 3: Analyse the Legal Merit of the Demand

Not every GST SCN represents genuine tax liability. Many notices are generated by automated system mismatches ITC gaps that have valid explanations such as late supplier filings. Expert analysis can identify grounds to contest the demand entirely or substantially reduce admitted liability. Do not assume the department’s position is correct without review.

Step 4: Draft and File a Legally Complete Written Response

Your reply must address each allegation individually with supporting evidence, cite the relevant legal provisions and CBIC circulars, reference favourable High Court and Tribunal judgments, and where genuine liability is admitted quantify it separately from contested amounts.

Step 5: Attend the Personal Hearing

You have a statutory right to a personal hearing before the adjudicating authority. Always request it. The hearing is frequently the turning point in a GST SCN case additional context, documentation, and direct clarification often resolve the matter before any demand order is passed.

If You Agree with the GST Demand: The Optimal Payment Path

| Payment Timing | Section 73 Penalty | Section 74 Penalty |

| Before SCN is issued | NIL (zero) | 15% of tax |

| Within 30 days of SCN | 10% of tax | 25% of tax |

| Within 30 days of demand order | 10% of tax | 50% of tax |

| After adjudication (contested and confirmed) | 10% of tax | 100% of tax |

To pay and close proceedings: File DRC-03 on the GST portal recording the voluntary payment of tax and interest. This is the standard mechanism to close Section 73 proceedings with minimum (or zero) penalty.

GST Show Cause Notice Timelines and Limitation Periods (2026)

- Section 73 SCN limitation: Must be issued within 3 years from the due date of the annual return for the relevant year (5 years if no return was filed).

- Section 74 SCN limitation: Must be issued within 5 years from the due date of the annual return.

- ASMT-10 response deadline: 30 days from notice date (extendable on application to the adjudicating officer).

- DRC-01 response deadline: As specified in the notice typically 30 days.

Conclusion: A GST Show Cause Notice Is a Process Respond Wisely

A GST Show Cause Notice is the opening of a legal conversation, not a final verdict. With the right approach timely response, strong documentation, correct legal citations, and expert representation most GST SCNs are resolved in the taxpayer’s favour or with substantially reduced liability.

Adwani & Company’s dedicated GST litigation team manages every stage of a GST dispute: SCN analysis, Section 73/74 determination, ITC reconciliation, response drafting, personal hearing representation, and appeals. Contact Dr. Haresh Adwani at www.itradvisor.in typically within 24 hours.

Frequently Asked Questions

Q1. How long do I have to respond to a GST SCN?

The notice specifies the deadline typically 30 days from the date of issue. You can apply to the adjudicating officer for an extension before the deadline expires. Never wait until the last day; response preparation requires time.

Q2. Can a GST SCN be challenged directly in court?

Courts generally require exhaustion of statutory remedies first. However, if the SCN is issued beyond the limitation period, lacks proper jurisdiction, or has procedural defects, a writ petition in the High Court may be maintainable. Adwani & Company has successfully pursued such writs where appropriate.

Q3. What happens if I ignore a GST SCN?

The GST officer issues an ex-parte demand order confirming the full tax, interest, and penalty on a best-judgment basis. Your GSTIN may also be suspended. Ignoring a GST SCN eliminates all legal defence and is always the worst possible course of action.

Q4. What is the difference between a GST SCN and a Demand Order?

A GST SCN is your opportunity to respond before any decision is made. A Demand Order (Form DRC-07) is the adjudicating officer’s final decision confirming the liability. A Demand Order can be appealed before the Appellate Authority within three months.

| About the Author Dr. Haresh Adwani Ph.D. in Commerce | 20+ years in Tax, FEMA & Financial Advisory Expert in: GST advisory · Income tax litigation · FEMA compliance · NRI taxation · F&O taxation · Corporate structuring Website: www.itradvisor.in |