Dr. Haresh Adwani May 2026 12 min read

NRI Tax Rules India 2026: The Essential Roadmap Every Returning NRI Must Follow

The flight is booked. The resignation letter is written. After ten, fifteen, sometimes twenty years abroad, you are finally coming home. But somewhere between the excitement of reunion dinners and the relief of leaving behind bitter winters, one question sits quietly at the back of your mind what happens to my money?

It is the question most returning NRIs either ask too late or never ask at all until the Income Tax Department sends them a notice that arrives long after they have settled back in. The uncomfortable truth is this: the moment your residential status shifts from NRI to Resident Indian, India’s tax net expands dramatically. Your US brokerage account, your UK pension, your Dubai rental income, your Singapore investments all of it can suddenly fall within India’s taxing jurisdiction.

This is not a scare tactic. It is the straightforward application of NRI tax rules in India, as laid out by the Income Tax Department at incometax.gov.in. And the good news is that with proper planning ideally six to twelve months before you board that return flight you can navigate this transition intelligently, legally, and with far less tax outgo than you might fear.

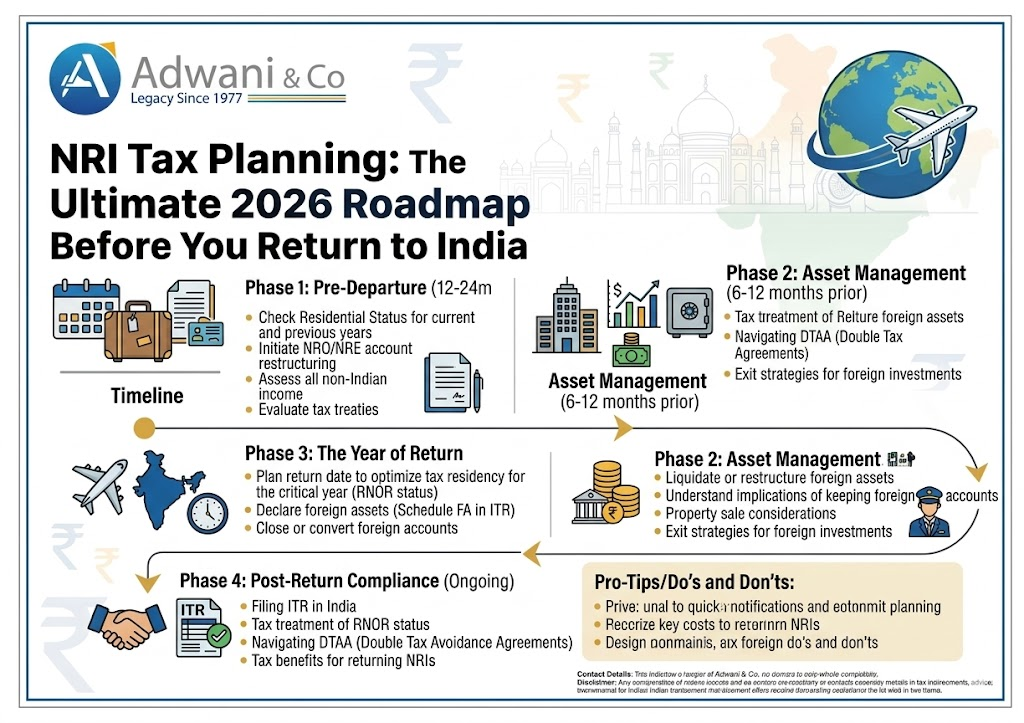

This comprehensive guide, prepared with insights from Adwani and Company and its lead expert Dr. Haresh Adwani , covers every critical dimension of NRI tax planning for 2026: residential status transitions, RNOR benefits, NRI capital gains tax implications, FEMA compliance, DTAA relief, and ITR filing obligations. Consider this your complete pre-departure tax checklist.

Understanding NRI Tax Rules in India : It All Starts With Residential Status

Before any investment strategy, account restructuring, or tax planning can begin, one thing must be determined with precision: your exact residential status under Indian tax law for each financial year during and after your return.

The Income Tax Act, 1961 classifies individuals into three categories and each carries dramatically different NRI tax rules:

The Three Residential Status Categories

NRI : Non-Resident Indian An individual qualifies as an NRI if they stay in India for fewer than 182 days in a financial year (general rule). As an NRI, India taxes you only on income earned or received within India your foreign income is completely outside India’s reach.

RNOR : Resident but Not Ordinarily Resident This is the transitional status that returning NRIs enter before becoming full residents. It is the single most valuable planning window in NRI tax rules. During RNOR status, you are technically a resident, but foreign income that is not derived from a business controlled in India or a profession set up in India remains outside India’s tax net. This status typically lasts two to three financial years after returning, depending on how many years you spent as an NRI.

ROR : Resident and Ordinarily Resident This is full residency. Every rupee of global income salary, interest, dividends, capital gains, rental income is taxable in India, regardless of where it is earned or held. Once you become ROR, the NRI tax rules that protected your foreign income no longer apply.

The transition looks like this: NRI → RNOR (planning window) → ROR (full global taxation).

The RNOR window is your golden opportunity. Squander it, and you pay taxes you did not need to pay. Use it wisely, and you can restructure investments, liquidate foreign assets, and repatriate funds in a way that is both legal and dramatically more tax-efficient.

“Most NRIs think they have all the time in the world after they land. The reality is the clock starts the moment the financial year begins. We always recommend calculating the RNOR window at least a year in advance , it is the foundation of the entire planning exercise.”

The 120-Day Trap — NRI Tax Rules That Catch People Off Guard

Here is a provision in India’s NRI income tax rules that most people including many financial advisors still underestimate. Introduced via the Finance Act 2020, it can reclassify an NRI as a tax resident even when they continue to physically live abroad.

When Does the 120-Day Rule Apply?

Three conditions must all be satisfied simultaneously:

- Your Indian income exceeds ₹15 lakh in the financial year (this includes salary from Indian employers, rent from Indian property, dividends from Indian stocks, or interest from NRO accounts)

- You stayed in India for 120 days or more in that financial year

- Your cumulative India stays over the preceding four financial years total 365 days or more

If all three conditions apply, you are classified as a resident for that financial year and your global income becomes taxable in India.

The dangerous part is how easily 120 days accumulates without deliberate tracking. A summer visit for a family wedding (30 days), a Diwali trip (3 weeks), a medical emergency in March (2 weeks), and a business trip to Mumbai (10 days) that alone is 87 days. Add a few more trips and you have crossed the threshold without ever intending to.

The solution is simple but requires discipline: maintain a precise record of every India entry and exit date, verified against your passport stamps. If your Indian income from any source NRI capital gains tax on property, NRO interest, rental income exceeds ₹15 lakh, this is not optional. It is essential risk management.

Also Read :The 120-Day Rule That Is Silently Taxing Thousands of NRIs in India :Are You at Risk?

NRI Capital Gains Tax in India 2026 — What Changes When You Return

One of the most financially significant areas within NRI tax rules concerns capital gains on investments both Indian and foreign. The rules shift substantially depending on your residential status at the time of the transaction.

Capital Gains on Indian Assets (Shares, Mutual Funds, Property)

For investments held in India listed shares, equity mutual funds, real estate NRI capital gains tax rules are broadly similar to those for resident Indians under the Income Tax Act, as updated for AY 2026-27

| Asset Type | Holding Period | Tax Rate (NRI & Resident) |

| Listed equity shares / equity MFs | > 1 year (LTCG) | 12.5% on gains above ₹1.25 lakh |

| Listed equity shares / equity MFs | ≤ 1 year (STCG) | 20% flat |

| Debt mutual funds | Any period | Taxable at slab rates |

| Real estate (property) | > 2 years (LTCG) | 12.5% (indexation removed for post-July 2024 sales) |

| Real estate (property) | ≤ 2 years (STCG) | Taxable at slab rates |

As an NRI selling Indian property, TDS at 12.5% (LTCG) or 30% (STCG) is deducted at source by the buyer — even before you see the proceeds. Obtaining a lower TDS certificate from the Income Tax Department (Form 13) beforehand can reduce this deduction to the actual tax liability, significantly improving your cash flow.

:Capital Gains on Foreign Assets After Returning

This is where the RNOR window becomes enormously valuable. Consider the difference:

- Sold while still NRI: India has no right to tax gains on foreign assets — taxed only in the country where the asset is held (subject to DTAA)

- Sold during RNOR period: Foreign sourced capital gains are generally not taxable in India during RNOR status — a significant relief

- Sold after becoming ROR: Full Indian capital gains tax applies on the global appreciation, with DTAA credit available only if foreign tax was actually paid

For a returning professional with, say, USD 200,000 in a US brokerage account (stocks bought at USD 80,000 cost — a gain of USD 120,000, approximately ₹1 crore), the difference between selling during the RNOR window versus after becoming ROR could easily amount to ₹12–15 lakh in Indian tax.

Real-World Example How Smart NRI Tax Planning Saved ₹18.5 Lakh

Case: Priya R., Senior Engineer Seattle to Hyderabad, Return Year FY 2025-26

Priya spent 12 years in the United States and decided to return to India permanently in November 2025. Her financial profile at the time of return:

- US stock portfolio: USD 180,000 (purchase cost: USD 65,000 — unrealized gain: USD 115,000 ≈ ₹97 lakh)

- 401(k) balance: USD 90,000

- Indian apartment generating ₹14.4 lakh annual rental income

- NRE fixed deposits: ₹32 lakh

Without Planning : Estimated Tax Exposure

After becoming ROR (which would have happened in FY 2027-28 without planning), if Priya sold her US portfolio, the entire ₹97 lakh gain would be taxable in India as long-term capital gains at 12.5% — a tax liability of approximately ₹12.1 lakh, with no foreign tax offset since the US levies 0% LTCG on this income bracket for her filing status.

Additionally, her NRE accounts, not re-designated in time, would constitute a FEMA violation penalties of up to 3x the value of the violation apply under FEMA, 1999.

With Planning via Adwani and Company:

Dr. Haresh Adwani’s team calculated Priya’s RNOR window as covering FY 2025-26 and FY 2026-27 two full financial years during which foreign income would not be taxable in India. By selling the US portfolio during this RNOR window, the ₹97 lakh capital gain attracted zero Indian tax.

Her NRE accounts were timely re-designated to RFC accounts. Rental income was correctly declared in her ITR filing 2026 (ITR-2 for AY 2026-27). Form 67 was filed for foreign tax credits on US dividend income.

Total Tax Saved Through Planning: ₹18.5 lakh (approximately)

This is not exceptional it is the standard outcome when NRI tax rules are applied correctly and proactively.

FEMA Compliance for Returning NRIs :Non-Negotiable Steps

The Foreign Exchange Management Act (FEMA), 1999, governs how Indian residents hold, operate, and transact in foreign currency assets. Returning NRIs must take specific mandatory steps under FEMA and the consequences of non-compliance are enforced by the Enforcement Directorate, not the Income Tax Department, making them distinct and sometimes more severe.

Mandatory Account Re-Designations

As per Reserve Bank of India (RBI) guidelines, the following must be done immediately upon change of residential status:

| Account Type | Required Action | Consequence of Inaction |

| NRE Account (Non-Resident External) | Re-designate to RFC or regular resident savings account | FEMA violation — penalty up to 3x transaction value |

| FCNR Account (Foreign Currency Non-Resident) | Re-designate to RFC account at maturity | FEMA violation |

| NRO Account (Non-Resident Ordinary) | Re-designate to ordinary resident savings account | FEMA violation |

| Foreign bank accounts abroad | Permitted to retain; must declare in ITR Schedule FA | Penalty under Black Money Act for non-disclosure |

The RFC (Resident Foreign Currency) account is specifically designed for returning residents and allows you to hold foreign currency assets legally after returning. Interest earned on RFC accounts is fully taxable in India under the Income Tax Act unlike NRE accounts, which were tax-free.

Foreign Asset Disclosure in ITR : Schedule FA

Once you attain ROR status, the annual Income Tax Return (ITR filing for AY 2026-27 and beyond) must include Schedule FA Foreign Assets. This covers:

- Foreign bank accounts and their year-end balances

- Foreign equity and debt holdings

- Foreign immovable property

- Foreign trusts, beneficial interests, or signing authority

- Accounts held as beneficial owner or beneficiary in foreign entities

Non-disclosure of foreign assets is prosecuted under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015 which prescribes a flat 30% tax plus a 90% penalty on undisclosed amounts. The penalties are not proportional to undisclosed income they are absolute.

DTAA Benefits : How Returning NRIs Avoid Double Taxation

India’s Double Taxation Avoidance Agreements (DTAA) with over 90 countries are among the most powerful tools in any NRI’s tax planning toolkit. These treaties ensure that income earned in one country is not taxed twice once where it is earned and again in India.

However, DTAA benefits are not automatic. To claim relief, you must:

- Obtain a Tax Residency Certificate (TRC) from the foreign country confirming your tax residency there during the relevant period

- File Form 10F on the Indian income tax e-filing portal along with TRC details

- File Form 67 to claim Foreign Tax Credit (FTC) for taxes already paid abroad this must be filed before the ITR due date or credit is forfeited permanently

Key DTAA provisions relevant to returning NRIs in 2026:

- India-USA DTAA: Covers salary, dividends, interest, royalties, and capital gains — with specific conditions for each. 401(k) and IRA distributions have specific treatment under the agreement.

- India-UAE DTAA: Recently renegotiated. The updated provisions affect salary income and investment gains — obtain current treaty text or consult a specialist.

- India-UK DTAA: Pension income provisions are particularly relevant for UK returnees — UK state pension and occupational pension taxability in India is treaty-governed.

- India-Canada, India-Australia, India-Singapore DTAAs: Each has distinct provisions for employment income, dividends, and capital gains.

As Dr. Haresh Adwani notes: “The DTAA is like a legal shield. But it only protects you if you know how to invoke it correctly — the right forms, the right timing, the right documentation. A missed Form 67 deadline means you lose the credit entirely, even if the law gives you the right to it.”

NRI ITR Filing 2026 : Which Form, What to Declare, When to File

NRI ITR filing is one of the most commonly mishandled aspects of NRI tax compliance in India. Many NRIs believe they do not need to file an ITR if TDS has already been deducted. This is incorrect in most situations.

When Is ITR Filing Mandatory for NRIs?

You must file an ITR if:

- Your India-sourced income exceeds the basic exemption limit (₹3 lakh under new regime, ₹2.5 lakh under old regime)

- You want to claim a refund of excess TDS deducted on NRI capital gains tax or rental income

- You want to carry forward capital losses for set-off in future years

- Your Indian income includes capital gains from sale of property or shares

- You have foreign assets to declare after becoming ROR

Which ITR Form for NRIs and Returning Residents?

| Status & Income Type | Correct ITR Form |

| NRI with salary + one property + interest | ITR-2 |

| NRI with capital gains from shares / property | ITR-2 |

| RNOR or ROR with foreign assets to declare | ITR-2 (Schedule FA mandatory) |

| Returning NRI with business income in India | ITR-3 |

ITR filing last date 2026: July 31, 2026 for individuals not requiring audit (ITR-1 and ITR-2). Missing this date triggers a late filing fee under Section 234F (₹5,000 for income above ₹5 lakh) plus interest under Section 234A.

: NRI Tax Planning Pre-Return Checklist :12 Months Before You Land

Use this checklist as your action plan. Work backward from your expected return date.

12 Months Before Return:

- Calculate your exact RNOR window this single calculation shapes every decision that follows

- List every foreign asset: equity portfolio, retirement accounts (401k, IRA, pension), real estate, mutual funds, bank balances

- Map which assets carry significant unrealised gains and create a disposal strategy

6 Months Before Return:

- Evaluate whether to sell high-gain foreign assets before return (while still NRI) or during the RNOR window

- Obtain Tax Residency Certificate from the foreign country for DTAA purposes

- Begin preparing documentation for Form 67 (foreign tax credit)

- Consult your Indian bank about re-designating NRE/FCNR accounts to RFC accounts

Before or Immediately Upon Return:

- Re-designate NRE and FCNR accounts do not delay this even by one day

- File NRI status change intimation with your Indian bank(s)

- Ensure your ITR for the year of return includes both Indian and foreign income correctly bifurcated by RNOR rules

After Return (Ongoing):

- File annual ITR with Schedule FA for all foreign assets once ROR status is attained

- Track India stay days carefully every financial year if Indian income exceeds ₹15 lakh

- Renew Tax Residency Certificates annually as long as DTAA claims are being made

Frequently Asked Questions

1. What is the most important thing an NRI must do before returning to India for tax purposes?

The single most important step is calculating your RNOR window the period after returning during which foreign income remains outside India’s tax net. This window, typically two to three financial years, is the foundation of all NRI tax planning. Calculating it in advance allows you to time investment liquidations, account restructuring, and fund repatriation for maximum tax efficiency. Adwani and Company recommends doing this calculation at least 12 months before the planned return date.

2. Do I have to pay tax in India on money already sitting in my foreign bank account when I return?

The principal amount in your foreign bank account money already earned and saved — is generally not taxed again in India. However, interest earned on that account after you become ROR is taxable as income in India. Additionally, any investment gains on assets funded by that account will be subject to Indian NRI capital gains tax rules once you are ROR. The account itself must be declared in Schedule FA of your ITR once ROR status is attained.

3. Can I keep my foreign brokerage account (US, UK, Singapore) after returning to India?

Yes, you are permitted to retain foreign investment accounts after returning to India, under FEMA’s Overseas Investment (OI) regulations. However, once you attain ROR status, all income (dividends, interest) and gains from these accounts must be declared in your Indian ITR, including Schedule FA. Additionally, any gains on sale of foreign securities are taxable as NRI capital gains tax in India subject to DTAA relief if foreign taxes were paid.

4.Is NRI ITR filing mandatory if TDS has already been deducted on my Indian income?

Yes, NRI ITR filing is mandatory if your total Indian income exceeds the basic exemption limit, even if TDS has been fully deducted. Filing the ITR is the only way to claim a refund if excess TDS was deducted, to carry forward capital losses, and critically to comply with foreign asset disclosure requirements under Schedule FA once you become ROR. Non-filing when mandatory can attract notices, penalties, and assessments from the Income Tax Department.

5. What penalties apply if I fail to disclose foreign assets after becoming a Resident Indian?

Under the Black Money (Undisclosed Foreign Income and Assets) and Imposition of Tax Act, 2015, failure to disclose foreign assets in your ITR attracts a flat 30% tax on the asset’s fair market value plus a 90% penalty effectively 120% of the asset’s value in taxes and penalties. Additionally, prosecution for wilful non-disclosure can result in imprisonment of three to ten years. This is one of the most severe penalty regimes in Indian tax law and leaves absolutely no room for casual non-compliance.

Conclusion

Returning home after years abroad is one of life’s most meaningful transitions. The last thing you want is to discover —six months after landing that you owe the Income Tax Department a sum that proper planning could have legally eliminated.

The NRI tax rules India 2026 framework is neither punitive nor impossible to navigate. The RNOR window is a legitimate, statutory protection. The DTAA regime provides genuine relief from double taxation. FEMA compliance, handled proactively, is straightforward. The 120-day rule, once understood, is entirely manageable with basic travel tracking.

What makes the difference is timing and expertise. Every month of delay between the decision to return and the implementation of a proper tax plan costs you options. Assets that could have been sold tax-free during the RNOR window become taxable. NRE accounts that should have been re-designated continue in violation. Foreign tax credits that could have been claimed are forfeited because Form 67 was not filed on time.

If you want expert, end-to-end GST compliance support for your business in FY 2026-27, connect with Adwani and Company today. Our team handles everything monthly filings, ITC reconciliation, annual returns, and notice management so you can focus entirely on growing your business.

About the Author

Dr. Haresh Adwani

Ph.D. in Commerce | Law Graduate | Managing Partner, Adwani & Co LLP Dr. Haresh Adwani holds a Ph.D. in Commerce and is a qualified Law graduate with over two decades of hands-on experience in GST advisory, direct taxation, and statutory compliance for businesses across Pune and Maharashtra.

Leave a Reply