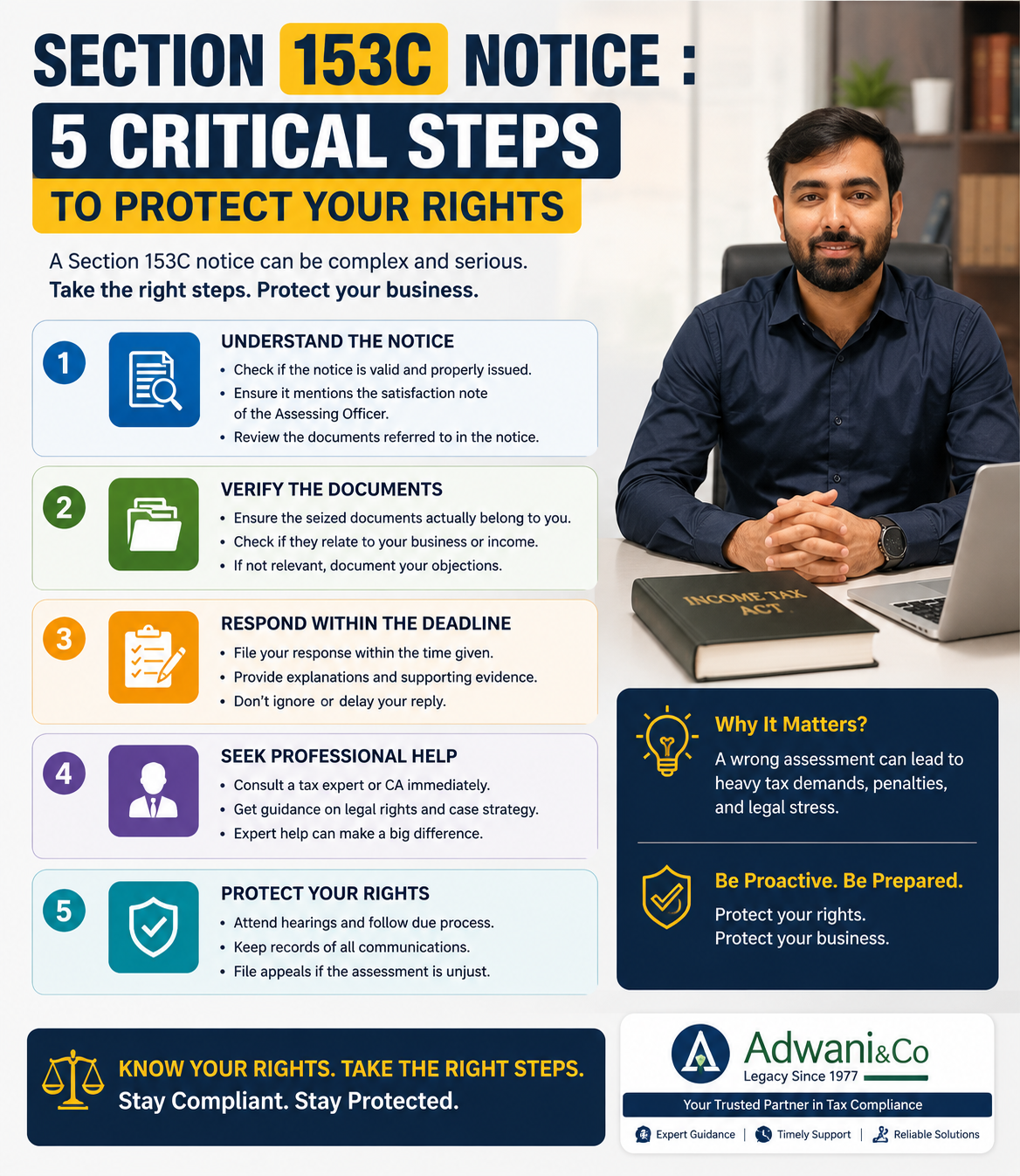

Section 153C Notice : 5 Critical Steps to Protect Your Rights

You didn’t face a search. You didn’t face a seizure. And yet, one morning, a Section 153C income tax notice lands at your door addressed to you as a third party whose documents were found during a raid on someone else. This is where taxpayers make their most expensive mistake: they either panic and overshare, or they ignore the notice entirely. Both approaches can destroy an otherwise defensible position. Here’s everything you need to know and the 5 critical steps that could make all the difference.

What Is a Section 153C Notice in Income Tax? Understanding the Search & Seizure Connection

Section 153C of the Income Tax Act, 1961 is one of the most powerful and misunderstood provisions in Indian taxation. It allows the Income Tax Department to assess a person called a ‘non-searched person’ based on incriminating documents, books of account, or assets belonging to them that were found during a search and seizure operation conducted at another person’s premises under Section 132.

In plain terms: if you are a business partner, family member, client, or associate of someone whose premises were raided, and the department finds papers or digital records belonging to you during that raid, you can receive a Section 153C search and seizure notice even though no search was ever conducted at your own address.

The Income Tax Department, as guided by CBDT circulars available on incometax.gov.in, uses this provision to widen the net of a search operation beyond the original searched person. This makes Section 153C notices particularly dangerous because taxpayers often receive them with no context about what was found, where, or by whom.

Read our detailed guide on Received a Shocking Section 153C Income Tax Notice?

Section 153C vs Section 153A: Why the Difference Matters for Your Section 153C Notice

Section 153A applies to the searched person the one whose premises were actually raided. Section 153C applies to a third party someone connected to the searched person. This distinction is not just academic. Under Section 153C, the Assessing Officer of the searched person must first record a satisfaction note establishing that the seized documents ‘belong to’ or ‘pertain to’ the non-searched person, and then transmit those documents and the satisfaction note to the AO having jurisdiction over you. If this satisfaction note is missing, vague, or improperly recorded, your Section 153C notice is legally vulnerable to challenge.

Critical Legal Point

The Supreme Court of India and multiple High Courts have consistently held that a Section 153C notice is invalid if:

• The satisfaction note by the AO of the searched person is absent or defective

• The documents found cannot be shown to ‘belong to’ the non-searched person

• The notice is issued beyond the prescribed time limit under Section 153C Source: CBDT guidelines and landmark rulings including CIT vs. Kabul Chawla (Delhi HC)

Section 153C Time Limit: A Crucial Safeguard That Many Taxpayers Miss

The income tax notice time limit under Section 153C is strictly prescribed. The AO can issue a Section 153C notice for six assessment years immediately preceding the year of search and, in cases of escaped income of ₹50 lakh or more in any year, up to ten assessment years preceding the year of search can be covered.

If a Section 153C notice is issued for years beyond this window, it is barred by limitation and legally challengeable. Always check the date of search and the assessment years covered in your notice. This simple check has helped many taxpayers avoid unnecessary compliance entirely.

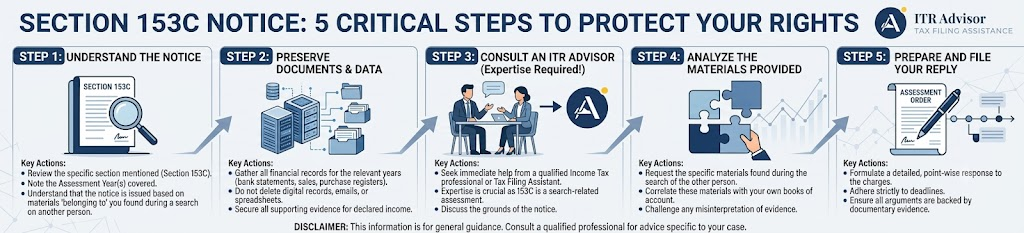

5 Critical Steps to Protect Your Rights When You Receive a Section 153C Notice

1: Do Not Panic : But Act Immediately The moment you receive a Section 153C income tax notice, acknowledge its receipt and note the response deadline. Never ignore it non-response can lead to ex-parte assessment and severe adverse orders. Your response window is typically 30 days, but this can vary.

2: Examine the Notice for Procedural Validity Check: (a) Is a satisfaction note recorded by the searched person’s AO? (b) Does the notice specify what documents were found and how they ‘belong to’ you? (c) Is the notice within the Section 153C time limit? Any defect here is a ground for legal challenge before you even address the merits.

3: Gather and Organise Your Financial Records: Compile all books of account, bank statements, ITRs, agreements, and correspondence for the years under scrutiny. Cross-check what the department may have found against what was legitimately disclosed. Unexplained gaps are far more dangerous than disclosed income.

4: File a Detailed, Calibrated Written Reply :Your reply to the Section 153C notice must be factual, legally precise, and free of unnecessary admissions. Address each document or asset the notice references. Raise preliminary objections on jurisdiction and limitation first, then respond on merits — in the same reply if the deadline doesn’t allow separate submissions.

Step 5: Engage a Qualified Tax Professional Immediately: Section 153C proceedings involve complex interplay of search and seizure law, assessment procedure, and evidentiary standards. As tax professionals associated with Adwani & Co LLP led by Dr. Haresh Adwani have noted in practice, the difference between a well-prepared Section 153C reply and a reactive one can run into crores of rupees in tax demand. Do not navigate this alone.

Key Takeaway

Section 153C notice can reach you even if your own premises were never searched

A missing or defective satisfaction note by the searched person’s AO = legally invalid notice

Always verify the Section 153C time limit notices beyond 6/10 assessment years are barred

Section 153C is distinct from Section 153A your rights as a non-searched person differ significantly

A precise, legally grounded reply is non-negotiable never reply without professional guidance Government reference: Income Tax Department guidelines at incometax.gov.in and CBDT search & seizure circulars

Frequently Asked Questions

Q1. What is a Section 153C notice and who can receive it?

A Section 153C notice is issued to a non-searched person whose documents or assets are found during a search at someone else’s premises. You can receive it even if no raid was conducted at your own address.

Q2. Can I challenge a Section 153C notice on procedural grounds?

Yes. If the satisfaction note is absent or defective, or if the notice covers years beyond the Section 153C time limit, you can raise legal objections. Courts have quashed Section 153C notices on these grounds.

Q3. How many years can be covered under a Section 153C income tax search notice?

Typically 6 assessment years preceding the year of search. In cases of escaped income of ₹50 lakh or more, this can extend to 10 assessment years.

Q4. What documents should I collect after receiving a Section 153C notice?

Collect ITRs, bank statements, books of account, contracts, and any financial records for the relevant assessment years. Cross-reference them against what the department may have seized.

Q5. Is Section 153C the same as a scrutiny notice under Section 143(2)?

No. Section 153C arises specifically from search and seizure proceedings under Section 132 and involves much higher legal stakes. A Section 153C reply requires specialised legal and tax expertise — it is far more complex than a routine scrutiny notice

Conclusion:

Receiving a Section 153C income tax notice is not the end of the world but it requires an informed, strategic response from day one. Verify the notice’s procedural validity, check the Section 153C time limit, organise your financial records, and file a calibrated reply that addresses legal objections first and merits second. The Income Tax Department’s search and seizure machinery is powerful, but it operates within legal boundaries boundaries that protect you if you know how to invoke them.

The worst thing you can do after receiving a Section 153C notice is to respond in panic, overshare information, or go silent. The second-worst thing is to face it without experienced guidance.

Author

CA. Dipesh Gurubakshani. He is a Chartered Accountant with professional experience in audit, direct taxation, and accounting advisory services.

Whether you have already received a credit card income tax notice or want to ensure you never do Adwani and Company is your trusted partner. Led by Dr. Haresh Adwani and a seasoned team of Chartered Accountants, Adwani and Company provides end-to-end income tax compliance, notice response, and financial planning services.

Get Expert Tax Guidance

If you want to file your ITR accurately and defend it confidently visit ITRAdvisor.in today.

From ITR form selection and tax regime comparison to notice response and professional review, ITRAdvisor.in gives you the tax knowledge you need to stay compliant and avoid costly mistakes.

→ Read our ITR Filing Guide for AY 2026-27

→ Explore the Old vs New Tax Regime Comparison 2026

→ Understand Income Tax Notices and How to Respond Visit: ITRAdvisor.in

Disclaimer

ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform.

The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.

© 2026 ITRAdvisor.in. All rights reserved.