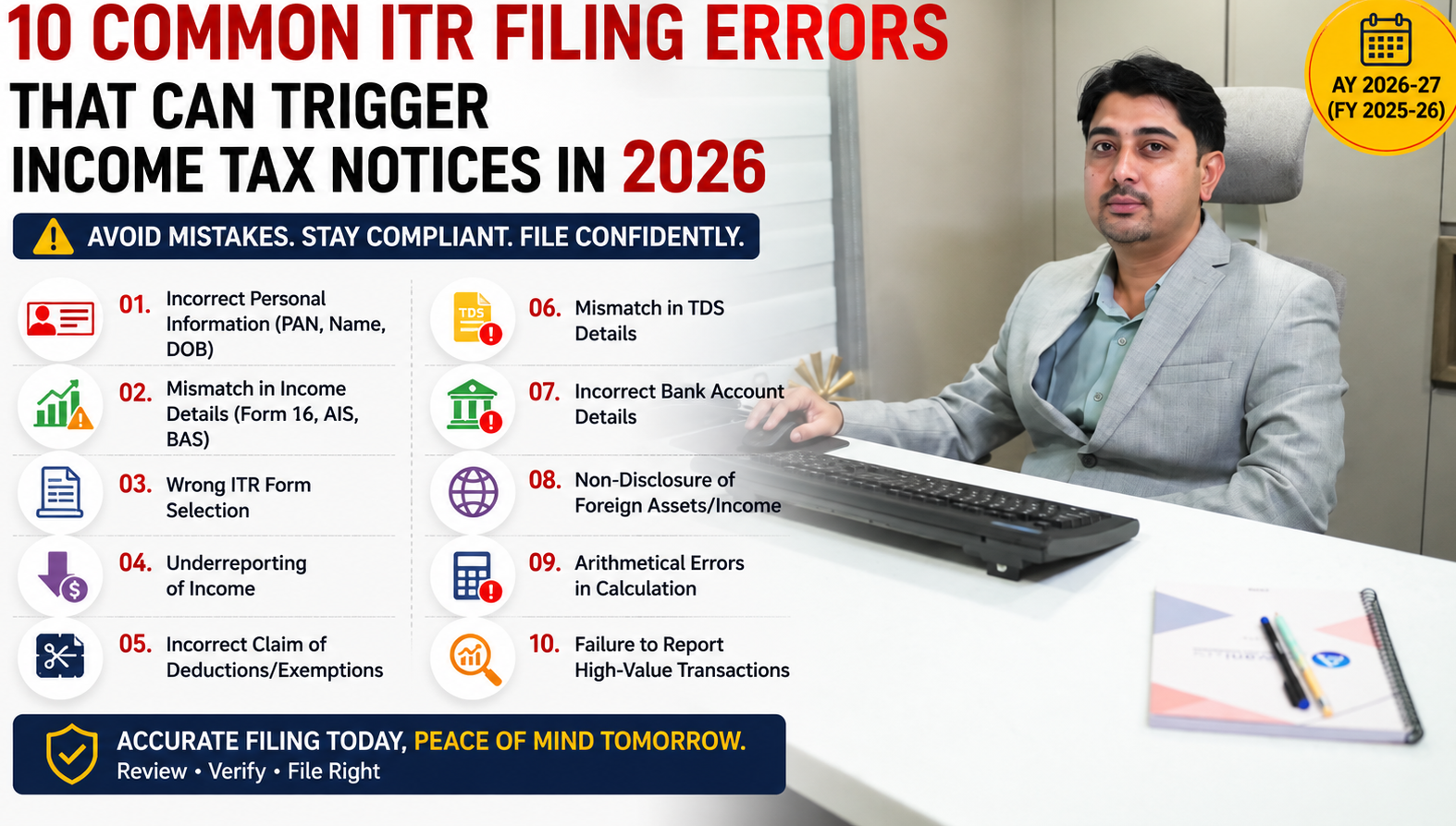

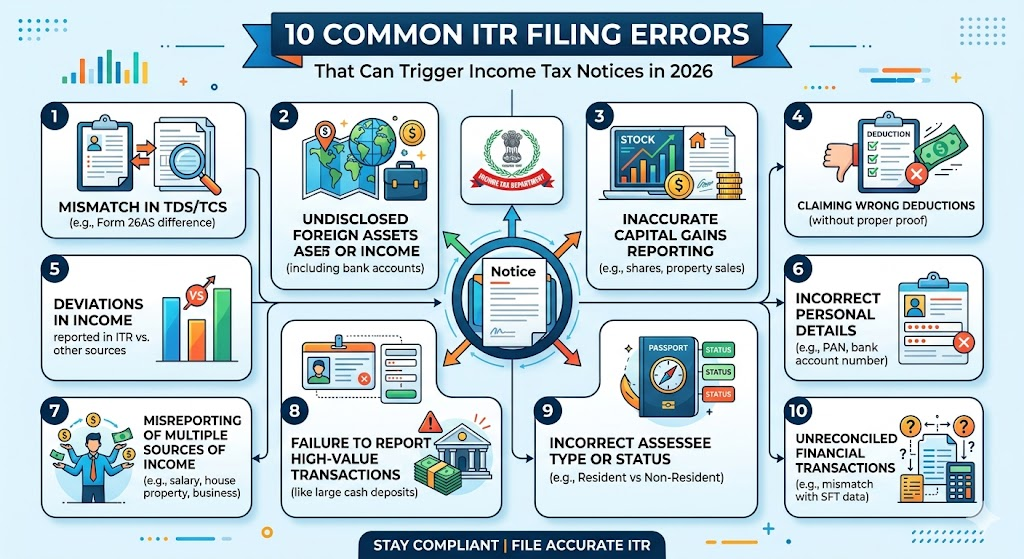

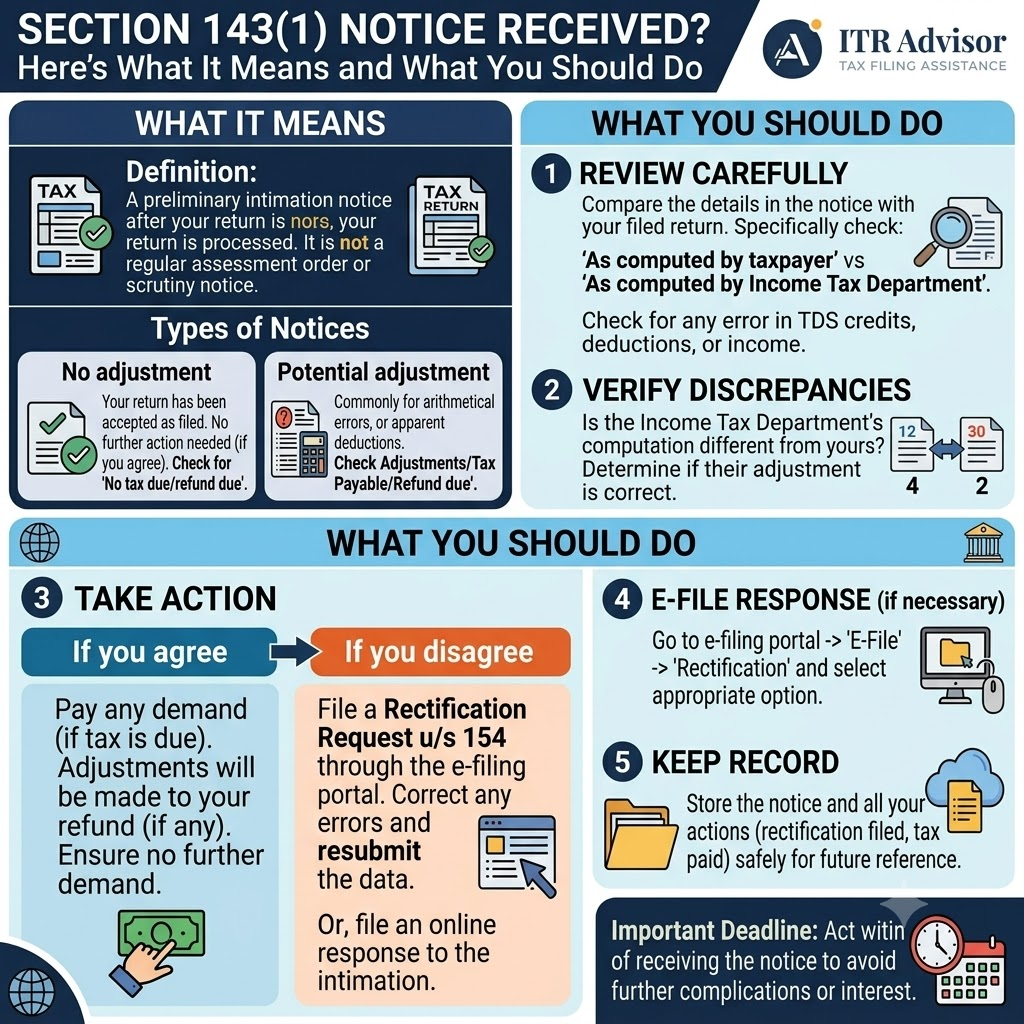

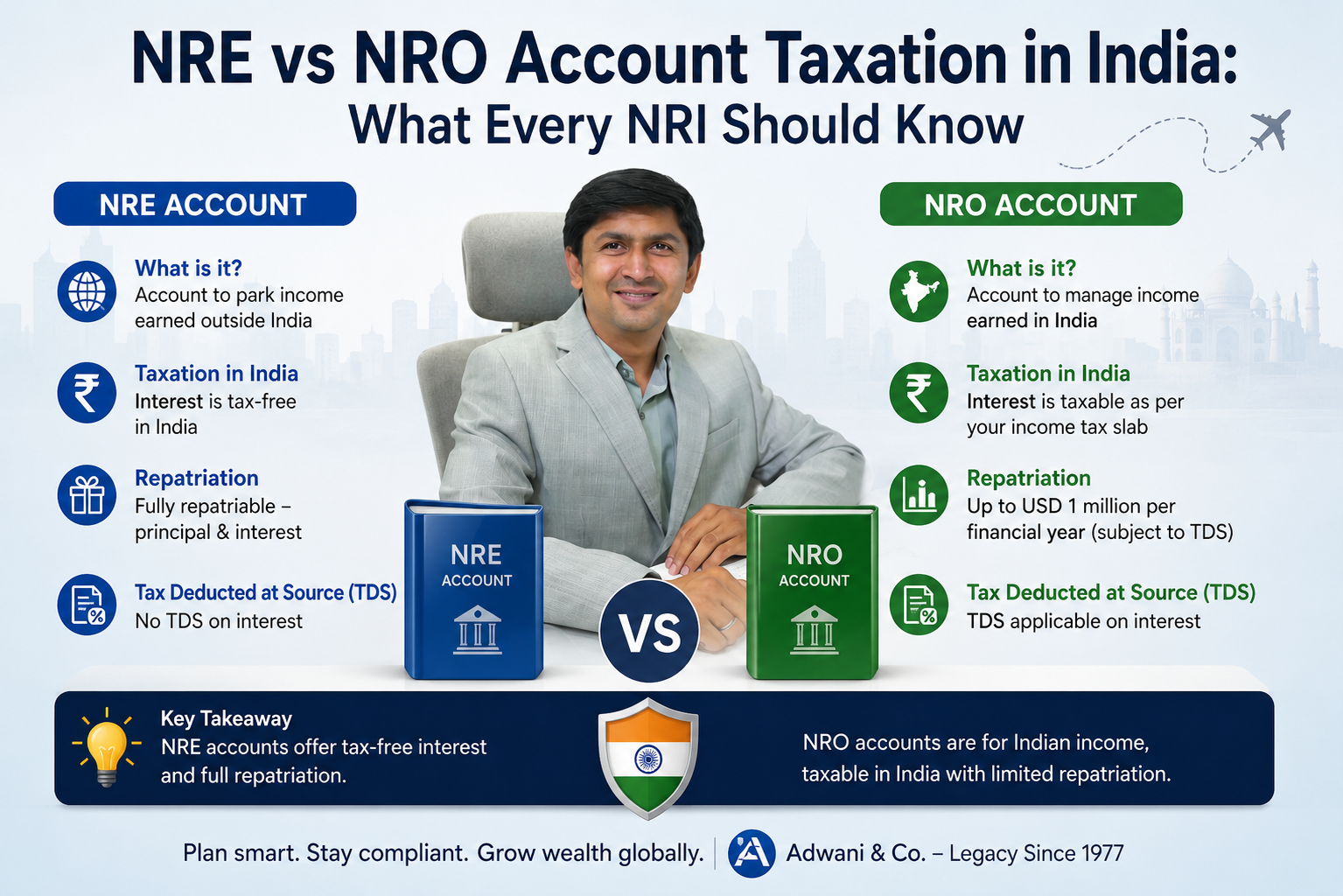

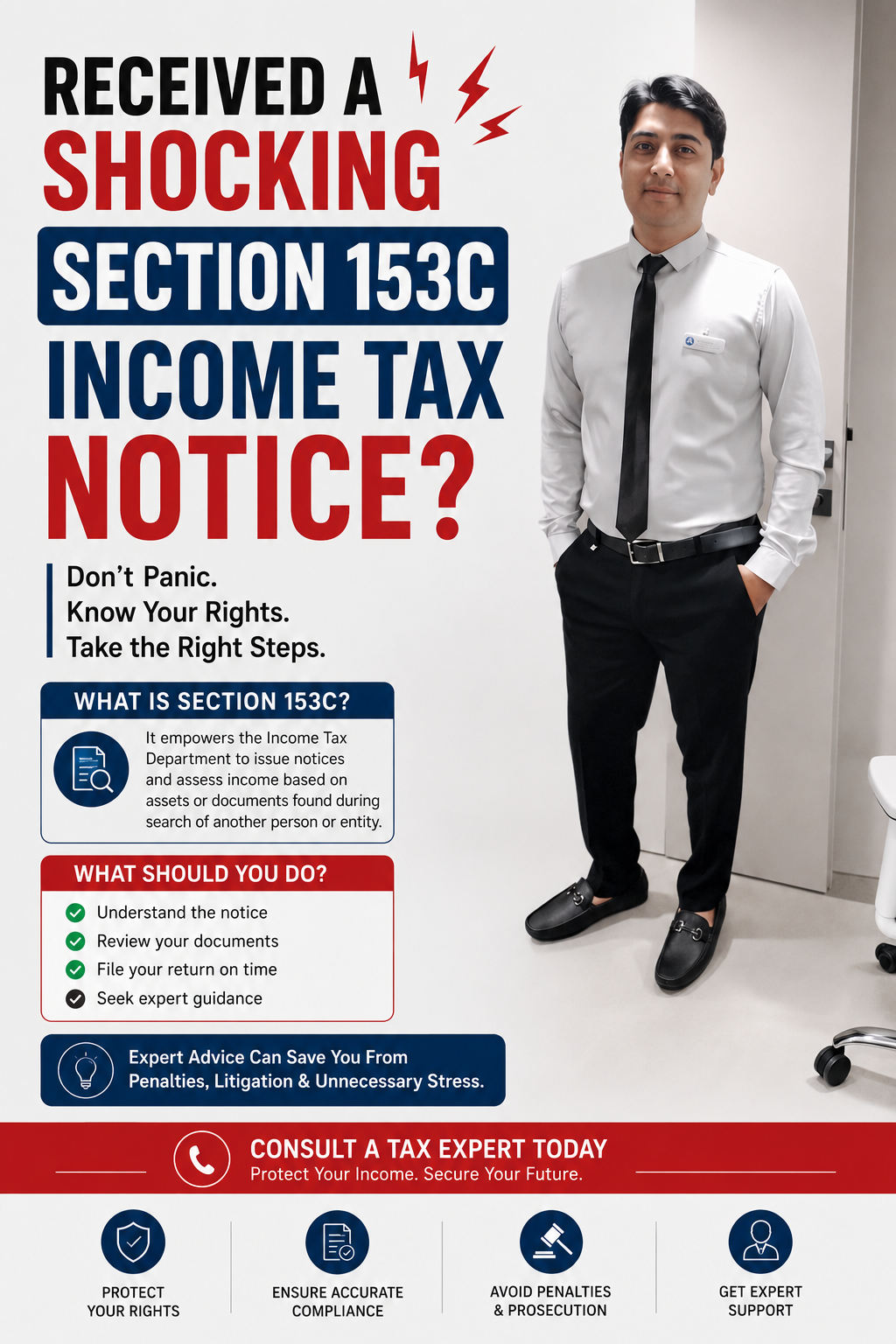

Section 153C Income Tax Notice

Here Is Your Definitive 2026 Survival Guide: Know Your Rights, Protect Your Wealth

Imagine this: The Income Tax Department raids a business associate, a vendor, or even a distant acquaintance and days later, a notice lands on your doorstep under Section 153C of the Income Tax Act. You were never searched. No officer stepped into your office. Yet suddenly, you are under the scanner for six years of your income and assets. This is not a hypothetical situation. Across India in 2025 and 2026, thousands of taxpayers salaried professionals, business owners, real estate investors, and even silent partners have received notices under Section 153C without any warning whatsoever.

If you have received such a notice or if you want to protect yourself before one arrives this guide by Dr. Haresh Adwani, of Adwani and Company, is exactly what you need. Read every section carefully, because what you learn here could save you from penalties reaching up to 200% of your tax liability.

What Is Section 153C of the Income Tax Act?

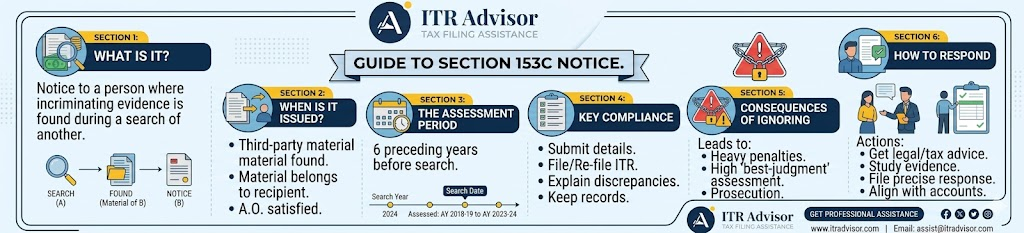

Section 153C of the Income Tax Act, 1961, is a powerful provision that empowers the Assessing Officer (AO) to issue a tax notice and initiate assessment proceedings against a person who was NOT the original subject of an income tax search or seizure. In simpler terms, if the Income Tax Department raids someone else and finds documents, books of account, digital data, jewellery, or any other asset that belongs to or pertains to you you can be assessed under Section 153C, even though your premises were never raided.

This section sits within the broader framework of search and seizure assessments under Indian tax law, alongside its companion provision, Section 153A which governs assessments of the person who was actually searched. The Income Tax Department uses Section 153C to extend its reach beyond the person searched, ensuring that any connected third party with undisclosed income does not escape scrutiny.

As Dr. Haresh Adwaniof Adwani and Company always advises clients: “Section 153C is not a minor notice. It is a full-scale tax assessment that can reopen six years of your financial history. Treating it lightly is the most expensive mistake a taxpayer can make.”

Learn more about our Income Tax Assessment Services at Adwani and Company, where our team of expert CAs handles Section 153C notices with precision and strategy.

Section 153C vs Section 153A: Understanding the Critical Difference

Many taxpayers confuse Section 153A with Section 153C, and that confusion can lead to wrong responses and serious legal consequences. Here is the clearest distinction:

Section 153A : Notice to the Person Searched

When the Income Tax Department conducts a search under Section 132 or a requisition under Section 132A, the person who was searched receives a notice under Section 153A. This notice requires filing of income tax returns for the six assessment years immediately preceding the year of search, plus the current year.

Section 153C : Notice to a Third Party (You)

When documents, assets, digital records, or books of account found during a search on someone else are determined to belong to or pertain to you, the AO of the searched person hands over those materials to your Assessing Officer. Your AO then issues you a Section 153C notice and initiates the same assessment procedure as under Section 153A.

The critical phrase here is “belongs to or pertains to.” Indian courts including the Delhi High Court in the landmark Kabul Chawla case (2015) have clarified that the material found must genuinely belong to you or contain information directly relating to your income. Without this clear ownership link, the Section 153C notice can be legally challenged and quashed.

How Is a Section 153C Income Tax Notice Triggered? Step-by-Step Process

Understanding the procedural chain that leads to a Section 153C notice helps you evaluate whether the notice issued to you is legally valid a key part of your defence strategy.

- The Income Tax Department conducts a search under Section 132 or a requisition under Section 132A at the premises of a person (let us call them Person A).

- During the search on Person A’s premises, the investigating officers discover documents, books of account, hard drives, cash, jewellery, or other assets that appear to belong to or relate to you (Person B).

- The AO in charge of Person A’s case reviews the seized material and records a Satisfaction Note a written document explaining in detail why he is satisfied that the material belongs to or pertains to Person B (you).

- The seized material is formally handed over to the AO having jurisdiction over Person B (you).

- Your AO reviews the material and issues a notice under Section 153C, requiring you to file income tax returns for the six assessment years preceding the year of search.

- Assessment or reassessment of your income for those six years begins in accordance with the provisions of Section 153A.

According to the Income Tax Department’s guidelines and confirmed by multiple High Court rulings, the Satisfaction Note at Step 3 is non-negotiable. If it is absent, vague, or not recorded in writing before the notice is issued, the entire Section 153C proceeding is legally invalid.

Real-World Example: How a Section 153C Notice Can Arrive at Your Door

Practical Example: The Income Tax Department conducts a search in FY 2023-24 at the premises of a real estate developer in Pune. During the search, investigators discover a set of financial documents referencing a private investor who had made an unrecorded cash payment of ₹45 lakhs for a commercial property. The investor was never searched. However, the documents clearly link the payment to the investor’s PAN.

The AO records a Satisfaction Note and hands over the documents to the investor’s AO. A Section 153C notice is then issued to the investor for Assessment Years 2018-19 to 2023-24 six full years. The investor now faces potential tax demand on ₹45 lakhs, plus interest under Sections 234A, 234B, and 234C, plus a penalty that can reach up to 200% of the tax evaded under Section 270A.

This example is not extraordinary. It plays out in hundreds of cases every year, and this is precisely why proactive tax planning and clean documentation matter as much as filing returns on time.

Read our detailed guide on :Income Tax Notice India 2026: Every Section Explained What It Means and How to Respond

Critical Time Limits Under Section 153C That Every Taxpayer Must Know

The Income Tax Act imposes strict time limits on assessments under Section 153C, and missing these deadlines can itself invalidate a notice. Here is what the law says:

Assessment Years Covered

Normally, a Section 153C notice covers the six assessment years immediately preceding the year in which the search was conducted. After amendments introduced in 2021, the timeline has been aligned with Section 132 and Section 132A provisions, providing greater clarity on which years can be reopened.

Extended Period of 10 Years

As amended by the Finance Act 2017, if the AO has credible evidence that undisclosed income exceeding ₹50 lakh has escaped assessment, the assessment window under Section 153C can be extended to cover up to ten years preceding the year of search. This extended period is not automatic it requires specific evidence and cannot be used as a blanket tool.

Time Limit for Completing Assessment

The Assessing Officer must complete the assessment within 12 months from the end of the financial year in which the evidence was handed over. This is a hard deadline under Section 153B, and failure to complete the assessment within this window renders the order invalid.

Dr. Haresh Adwani emphasises that checking these time limits carefully is the first defence a taxpayer should mount: “I have seen cases where the AO issued a Section 153C notice for years that were clearly outside the permissible window. A well-informed taxpayer, guided by the right CA, can get such proceedings quashed entirely based on this ground alone.”

The Satisfaction Note: Your Most Powerful Legal Shield Against a Section 153C Notice

The Satisfaction Note is arguably the most important procedural requirement in a Section 153C proceeding. Without it, the entire assessment collapses. Here is what you must know about it:

What Is the Satisfaction Note?

The Satisfaction Note is a written document prepared by the Assessing Officer of the searched person (Person A), in which he records his reasons for believing that the seized material belongs to or pertains to a third party (you, Person B). The Supreme Court and multiple High Courts have repeatedly held that this note must be prepared before the notice is issued not after.

What Happens If the Satisfaction Note Is Missing or Defective?

Indian courts have consistently quashed Section 153C assessments where the Satisfaction Note was absent, vague, or prepared mechanically. In the RRJ Securities Ltd. vs. CIT case decided by the Delhi High Court, the court held that for invoking Section 153C, the evidence must actually belong to the other person not merely refer to or relate to them. A defective Satisfaction Note is one of the strongest grounds for legally challenging a Section 153C notice.

At Adwani and Company, one of the first steps Dr. Haresh Adwani takes when reviewing a Section 153C notice is to request and examine the Satisfaction Note. A carefully prepared legal challenge based on procedural deficiencies has resulted in numerous assessments being set aside before they even begin.

Documents You Must Prepare When You Receive a Section 153C Income Tax Notice

Receiving a Section 153C notice is stressful, but a methodical, document-driven response is your most effective defence. Based on the guidelines issued by the Income Tax Department and practical experience, here is the complete list of documents you should gather immediately:

- Income Tax Returns (ITR) for all 6 relevant assessment years

- Books of account, ledgers, and financial statements for those years

- Bank statements for all accounts (savings, current, FD, OD)

- Details of all assets and liabilities during the relevant period

- Complete source of funds documentation for all major transactions

- Property purchase and sale documents (sale deeds, agreements)

- Loan agreements and repayment records

- Gift deeds or documentation for any assets received as gifts

- TDS certificates and Form 26AS for all relevant years

- PAN card, Aadhaar, and identity proof

- Any correspondence with the searched person (Person A)

- Investment records (shares, mutual funds, capital gains statements)

The Income Tax Department’s TRACES portal and the AIS (Annual Information Statement) available on the income tax e-filing portal (incometax.gov.in) provide a comprehensive picture of all transactions linked to your PAN. Reviewing your AIS before responding to any notice is a non-negotiable step recommended by Adwani and Company.

How to Respond to a Section 153C Tax Notice: A 6-Step Action Plan

Every Section 153C notice carries a response deadline. Missing that deadline can escalate the situation dramatically. Here is the structured action plan recommended by Dr. Haresh Adwani:

- Do not panic, but act immediately. Every day that passes without action reduces your options.

- Consult a qualified Chartered Accountant with proven experience in search and seizure assessments. This is not the time for general tax advice.

- Request the Satisfaction Note and review it carefully with your CA to determine if it is procedurally valid.

- Gather all the documents listed above and prepare a detailed reconciliation of your income, assets, and major transactions for the relevant years.

- File the required income tax returns for past years if they were not previously filed, and ensure all disclosures are complete and accurate.

- Respond to the notice within the stipulated deadline with a professionally prepared, legally sound reply that addresses each point raised by the AO.

If the Satisfaction Note is defective or the notice is issued for years beyond the permissible period, your CA may advise filing a writ petition before the appropriate High Court to get the proceedings stayed or quashed.

The team at Adwani and Company led by Dr. Haresh Adwani has successfully represented hundreds of clients before Assessing Officers, CIT(Appeals), and the Income Tax Appellate Tribunal (ITAT) in cases arising from Section 153C notices. A professionally drafted response, backed by clean documentation and sound legal arguments, resolves the majority of these cases at the earliest stage.

Consequences of Ignoring or Mishandling a Section 153C Income Tax Notice

The Income Tax Act provides for serious consequences when a taxpayer ignores a Section 153C notice or fails to respond adequately. Understanding these consequences reinforces why expert guidance is non-negotiable:

- Tax demands on undisclosed income discovered during assessment

- Interest under Section 234A (delay in filing), Section 234B (advance tax shortfall), and Section 234C (installment default)

- Penalty under Section 270A of up to 200% of the tax amount in cases of misreporting or under-reporting of income

- Best judgment assessment under Section 144 if the taxpayer fails to comply with notices or produce required documents

- Potential prosecution proceedings in cases involving deliberate concealment of income

None of these consequences are inevitable if you respond correctly and promptly. The Income Tax Department’s own circulars emphasise that taxpayers who cooperate fully and disclose income honestly are treated more favourably during assessment proceedings.

Official Government References and Authority Signals

The legal basis for Section 153C proceedings is firmly established in the Income Tax Act, 1961, as administered by the Central Board of Direct Taxes (CBDT). The CBDT has issued multiple circulars and instructions clarifying procedural requirements for Assessing Officers conducting assessments under Sections 153A and 153C. Taxpayers who receive Section 153C notices have the right to access these circulars and rely on them in their defence.

The Ministry of Finance, through the Income Tax Department, has also introduced the Faceless Assessment Scheme to reduce physical interaction and improve transparency in assessment proceedings. While Section 153C cases may have specific exemptions from full faceless assessment, the principles of natural justice including the right to be heard and the right to challenge procedural deficiencies remain fully applicable.

For the most current information on income tax assessments, the official Income Tax Department website at incometax.gov.in and the CBDT’s circulars available on the website of the Ministry of Finance are the authoritative sources.

Frequently Asked Questions

Q1. Can I receive a Section 153C notice even if the Income Tax Department never searched my premises?

Yes. Section 153C specifically applies to persons who were NOT the subject of the original search. If documents or assets belonging to you are found during a search at someone else’s premises, you can receive a Section 153C notice.

Q2. How many years of income can be reassessed under Section 153C?

Normally, the six assessment years immediately preceding the year of search. In cases where undisclosed income exceeding ₹50 lakh is discovered, the assessment window can be extended to ten years. The exact years depend on when the search was conducted and when the material was handed over to your AO.

Q3. What is the Satisfaction Note in Section 153C, and why does it matter?

The Satisfaction Note is a mandatory written document prepared by the AO of the searched person, recording the reasons why seized material belongs to or pertains to a third party. Without this note, a Section 153C notice is legally invalid and can be challenged in court.

Q4. What documents should I keep ready when I receive a Section 153C notice?

You should immediately gather income tax returns for the past six years, bank statements, books of account, asset and liability details, property documents, loan agreements, Form 26AS, and source of funds documentation for all major transactions. Consulting an experienced CA

Q5. Can a Section 153C notice be challenged or quashed?

Yes. If the Satisfaction Note is absent or defective, if the notice covers years beyond the permissible period, or if the seized material does not genuinely belong to the taxpayer, the Section 153C notice can be legally challenged before the High Court through a writ petition or before the CIT(Appeals) or ITAT in appeal proceedings.

Q6. How can Adwani and Company help me respond to a Section 153C tax notice?

Dr. Haresh Adwani and the expert team at Adwani and Company provide end-to-end assistance: reviewing the Satisfaction Note, identifying legal deficiencies, gathering and organising documents, preparing professionally drafted responses, representing clients before the AO, CIT(Appeals), and ITAT, and if necessary, pursuing High Court relief. Connect with Adwani and Company today at www.adwaniandco.com.

Conclusion:

A Section 153C income tax notice is not the end of the road. It is a beginning a beginning of a legal process that, with the right expertise and preparation, can be navigated successfully. The law provides clear procedural safeguards including the mandatory Satisfaction Note requirement, strict time limits for assessment, and the right to appeal and these safeguards exist precisely to protect taxpayers from arbitrary or unlawful proceedings.

The two most important actions you can take right now are: first, understand the provisions of Section 153C thoroughly so that you know your rights; and second, engage a qualified and experienced Chartered Accountant who has handled income tax search assessment cases before. Do not attempt to respond to a Section 153C notice without professional guidance. The stakes are too high.

Dr. Haresh Adwani has built Adwani and Company on the principle that every taxpayer deserves expert, transparent, and accessible professional guidance especially in high-stakes situations like a Section 153C notice. With a team of experienced CAs, tax lawyers, and assessment specialists, Adwani and Company has successfully resolved Section 153C and Section 153A cases across India.

Read our detailed guide on Income Tax Appeals and Assessment Proceedings to understand your complete rights as a taxpayer under Indian tax law.

About the Author : Prafull Nile

Prafull Nile is a senior taxation and accounting professional associated with Adwani & Co LLP, bringing over 19 years of extensive experience in direct taxation, tax audits, income tax assessments, GST audits, and financial statement finalization. He has successfully managed diverse client engagements across industries, providing strategic guidance on tax compliance, assessments, and regulatory matters. In addition to his technical expertise, Prafull leads and mentors teams, ensuring high standards of service delivery and operational excellence. His practical approach, deep understanding of tax laws, and commitment to client success make him a trusted advisor for businesses and professionals navigating complex financial and compliance requirements.

At ITRAdvisor.in, we help taxpayers with:

✔️ ITR Filing Review

✔️ AIS Reconciliation

✔️ Capital Gains Reporting

✔️ NRI Taxation

✔️ Tax Notice Response

✔️ Revised Returns

✔️ Income Tax Planning

✔️ Refund and Compliance Issues

If you are unsure whether your return has been filed correctly or want a professional review before submission, consulting an experienced tax professional can help avoid costly mistakes.

Visit ITRAdvisor.in for expert assistance with your Income Tax Return and tax compliance requirements.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP

A prominent “File Your ITR Now” button near the top and again at the end of the article.

Need help filing your Income Tax Return? Click the WhatsApp icon and our team will guide you through the process and assist you with your ITR filing.

Have questions about your ITR? Click the WhatsApp icon to connect with our tax experts for quick guidance and personalized assistance.