CA Dipesh Gurubakshani June 2026 8 min read

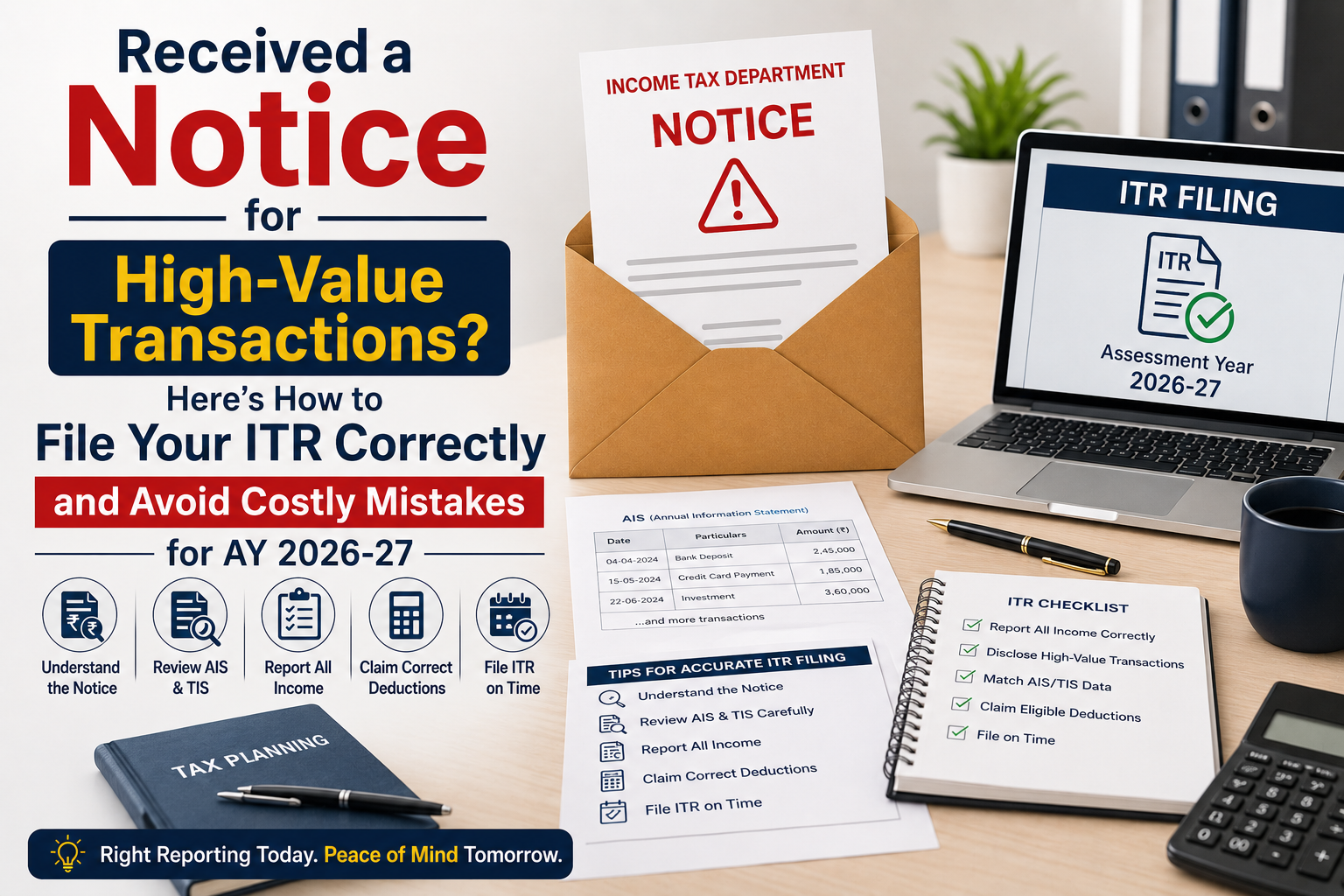

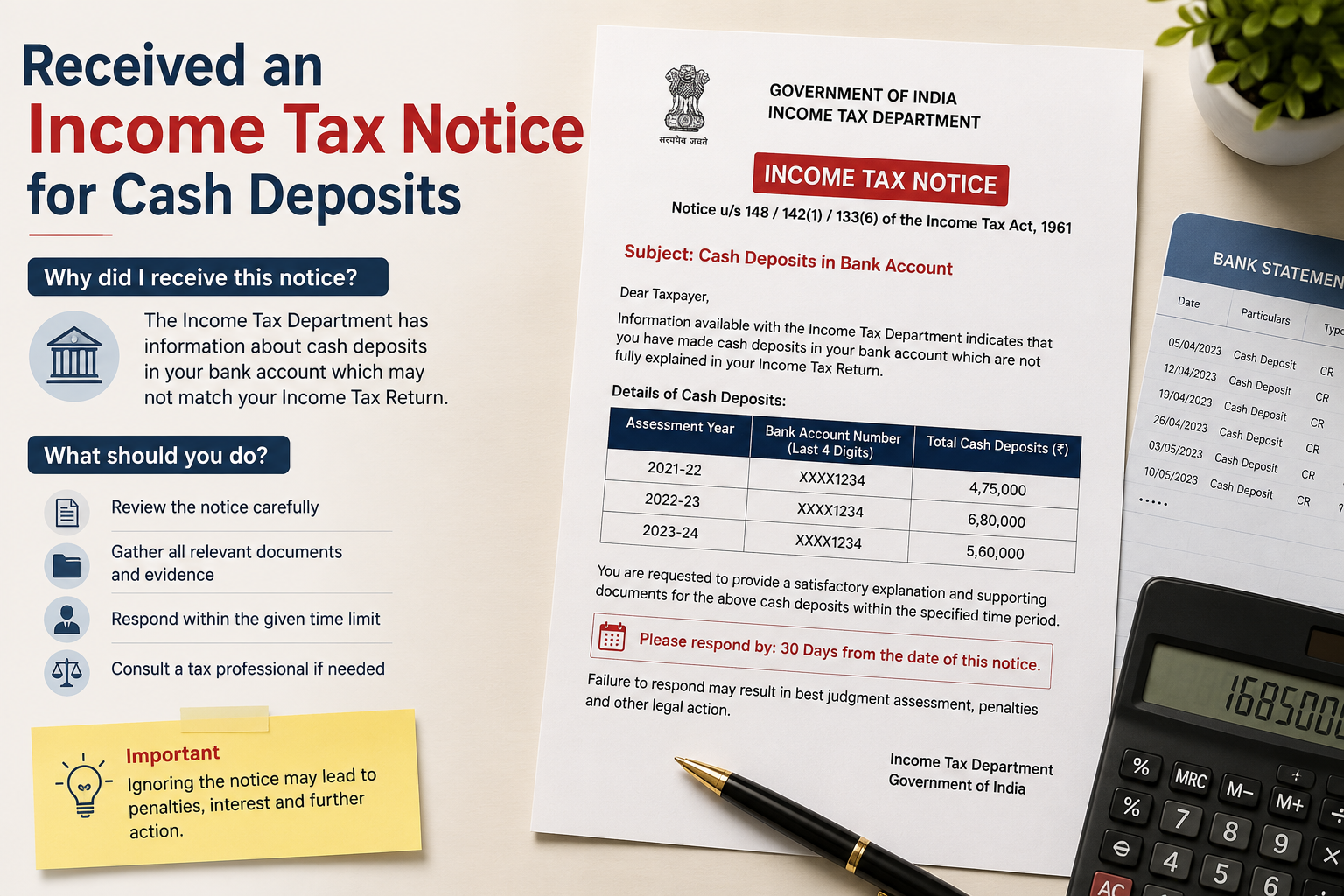

Received an Income Tax Notice for Cash Deposits? Don’t Panic

Have you recently received an Income Tax notice for cash deposits in your bank account?

You’re not alone

Every year, thousands of taxpayers receive notices from the Income Tax Department after depositing substantial amounts of cash in savings accounts, current accounts, or other bank accounts.

In many cases, the deposits are genuine and fully explainable. However, ignoring the notice or providing an incomplete response can lead to scrutiny, reassessment proceedings, additional tax demands, penalties, and prolonged litigation.

This guide explains why you may have received an Income Tax notice for cash deposits, what documents you should collect, how to respond, and how to protect yourself from unnecessary tax disputes in AY 2026-27.

Why Did You Receive an Income Tax Notice for Cash Deposits?

Banks and financial institutions report certain high-value transactions to the Income Tax Department.

The Department uses data analytics, PAN-based reporting, AIS (Annual Information Statement), and other information sources to identify cases where cash deposits appear inconsistent with the income reported in the Income Tax Return (ITR).

Common situations that trigger notices include:

- Large cash deposits in savings accounts

- Significant cash deposits in current accounts

- Cash deposits not matching declared income

- Cash deposits during specific monitoring periods

- High-value transactions reflected in AIS

- Cash deposits where no ITR has been filed

The notice does not automatically mean tax evasion. It simply means the Department requires an explanation.

Common Reasons for Large Cash Deposits

Before responding, identify the actual source of funds.

Legitimate sources may include:

- Cash Sales from Business

Businesses dealing in cash may deposit daily collections into bank accounts.

Supporting records should be maintained.

- Agricultural Income

Agricultural income may generate substantial cash receipts in certain cases.

Proper evidence should be available.

- Withdrawal and Redeployment of Cash

Taxpayers sometimes redeposit cash previously withdrawn from bank accounts.

A clear cash flow trail is important.

- Sale of Assets

Cash received from the sale of certain assets may be deposited into a bank account.

Documentation must support the transaction.

- Gifts or Family Contributions

In some situations, cash may have been received from family members or relatives.

Proper documentation becomes critical.

- Past Savings

Taxpayers may deposit accumulated cash savings.

However, the source and accumulation history should be capable of explanation.

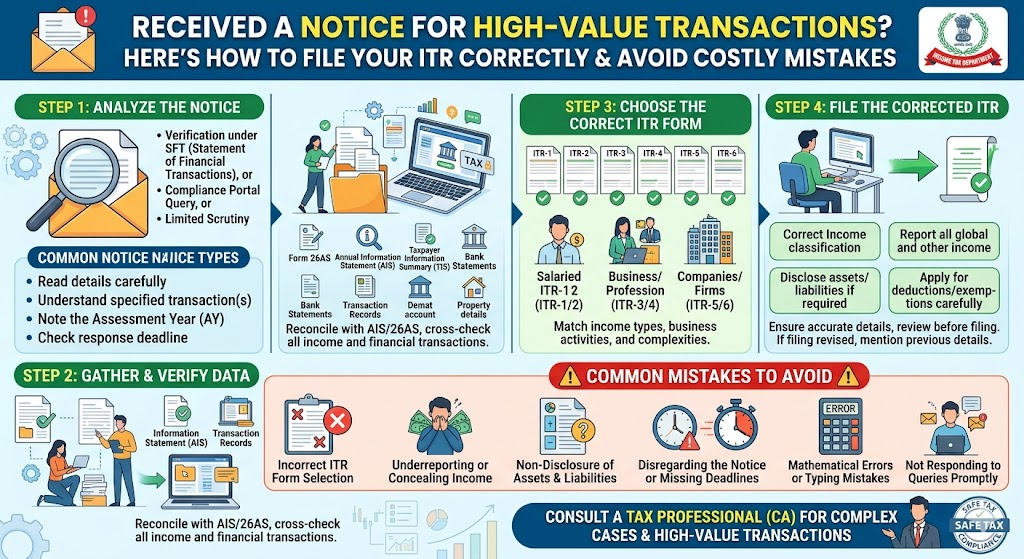

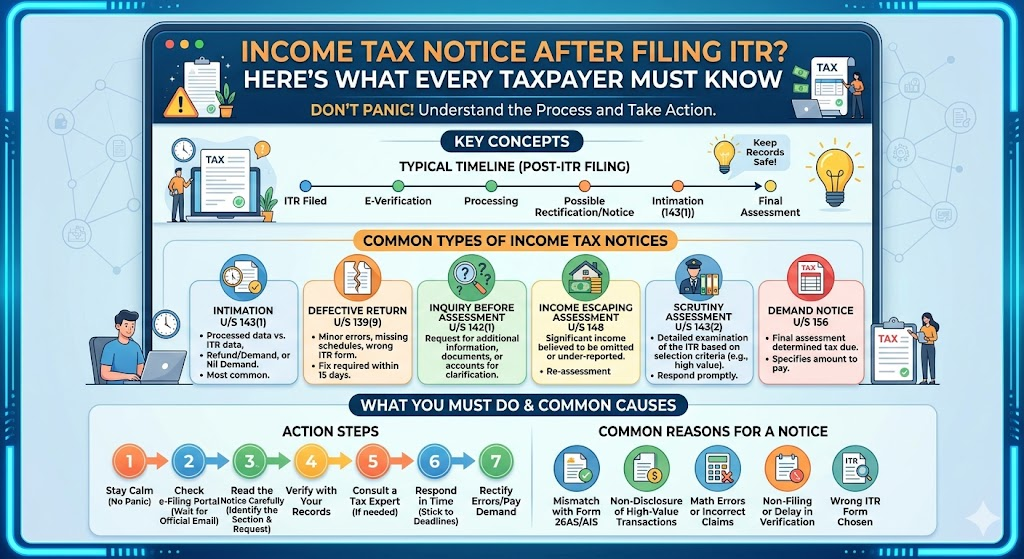

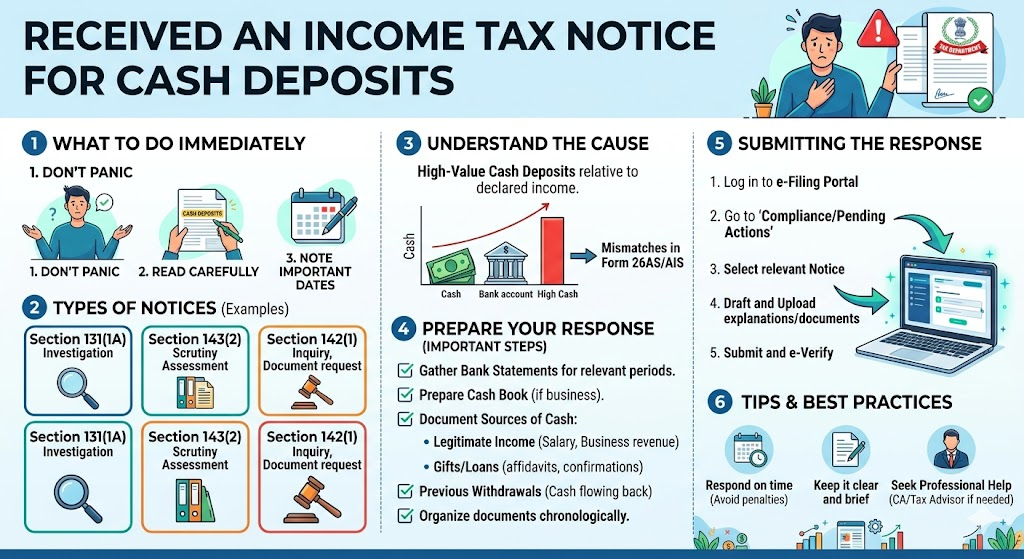

What Types of Notices May Be Issued?

The Income Tax Department may issue different notices depending upon the facts of the case.

Common notices include:

Notice Seeking Information

The Department may ask you to explain the source of cash deposits and provide supporting evidence.

Scrutiny Proceedings

Your return may be selected for detailed examination.

Reassessment Proceedings

In certain circumstances, reassessment proceedings may be initiated if income is believed to have escaped assessment.

Section 148 Notice

A notice under Section 148 may be issued in cases where the Department believes taxable income may not have been properly reported.

A Section 148 notice should never be ignored and requires careful professional review.

What Should You Do Immediately After Receiving the Notice?

Step 1: Read the Notice Carefully

Identify:

- Notice section

- Assessment year involved

- Response deadline

- Information requested

Different notices require different responses.

Step 2: Download AIS and Form 26AS

Review:

- Reported cash transactions

- Bank information

- TDS records

- Other financial transactions

- TDS records

- Other financial transactions

- Many notices originate from information reflected in AIS.

Step 3: Gather Supporting Documents

- Collect documents relevant to the source of cash deposits.

- Examples include:

- Bank statements

- Cash books

- Sale agreements

- Agricultural records

- Income records

- Gift documentation

- Business books of accounts

- The stronger the documentation, the stronger the response.

Step 4: Prepare a Cash Flow Explanation

- The Income Tax Department generally expects a logical explanation supported by evidence.

- A proper cash flow statement should explain:

- Opening cash balance

- Cash receipts

- Cash utilization

- Cash deposits made

- This often becomes the most important document in cash deposit cases.

What Happens If You Ignore the Notice?

Ignoring a notice can create serious problems.

Possible consequences include:

- Best judgment assessment

- Addition of unexplained income

- Additional tax liability

- Interest charges

- Penalty proceedings

- Further notices and litigation

Even when the cash deposits are genuine, failure to respond can result in adverse outcomes.

Can Cash Deposits Be Treated as Unexplained Income?

Yes.

If a taxpayer fails to satisfactorily explain the source of cash deposits, the Department may treat the amount as unexplained income under applicable provisions of the Income Tax Act.

This can lead to:

- High tax liability

- Interest

- Penalties

- Extended scrutiny

Therefore, documentation and professional representation are extremely important.

Example:

Cash Deposit Notice Successfully Explained

Mr. Sharma received a notice regarding cash deposits of ₹18 lakh in his savings account.

Initially, he was concerned that the Department would treat the entire amount as unexplained income.

Upon review, it was found that:

- Part of the deposits represented business receipts

- Part represented redeposit of earlier withdrawals

- Supporting records were available

A detailed explanation with documentary evidence was submitted.

As a result, the matter was resolved without adverse additions.

This demonstrates the importance of proper representation and documentation.

Common Mistakes Taxpayers Make

Ignoring the Notice

Many taxpayers assume the issue will disappear automatically.

It will not.

Responding Without Reviewing Documents

Incorrect explanations can weaken the case.

Providing Incomplete Information

Half-complete responses often generate additional queries.

Missing Response Deadlines

Delays can adversely affect the outcome.

Not Seeking Professional Advice

Complex cash deposit cases often require technical tax analysis and structured submissions.

Read our detailed guide on: Income Tax Notice After Filing ITR? Here’s What Every Taxpayer Must Know

How to Avoid Cash Deposit Notices in Future To reduce future risks:

✅ File your ITR on time

✅ Maintain proper books and records

✅ Reconcile cash transactions regularly

✅ Review AIS before filing returns

✅ Maintain supporting evidence for large cash transactions

✅ Ensure reported income matches actual financial activity

Frequently Asked Questions (FAQs)

1. Why did I receive an income tax notice for cash deposits

The notice is generally issued when cash deposits reported by banks appear inconsistent with the income disclosed in your tax records.

2.Does receiving a notice mean I have done something wrong?

No. A notice simply means the Department wants clarification regarding the transaction.

3.Can cash deposits from past savings be explained?

Yes, provided sufficient evidence and a credible explanation are available.

4.What if I received a Section 148 notice for cash deposits?

A Section 148 notice should be reviewed carefully and responded to within the prescribed time limits after evaluating the facts and supporting records.

5.Should I handle the notice myself?

Simple cases may be manageable. However, substantial cash deposits or reassessment proceedings often require professional assistance.

Author

CA Dipesh Gurubakshani is a Chartered Accountant with Adwani & Co LLP, Pune, specialising in income tax audit, direct taxation, and accounting advisory. He supports clients across statutory compliance, financial reporting, and income tax matters with a focus on accuracy, regulatory adherence, and disciplined execution.Received an Income Tax Notice for Cash Deposits? We Can Help.

If you have received:

- An income tax notice for cash deposits

- A cash transaction notice

- A scrutiny notice

- A Section 148 notice

- A reassessment notice

our experienced tax professionals can help you prepare a strong response supported by proper documentation and legal analysis.

Contact ITR Advisor Today

Don’t ignore the notice. The right response at the right time can make all the difference.

Disclaimer: ITRAdvisor.in is an educational and informational platform focused on tax awareness and compliance updates. Nothing contained herein should be construed as solicitation or advertisement of professional services. Professional services, where applicable, are rendered in accordance with ICAI guidelines. This article is published on ITRAdvisor.in, a tax and compliance knowledge platform. The content has been reviewed for technical accuracy by professionals associated with Adwani & Co LLP.